Liberal Party MP, Tim Wilson, has used his position as House economics committee chairman to question why industry superannuation funds have failed to property write-down their unlisted assets to reflect recent adverse market movements:

The unlisted asset holdings of super funds are typically revalued quarterly. But a number of large funds have made ad hoc revaluations in the unfolding crisis, cutting unlisted infrastructure, for example, by about 7.5 per cent…

“If there is a difference, why is there a difference?” Mr Wilson asked in letters that require responses by the end of the month.

Critics have raised a related problem – the major inequities that can occur between members as some panicked investors move to cash or into a new fund entirely.

If a fund was to conduct an ad hoc revaluation of its unlisted assets of 7.5 per cent on a Tuesday, members switching to cash or moving to another fund a day before will have grabbed their money and ran at an “inflated” unit price…

Exante Data’s head of Asia-Pacific, Grant Wilson… said better informed and more engaged members would switch to more conservative investment options at “artificially high” unit prices, leaving less informed members in a much smaller pool of investors with assets worth much less than when their peers opted out.

The attack continues via The AFR from Exante Data’s head of Asia-Pacific, Grant Wilson:

Think of a hypothetical super fund with $50 billion in assets under management as at December 31. Assume that the fund has 1 million members, most of whom are eligible to access two instalments of up to $10,000 under the Treasury’s current plan, applications for which open on April 20.

Assume as well that the fund has a high level of concentration in unlisted assets, such as infrastructure, property, private equity, structured credit and alternatives. Let us say a 40 per cent weight, for example, with the balance held in more traditional assets such as equities, bonds and cash.

As at March 31 this hypothetical fund reports that performance has deteriorated significantly due to COVID-19. Let us say from up 10 per cent for the financial year at end December, to now down 10 per cent.

With Australian shares down 25 per cent for the quarter, a result like this would probably be expected. Indeed many actual super funds, including those we briefed on COVID-19 through early February on a gratis basis, will report much worse than this.

The problem is the unlisted assets.

If our hypothetical fund refuses to write down the value of these assets to realistic levels, the resulting unit price will be artificially high.

To the extent that the unit price remains artificially high as redemptions mount, the outcome for those less informed and less engaged members will be devastating.

In our example, if 25 per cent of AUM is redeemed down 10 per cent, and the unlisted assets are then marked down by 30 per cent, those remaining fund members will be looking at losses of 28 per cent.

If instead, the writedown is done in a timely manner, the losses are shared equitably, with all members in our hypothetical fund down 23 per cent.

Of course, readers will know that the issue of industry superannuation funds’ high share of unlisted assets, and the problems this can cause, was first raised at MB by Damien Klassen, Head of Investments at the Macrobusiness Fund. Public policy advocacy is part of MB’s remit so we’re always pleased to see other’s follow along.

Basically, for some industry superannuation funds, the value they are telling everyone the unlisted assets are worth is not the true value, which means their unit prices remain inflated:

A few industry funds have written down assets. For example, AustralianSuper has revalued its unlisted infrastructure and property holdings downwards by 7.5%.

But look at the rest of the market. The listed property sector is off more than 40%. Airports? Down 30%+. Private Equity? Ha! You are telling me that illiquid shares are worth a few per cent less while listed shares are down 25%+ and illiquid bonds aren’t even trading?

The writedowns help, but are nowhere near the level the assets would sell for today…

This, according to Damien Klassen, can mean that those whom withdraw their funds early before unlisted assets have been written down receive an over-sized redemption, whereas those whom remain in the fund have their investment value diluted.

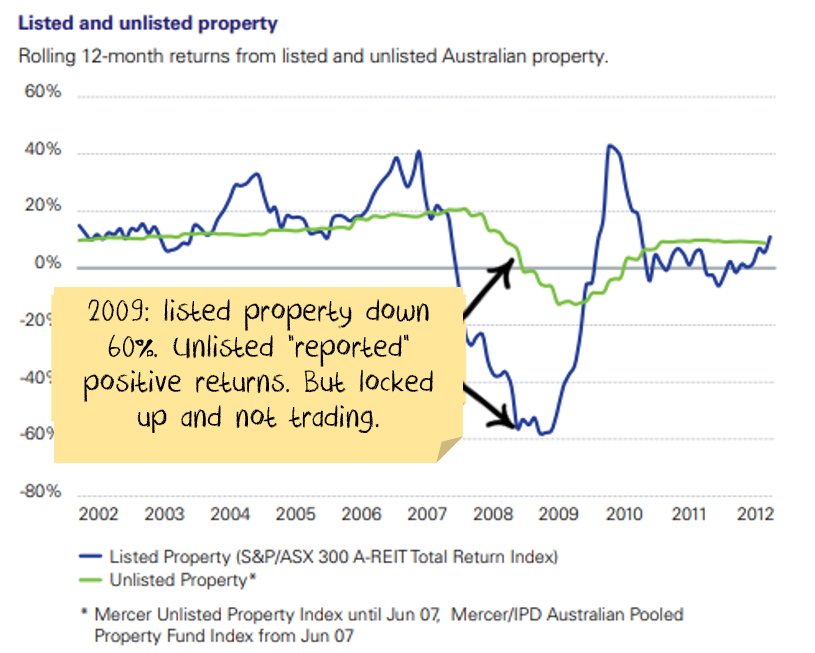

Klassen cited the Global Financial Crisis as a useful example. Then, superannuation funds failed to write down unlisted property to the same degree as listed property, despite holding effectively the same assets:

The obvious first best solution is to require industry superannuation funds to write-down unlisted assets to an accurate value so that those who leave do not shift the cost onto those who stay.

The bottom line is that if you are a member of an industry superannuation fund that holds unlisted assets, be cognisant that if you chose to stay, the value of your investment could very well absorb the losses and could get diluted as members leave. Moreover, this problem will likely be exacerbated as people take up the Morrison Government’s early redemption offer.

Of course, MB provides a superannuation fund with our partners at Nucleus Wealth. Therefore, we are not an unbiased observer.

With that explicit disclaimer, next-generation superannuation funds like ours hold each client’s assets in separately managed accounts. Thus, you do not experience the problem whereby the withdrawals of one investor impacts other investors who are staying put.

——————————————-