By Gareth Aird, senior economist at CBA:

Key Points

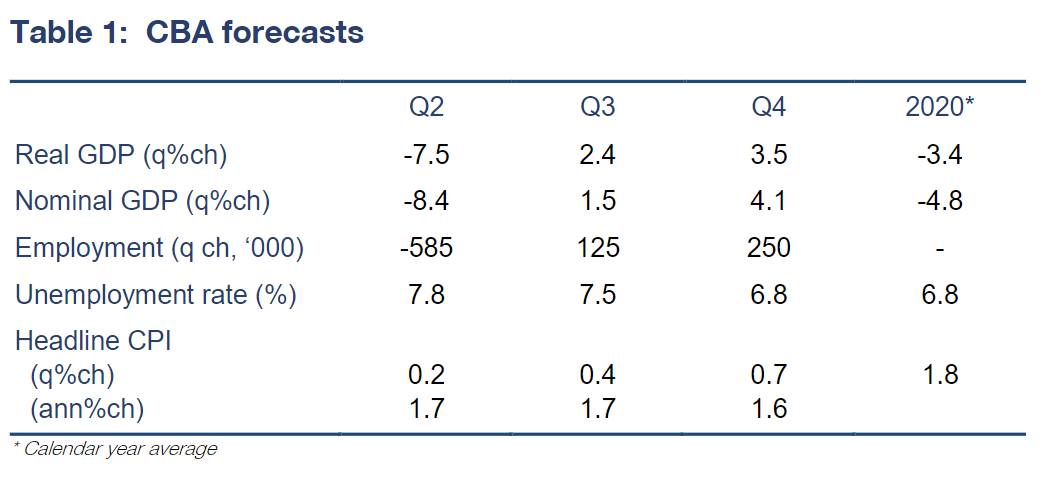

- We expect the Australian economy to contract by 7.5%/qtr in Q2 20 and by 3.4% in 2020.

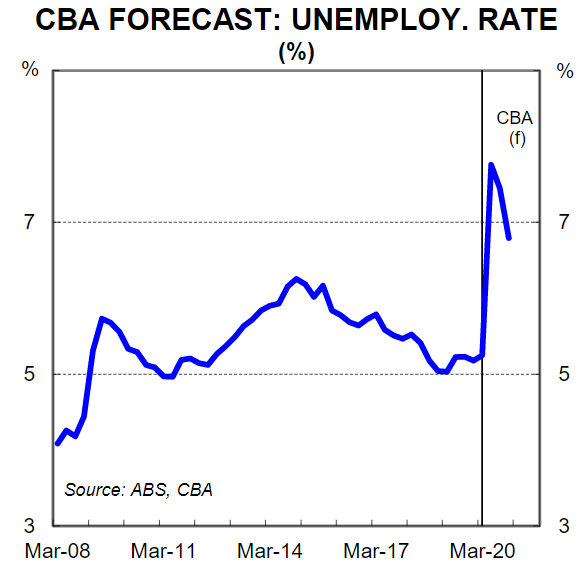

- The unemployment rate is forecast to lift sharply to 7.8% in Q2 20.

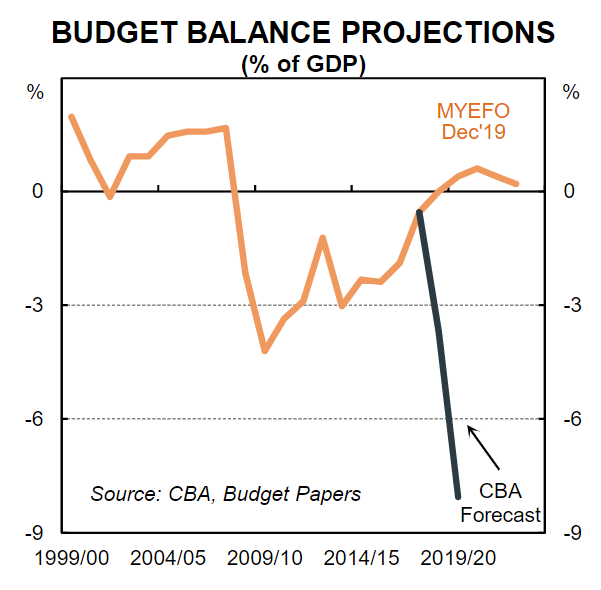

- We expect the Commonwealth fiscal position to deteriorate to a deficit of $A72bn in 2019/20 (3.7% of GDP) and to $A155bn in 2020/21 (8.1% of GDP).

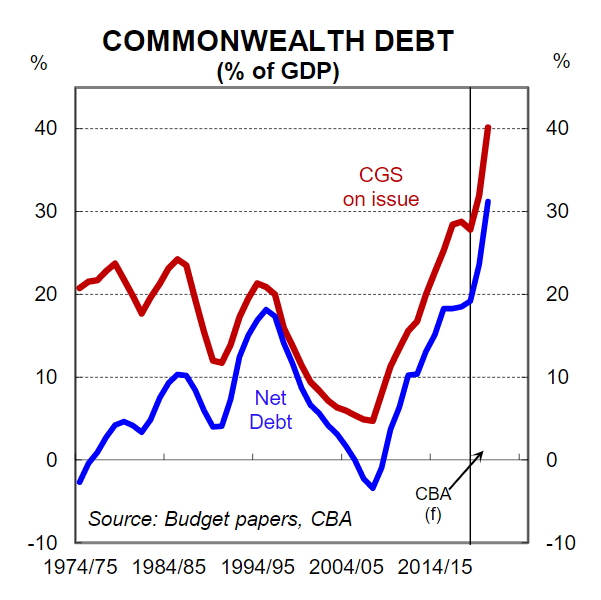

- Total Australian Government bonds outstanding rises to ~$A790bn or 40% of GDP by 2020/21 (compared with the estimate in the 2019 MYEFO of $A558bn or 27% of GDP).

Overview

The Australian economy is in the midst of an extraordinary set of circumstances. Policymakers have shut down entire parts of the economy to limit the spread of COVID-19. At the same time an unprecedented amount of fiscal and monetary stimulus, as well as industry support, has been unleashed to support households,businesses and the community through this period.

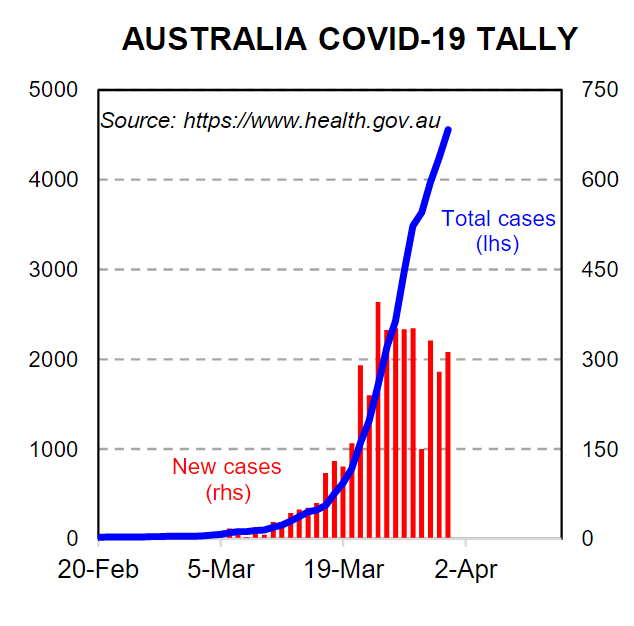

Developments over the past three weeks have created a lot of uncertainty around the path of output and unemployment, particularly as the depth and duration of the enforced shutdown and self-isolating period is unknown. Notwithstanding, it is clear that a significant proportion of the domestic economy will remain shut in some capacity through the June quarter and most likely the early part of the September quarter.

In this note we update our forecasts for GDP, the labour market and the Commonwealth fiscal position. We take a bottom up approach to our forecasts for Q2 20 GDP and the labour market given the unique set of circumstances surrounding the economy. All economic downturns are different, but an enforced shutdown of significant parts of the economy to combat the spread of a virus is unprecedented in modern times.

We should stress that no economist has a crystal ball and forecasting is an inexact science. It is a tricky art at the best of times and right now it is incredibly challenging.We have refrained from publishing updated forecasts until now as the landscape has changed on an almost daily basis. Indeed some of the policy decisions have meant radical revisions to forecasts. However, it appears as though the dust has settled a little and the picture is a bit clearer. As such,our new forecasts are enclosed.We should stress that the overall story is more important than our point forecasts and the shape of our profile is what readers should focus on.

Output

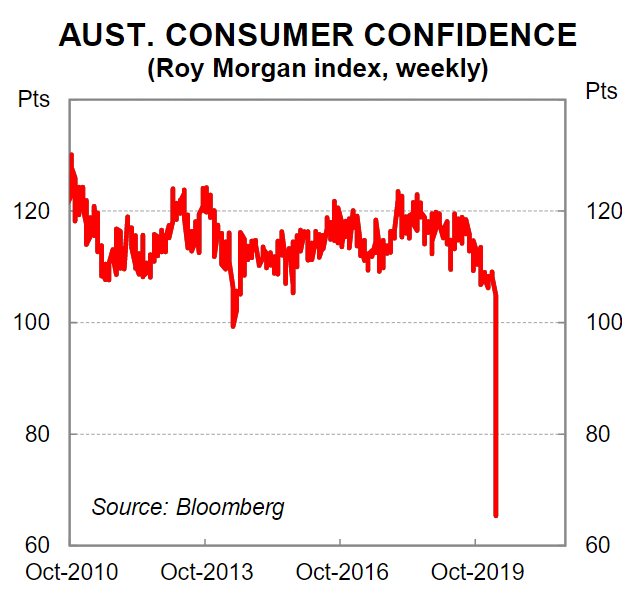

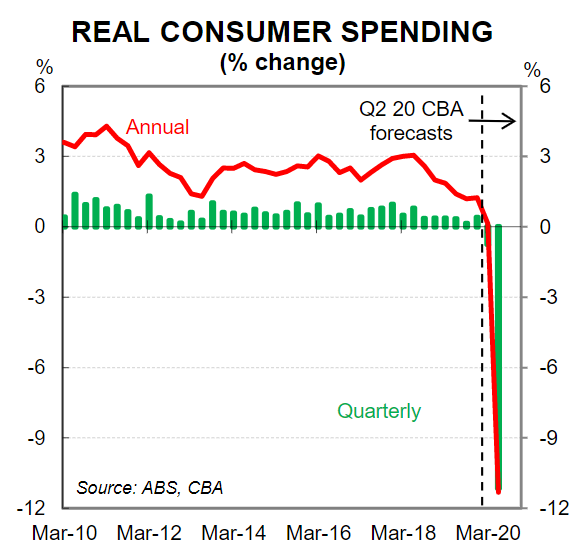

The key component in our GDP forecast over Q2 20 is household consumption. Household consumption makes up close to 60% of GDP. Our base case is for household consumption to contract by ~11% over the quarter. Spending on both discretionary and non-discretionary goods and services is expected to fall significantly due to the enforced shut down. It is simply not possible for households to consume a range of goods and services at present because the businesses that provide them are closed and people are largely staying at home. The enforced shut down and social distancing measures results in job losses, which further weighs on consumer spending via a negative feedback loop. And while the government is providing an extraordinary amount of support to households, uncertainty around employment and the economy, which has seen consumer sentiment plunge, also means that consumers are likely to rein in their spending.

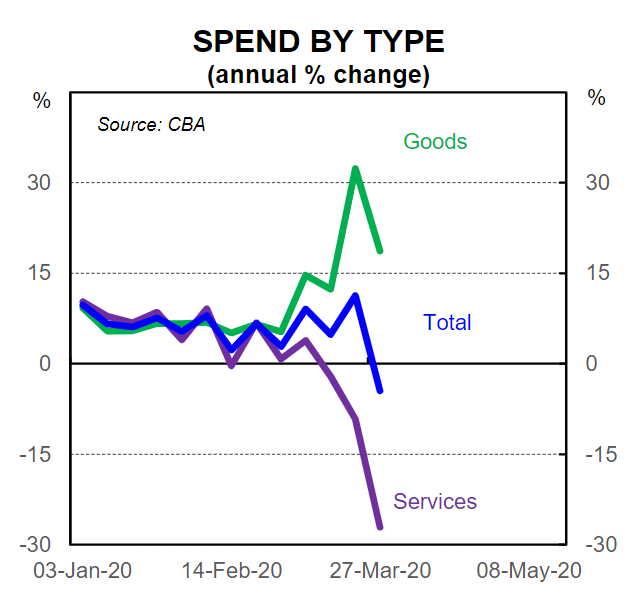

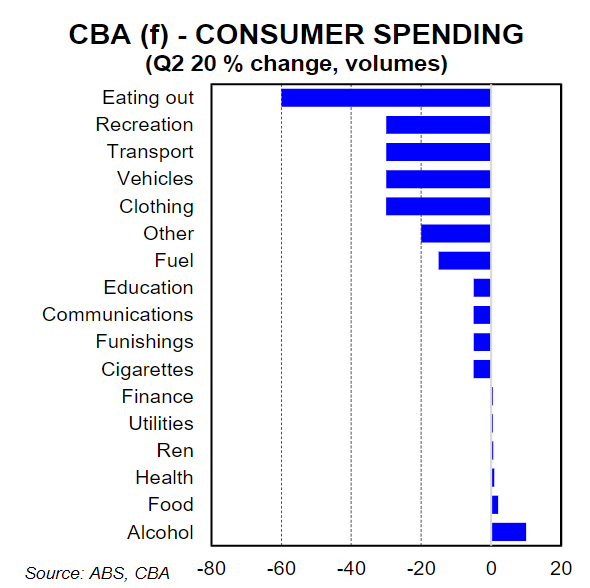

We expect to see the largest fall in the eating-out category. Restaurants, cafes and hotel shave been limited to just takeaway since late March. Our forecasts have activity in this category sitting at around one third of its normal level in Q2 20. There are downside risks to our forecast. Recreation, transport, purchases of vehicles and clothing are also expected to post very large falls in the June quarter. Household furnishings & equipment will be hit by a sharp fall in housing turnover. Although there is likely to be some cushioning from people undertaking home DIY renovations and maintenance.

There are some partial offsetting forces to the categories that contract. We expect spending in some categories to increase in the quarter (see chart opposite). Food and alcohol are likely to show the largest gains. Our CBA credit and debit card data has shown that spending is rocketing higher in these two categories as consumers stockpile and substitution takes place. The enforced shutdown means people are now mostly eating and drinking at home.

Business and dwelling investment will also fall, while public consumption will remain a support to the economy. Both imports and exports are forecast to be lower so the overall impact on growth from the external sector will be small relative to the big hit expected on domestic demand.

At this stage we expect the economy to remain at least partially shut in Q320, particularly as colder weather in winter is likely to increase the ease of transmission of COVID-19. But it is reasonable to assume that some restrictions may be relaxed towards the end of the September quarter. As such, we have pencilled in a lift in growth of 2½% in Q3, but note that there is a very high degree of uncertainty as to how the situation will evolve. If further restrictions are imposed on activity then GDP will naturally be lower than we envisage. That is not our base case, however.If the economy is further opened in Q4 20 then we would expect a more significant rebound in activity and growth. Our central scenario for the economy therefore takes a U shape.Overall GDP is forecast to decline by 3.4% in 2020.

Labour market

Australia entered the COVID-19 crisis with an unemployment rate close to 5% and a natural rate of unemployment rate of 4½%. Past recessions indicate that unemployment rises more when there is a bigger degree of slack in the labour market. However more recent economic downturns have seen less labour shedding due to more flexibility in the labour market.

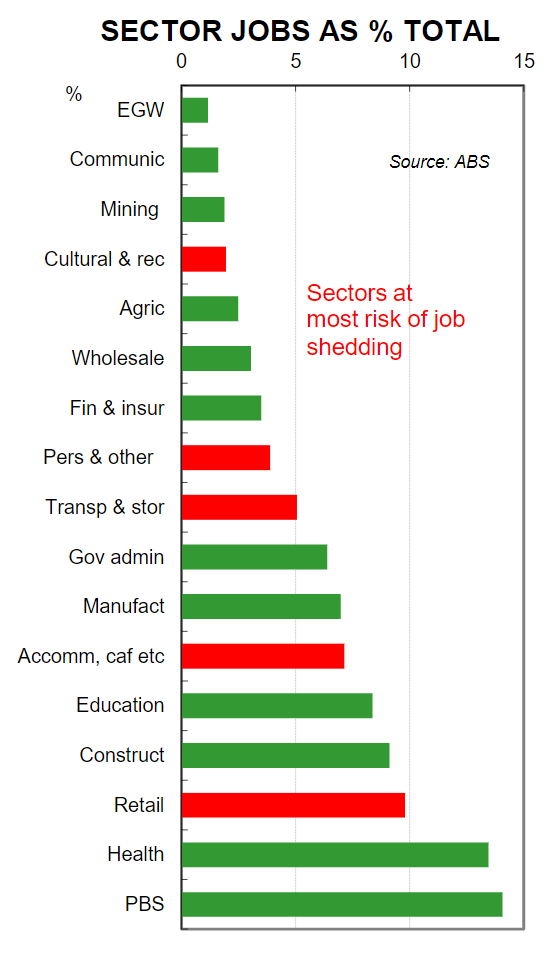

The labour market will be profoundly impacted in several ways: employment will drop, unemployment and underemployment will rise, participation will dip and hours worked will contract sharply. These trends are already in play. We have already seen significant job shedding in retail, accommodation & cafes, air transport and we expect more in personal services and recreation as certain parts of the economy remain shut and the prevalence of self-isolation increases.

The sectors most exposed to job shedding account for 23% of the labour market, roughly 3 million people. Other sectors will be exposed as a contraction in economic activity occurs. Industry anecdotes suggest there have already been over 120,000 workers stood down in the Australian economy as at the end of March. More job losses will come.

Our forecast for employment and unemployment is complicated by the JobKeeper payment which shifts the paradigm for the labour market (see here). In short, the JobKeeper allowance will mute the rise in the unemployment rate. But it won’t be enough to fend off all job losses. In particular, workers who have been with their employer for less than 12 months are not covered by JobKeeper.And it still remains the case that many businesses will struggle financially to remain viable over the next six months as wages are not the only cost of running a business. Nonetheless, the cost of labour for firms that can switch their wage costs to JobKeeper will drop to zero (or close to zero depending on other arrangements between a worker and their employer). This is an extraordinary incentive for businesses to retain staff over the next six months as the economy contracts.

Our forecast is for total job losses in the June quarter of ~580k. But the fall in the level of employment will be bigger than the rise in unemployment because we expect participation in the workforce to dip. Our forecast is for the participation to drop by 1.5ppts to 64.5% which would see the unemployment rate peak at 7.8%.

Participation will drop because there will be a significant proportion of people who will lose their jobs, but they will temporarily drop out of the labour force (i.e. they will not fall in the category of either employed or unemployed). These will be people who will choose not to actively look for work either because: (i) there are no job openings in their profession given the enforced shut down (e.g. bartender, flight attendant); (ii) they are older workers concerned about the health risks remove themselves from the workforce; or (iii) they are parents who decide the challenges of home schooling require one parent at home.The doubling in JobSeeker is likely to result in more people who lose their jobs not looking for employment over the shutdown period than would otherwise be the case.Please see page 4 for our more detailed thinking on the labour market.

Commonwealth Budget

The Commonwealth budget will be hit materially by both the impact of COVID-19 on tax receipts and the cost of the stimulus packages. Revenue will drop significantly and growth in expenditure will accelerate meaning a twofold blow to the fiscal balance.

Based on our profile for nominal GDP, unemployment and the cost of the stimulus packages, we expect the budget position to worsen from a broadly balanced budget in 2019/20 to a deficit of $A72bn (3.7% of GDP). The arithmetic is a fall in revenue of $A12bn and an increase in expenditure of $A66bn. In 2020/21 our fiscal model is pointing to an incredible deterioration of $A161bn in the budget to a deficit of $A155bn (8.1% of GDP). The arithmetic is a shortfall in revenue of $A35bn (compared to the 2019 Mid-Year-Economic-&-Fiscal Outlook (MYEFO) position) and an increase in expenditure of $A126bn (based on the cost of the stimulus packages). These numbers see total Commonwealth government debt increase by ~$A240bn (12% of GDP). Total Australian Government bonds outstanding would rise to ~$A790bn or 40% of GDP by 2020/21 (compared with the estimate in MYEFO of $A558bn or 27% of GDP). Net debt on our forecasts would lift to 28% of GDP in 2020/21 (compared with the estimate in MYEFO of 18½% of GDP). Please note that the Australian Office of Financial Management (AOFM) is expected to announce a new borrowing profile this week.

The Australian labour market – Some further thoughts

Australia entered the COVID-19 crisis with an unemployment rate close to 5% and a natural rate of unemployment rate of 4½%. Past recessions indicate that unemployment rises more when there is a bigger degree of slack in the labour market. However, more recent economic downturns have seen less labour shedding due to more flexibility in the labour market. Employers are more inclined to vary conditions (i.e. hours worked) rather than job shed. Wages are also more responsive to labour demand in a less unionised labour market. This time, of course, is different. The expected sharp contraction in economic activity is closer to a depression than a recession. But the policy response, particularly the JobKeeper payment, is unprecedented. It has been introduced to keep workers tied to employers as the Australian economy enters a period of hibernation.

JobKeeper will limit the rise in unemployment because many firms who could not afford to retain staff due to a drop in sales as a result of COVID-19 will now be able to do so. In essence, the cost of labour for impacted firms will drop to zero (or close to zero depending on other arrangements between a worker and their employer). This is an extraordinary incentive for businesses to retain staff over the next six months as the economy contracts primarily due to the imposed shutdown/s. So on that score we can expect less damage done to the labour market than otherwise. However the payment is capped at $A1500 so we could see those workers earning more than that have their terms of employment altered to reduce the cost to the business. This would see hours worked fall and underemployment rise.

The OECD notes that a quarter of Australia’s workforce is casual. As at December 2019 there were a total of 2.5m workers who had been with their employer less than 12 months. If one quarter of those workers are casuals, in line with the broader employment breakdown, the number of casual jobs at risk is 575k. There is no incentive for businesses to employ these casual workers if there is no demand. If all casual workers employed for less than 12 months lost their job, with an unchanged participation rate of 66%,then the unemployment rate would be 9.3%.

That situation is unlikely though as casuals in some industries will continue to be employed. There are also employment opportunities in some industries that are lifting headcount – i.e. food retailers, logistics, health and the government sector. Reducing this number to compensate for these industries and a reasonable level of casual workers would see an unemployment rate of over 8%. That is still higher than our point forecast of 7.8% because growth in the labour force will slow.

Net overseas migration will be largely non-existent due to Australia’s border closing. This will see population growth slow to 0.6%/yr in Q3 20 (down from 1.5%/yr). This means slower growth in the labour force and a reduction in the number of jobs needed to be created each month on an unchanged participation rate to keep the unemployment rate steady. But the participation rate will also fall. There will be a significant proportion of people who will lose their jobs, but they will temporarily drop out of the labour force (i.e. they will not fall in the category of either employed or unemployed). These will be people who will choose not to actively look for work either because: (i) there are no job openings in their profession given the enforced shut down (e.g. bartender, flight attendant); (ii) they are older workers concerned about the health risks remove themselves from the workforce; or (iii) they are parents who decide the challenges of home schooling require one parent at home. The doubling in JobSeeker is likely to result in more people who lose their jobs not looking for employment over the shutdown period than would otherwise be the case.

As a result we expect to see the participation rate drop by 1.5ppts to 64.5%. This will help to mitigate the rise in the unemployment rate. We also expect to see a lift in the underemployment rate as workers hours are cut. When we add the unemployment rate and the underemployment rates together we get the underutilisation rate. This peaked at 18% during the 1990s recession. We expect to see these levels tested again.