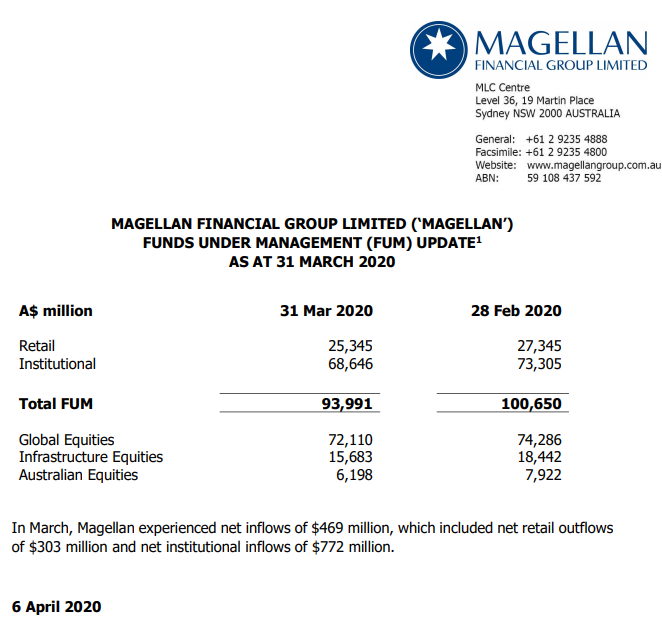

Magellan has reported its FUM flows for March:

From a peak at the end of January, FUM is down roughly 11% (extracted from flows). Magellan has various funds with a very wide variety of performance. The 11% may not be a bad representation of the firm’s aggregate performance for what that’s worth.

It has still done better than many!

For comparisons, the MB Fund international direct shares SMA was -4.8% over the period, clubbing the others like baby seals (past performance is no guarantee of future performance of course).

The Hamish Douglass take on things is reasonable:

The glaring omission in that analysis, which is subsumed by a quaint faith in policymakers in Issue 2, is no recognition of the virus’s impact on debt dynamics and cycle. The shock is plenty large enough to trigger balance sheet shakeouts in:

- US corporate debt;

- European banks;

- China in general;

- and Australian households.

Thus any U-shaped recovery thesis must be leavened by the prospect of a second-round of stress for credit markets and banks as the bad debts of the cycle come to bear. Policymakers can mitigate this but not prevent it.

That presents the prospect of a very long bottom in the “U” or even an “L-shaped” recovery.