Matthew Ross of Goldman Sachs estimates that up to $44 billion could be withdrawn from superannuation funds by people who have been financially hit by the pandemic. This is based on 10% of superannuation members withdrawing $20,000 of funds.

Ross’ estimate compares to the federal government’s forecast withdrawals of $27 billion and the superannuation industry’s estimate of between $50 billion and $65 billion.

Ross contends that the early access scheme could result in liquidity issues for some super funds, which could in turn be forced to reduce their exposure to shares. In turn, this could place downward pressure on share prices and reduce the benchmark S&P/ASX 200’s market capitalisation by around 0.45%.

From Ross:

“The early withdrawal policy will nevertheless leave super funds in a worse liquidity position than before, with over half of the funds largely depleting their cash balances under our $44bn scenario.”

“This liquidity position will be further worsened by the extent of member-switching towards more defensive products, and the fact that illiquid assets may be especially hard to liquidate in the current environment — meaning any future portfolio rebalance will need to come from selling liquid assets.”

It is unknown whether these forecasts have taken into account the full effect of a downturn in employment and wages, which will necessarily also crimp compulsory superannuation inflows. If not, the impacts on liquidity and share valuations could be much worse.

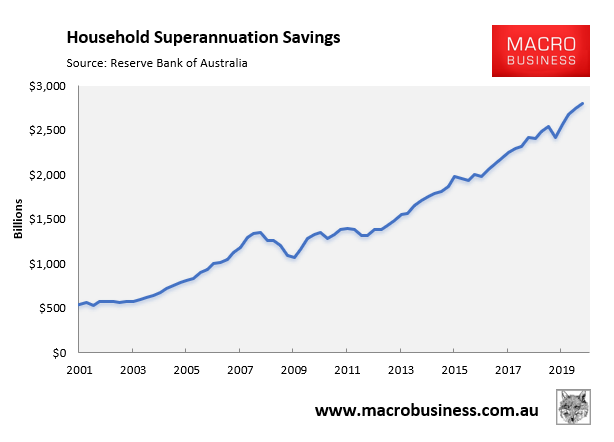

What this analysis also highlights is that the long rise in Australia’s superannuation pool (see next chart) has increased demand and helped drive-up share prices.

That is, mandating Australians to direct 9.5% of their wages into financial markets via the superannuation guarantee necessarily inflates stock and bond prices which, because prices are rising, may also have encouraged others to pile in.

Because of these dynamics, Melbourne University research economist, Warwick Smith, described superannuation as Australia’s first compulsory Ponzi scheme.

Smith warns that with the large baby boomer generation entering requirement age, and needing to draw down on their superannuation savings (to which they hold the lion’s share), this risks deflating share prices.

Therefore, lifting the superannuation guarantee from 9.5% to 12% is a sure fire way to maintain positive net superannuation inflows, thus keeping the superannuation Ponzi going.

The COVID-19 economic collapse, alongside the Morrison Government’s early withdrawal policy, has obviously put a short-term spanner in the works, as illustrated by the widespread liquidity problems experienced by the superannuation industry.