It has been a sobering month for Australia’s industry superannuation funds, which have been attacked from almost every angle.

The harshest attacks have come from Coalition MPs.

Assistant Superannuation Minister, Jane Hume, accused industry superannuation funds of having a “structural weakness… that has been hiding in plain sight” in relation to their over-exposure to unlisted assets and their resultant liquidity problems. MP Andrew Bragg also accused these same funds of “bad management” for being so exposed to illiquid unlisted assets

Coalition MP, Tim Wilson, used his position as House economics committee chairman to question why some industry superannuation funds had not adequately written down their exposures to unlisted assets in proportion to equivalent listed assets.

He was joined by Exante Data’s head of Asia-Pacific, Grant Wilson (no relation), who raised similar concerns, arguing that unit prices in some industry funds were being artificially inflated by the failure to write-down unlisted assets.

Finally, the chairman of the Financial System Inquiry, David Murray, lashed calls for the Reserve Bank of Australia (RBA) to provide industry superannuation funds with liquidity support, arguing that it would create a “moral hazard” that would encourage the industry to make poor risk management decisions in the future.

With this background in mind, it is important to recognise that we witnessed similar shenanigans by superannuation funds during the Global Financial Crisis, when they found themselves facing similar liquidity problems:

If this was the first time Australia’s cosseted superannuation sector found itself in a crisis-induced crunch, you could forgive the industry its current consternation. This is however starting to look like a replay of the Global Financial Crisis, little more than a decade ago…

For funds with significant exposure to physical assets such as commercial property, airports, toll roads and ports, liquidity management and fair pricing of their fund options becomes even more problematic…

Reading between the lines of recent press releases by the various industry associations, fund liquidity is of serious concern to the industry at present. Sufficiently serious that the RBA has reportedly been quietly working on a plan to provide a liquidity backstop to funds in the months ahead.

It is an issue that the super regulator, APRA, is also keenly aware of. It had to be involved when a number of entities, both bank-owned retail super and industry funds, found themselves in exactly this same liquidity crunch during the Global Financial Crisis…

Worryingly, unless there is genuine reform, the next crisis will likely produce the same outcome.

The fact of the matter is that superannuation funds should never experience liquidity problems, especially with compulsory inflows of 9.5% of everyone’s wages via the superannuation guarantee.

The Australian Treasury forecasts that up to $27 billion will be withdrawn from superannuation accounts in response to the Morrison Government’s emergency access arrangements, whereas industry superannuation funds have estimated redemptions of up to $65 billion.

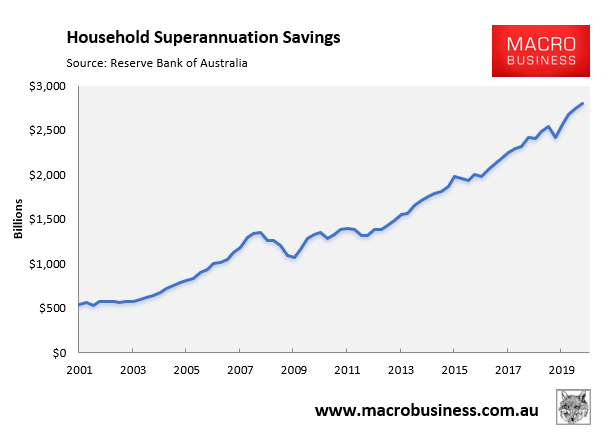

Even if the funds are correct, and $65 billion is withdrawn, this represents less than 2.5% of the $2.8 billion in total superannuation savings as at December 2019:

This is a tiny percentage of total superannuation assets that should be easily manageable.

Those funds that cannot meet redemptions due to excessive exposure to illiquid assets should not be bailed out by the RBA, but rather be forced to bite the bullet, sell their assets at market prices, crystallise losses, and then face up to their investors.

This is the only way to instill market discipline and weed ‘moral hazard’ out of the system, as well as ensure that funds undertake proper risk management in the future.