According to The AFR, nearly one million Australians have already registered their interest to access up to $20,000 of emergency funds from their superannuation accounts, representing nearly two-thirds of the Morrison Government’s forecast of 1.6 million people:

A total of 975,300 super members registered early interest in the ATO scheme before the April 20 start date. The government expects about 1.6 million to make use of the hardship access.

This weekend, it was revealed that the Australian Taxation Office (ATO) has approved 456,000 of these applications, averaging around $8,000 and totalling $3.8 billion.

These funds will require payment by superannuation funds over this coming week.

Industry superannuation funds are being hit particularly hard, suffering triple the withdrawal rate of retail funds:

The influx of applications to industry funds so far is almost three times the volume experienced by bank-owned and retail funds, despite being only 17 per cent larger in its total market share of assets under management…

Not surprisingly, industry funds operating in the hospitality, retail and travel space have been hit hardest from young Australians that have recently lost their jobs:

A call-around by Money Management revealed that most superannuation funds have received at least 200 to 300 early release requests with more than half coming from younger members with low balances…

The superannuation funds dealing with the highest numbers of applicants (in the tens of thousands) were those in the travel, hospitality and retail industry such as Hostplus, Clubplus and REST…

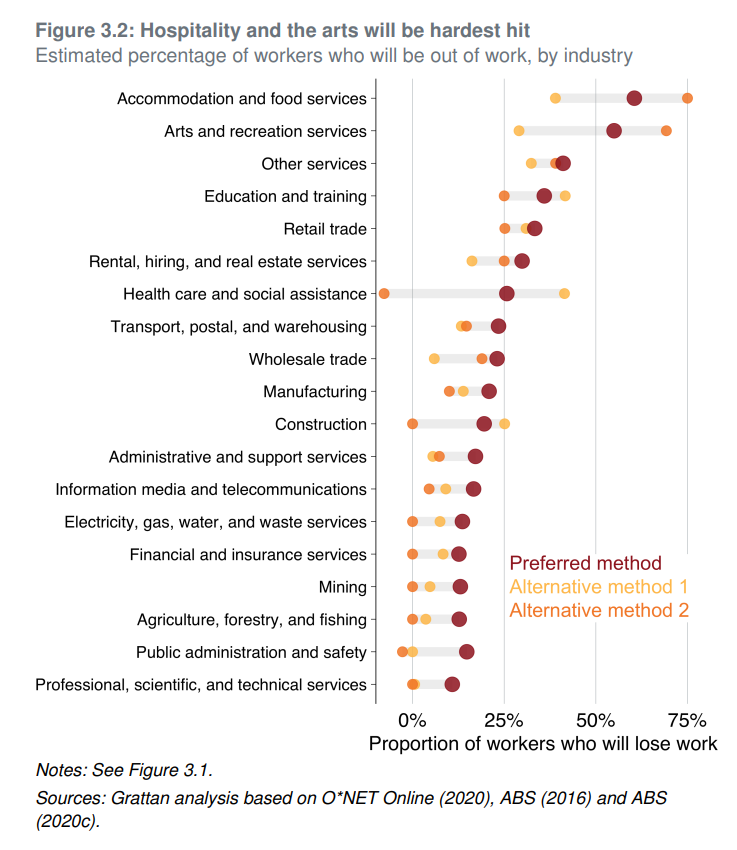

The Grattan Institute’s latest unemployment projections show that these industries will continue to be hit hardest from the COVID-19 economic collapse, with between 25% and 75% of workers losing their jobs:

Therefore, these early withdrawals could merely be the tip of the iceberg for the industry superannuation sector, which faces further heavy withdrawals of members’ funds.

This could pose an acute liquidity problem for some industry funds, namely those that have operated on the erroneous assumption that their younger member bases would not withdraw their funds for decades and that they would continue to receive ongoing inflows via the compulsory superannuation guarantee.

Based on these assumptions, some industry funds have invested heavily in illiquid assets like infrastructure and private equity, which now may have to be sold at depressed prices.

This explains the incessant lobbying by industry super funds for emergency liquidity support from the Reserve Bank of Australia. They want to be bailed out for poor risk management.