Via Fitch:

Fitch Ratings-Sydney-07 April 2020: Fitch Ratings’ downgrade of the Issuer Default Ratings (IDRs) of Australia’s four largest banking groups and their New Zealand subsidiaries to ‘A+’/’F1’ from ‘AA-‘/’F1+’ reflects the agency’s expectations of a significant economic shock in 1H20 due to measures taken halt the spread of the coronavirus, followed by a moderate recovery through 2021.

The ratings on the banks had limited buffers at the previous levels, as reflected in a Negative Outlook on the IDRs, with an economic shock and further profitability weakness as stated downgrade triggers in recent reviews. Buffers are more substantial at the new rating. Nevertheless, further downside risk remains to our baseline case, which is why a Negative Outlook has been retained on the ratings. Details of the actions can be found in the individual Rating Action Commentaries published on 7 April 2020. The affected entities are:

Australia and New Zealand Banking Group Limited

– ANZ Bank New Zealand Limited

– Senior debt issued by ANZ New Zealand (Int’l) Limited

Commonwealth Bank of Australia

– ASB Bank Limited

– Senior debt issued by ASB Finance Limited

National Australia Bank Limited

– Bank of New Zealand

– Senior debt issued by BNZ International Funding Limited

Westpac Banking Corporation

– Westpac New Zealand Limited

– Senior debt issued by Westpac Securities NZ LimitedFitch has revised the outlook on the operating environment score for banks in both Australia (aa-) and New Zealand (a) to negative from stable as part of this action. The agency expects GDP to shrink in both markets in 1H20, with only a modest recovery starting in 2H20 and extending into 2021. Unemployment is likely to spike sharply and remain very elevated relative to pre-pandemic levels even after the recovery is underway. The current operating environment scores incorporate this base case and the outlook on this factor would likely be revised to stable should the baseline case scenario eventuate. Conversely, a significant extension of the downturn into 2H20, or only a shallow recovery that results in much weaker economic conditions through 2021 and beyond could result in a reduction of the score in both markets. The implications, per Fitch’s criteria, are that we would expect banks to maintain stronger financial profiles – particularly for key financial metrics – than is the case with an operating environment assessment in the ‘aa’ category.

We expect these conditions to affect asset quality and earnings in particular, with the mid-points of both factors reduced by a notch for the large Australian banks, with negative factor outlooks. Support measures implemented by the government, regulators and banks themselves should alleviate some of the asset-quality pressure that will emerge from this downturn, particularly within the next six to 12 months.

However, we expect that a portion of businesses will fail to restart once the recovery begins and some households will not be able to resume debt repayments after the repayment holidays provided by the banks. As a result, asset-quality metrics will likely weaken from current levels over the next 12-18 months and, for the four large Australian banks, we expect them to no longer be consistent with a ‘aa-‘ factor score. Stage 3 loans ranged from 0.9% to 1.3% of gross loans at the most recent year-end for these banks. Fitch’s typically expects these ratios to be sustainably under 1% to be consistent with a score in the ‘aa’ range, although the Australian and New Zealand banks benefit from a high level of secured lending, which should help limit losses.

Earnings will face pressure from both higher impairment charges and lower interest rates. The central banks in Australia and New Zealand have cut their respective cash rates to 0.25% and indicated that they will remain there for a prolonged period. The banks’ earnings were already vulnerable before the pandemic hit, which was reflected in the negative outlook on the factor. The challenges from the outbreak are likely to exacerbate this pressure.

Capitalisation of these banks will be affected by the weaker asset quality, but buffers built in recent years should be sufficient at current scores under our baseline case, and we have retained a stable outlook for this factor. Funding and liquidity is supported by sound liquidity management and the significant support provided by the Australian and New Zealand central banks, with limited short-term pressure likely. The outlook for this factor remains stable as a result. The funding and liquidity scores for all banks are already lower than their respective Viability Ratings reflecting a high reliance on offshore wholesale funding.

Fitch reviewed the four large banks in Australia and New Zealand ahead of the rest of the portfolio as the outlooks on the IDRs were already Negative, indicating greater susceptibility to a downgrade at their relative rating levels and a higher likelihood that they would hit previously stated downgrade sensitivities. In addition, the banks combined account for a significant majority of banking system assets in both markets. We will review the remaining Australian and New Zealand banks rated by Fitch in the near future.

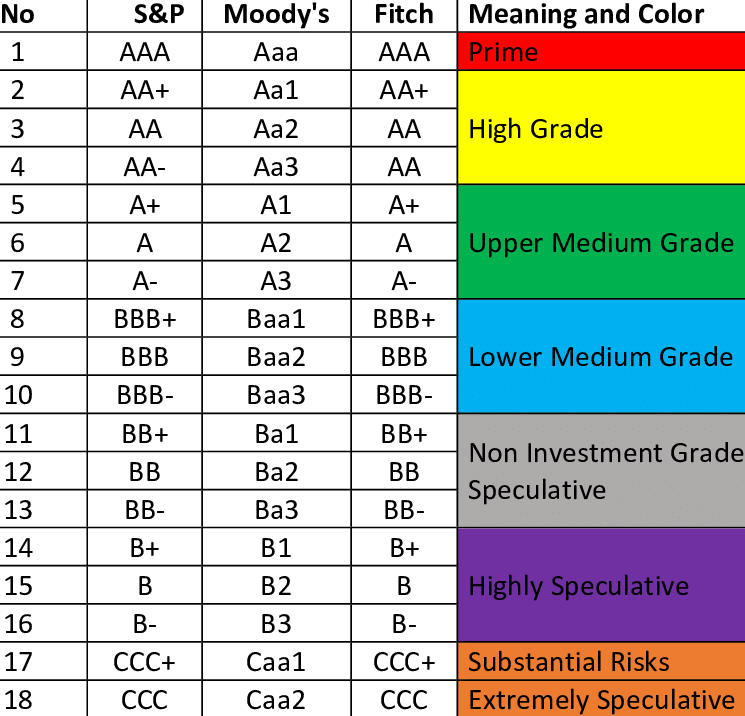

The crisis has been running for two months and the ratings are gone with negative watch for more. The big four are now medium grade only:

By the time this is over, Australian credit will be swimming in the toilet.