By Gareth Aird, senior economist at CBA:

Key Points

- COVID-19 will have a material negative impact on Australian residential property prices.

- Momentum in the property market has plunged and new lending, turnover and prices are all forecast to fall over the next six months.

- We expect Sydney and Melbourne property prices to underperform against the national benchmark.

Overview

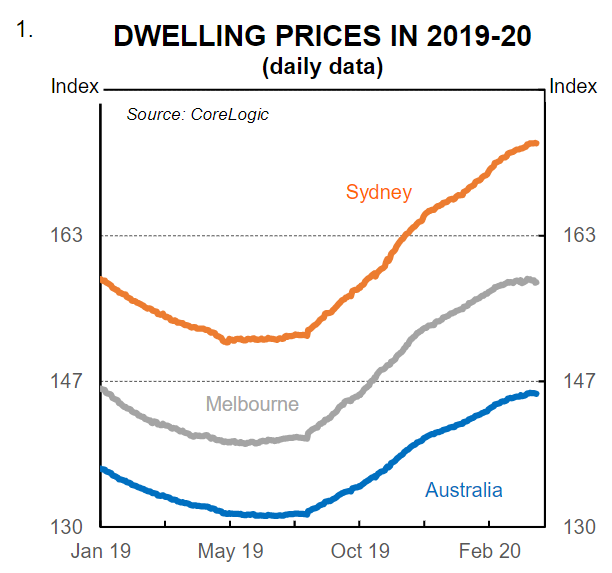

Australian capital city dwelling prices, led by Sydney and Melbourne, have risen strongly over the past nine months (chart 1). But we expect that stellar run to end abruptly. The policy response to limit the spread of COVID-19 has created a plunge in economic activity and unemployment will spike. This will have profound short term consequences for the housing market. As a result, we have materially downwardly revised our expectations for Australian residential property prices.

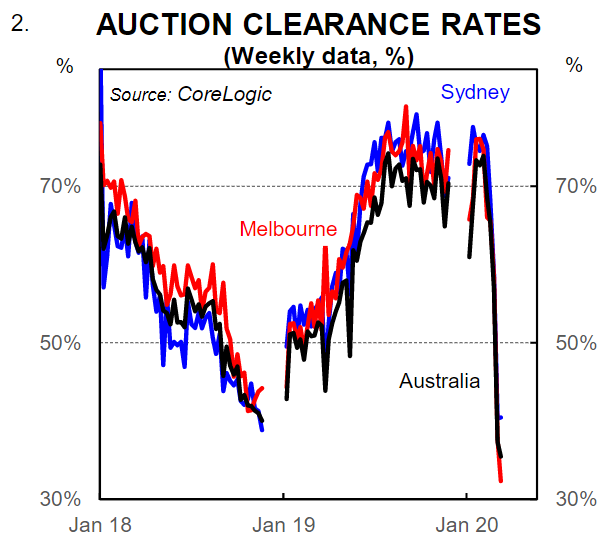

It is our view that prices will fall sharply over the next six months. New lending is expected to contract, buyer expectations have adjusted downwards from exuberance to pessimism, rents are likely to fall, auction clearance rates are expected to remain weak and turnover will be lower than usual. In addition, the usual underlying demand pulse from net overseas migration has evaporated because the border is shut. The net result means that price declines are inevitable. The extent to which prices fall will largely be determined by the magnitude of the lift in unemployment and the length of time that the government-imposed restrictions on day-to-day activity remain in play.

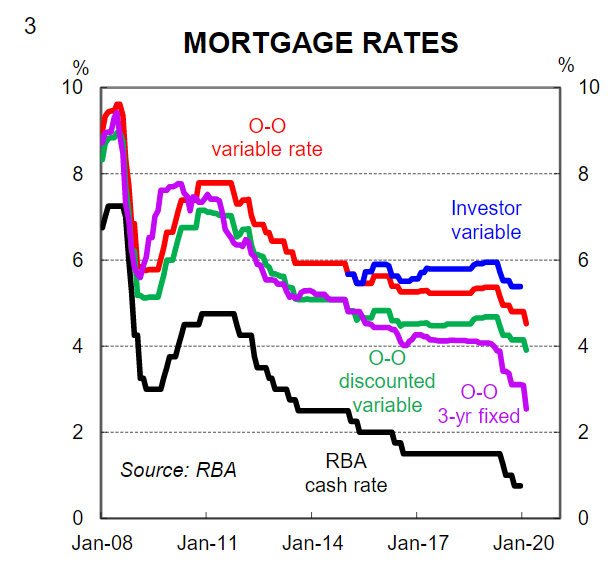

The forces are not all one way, however. Aggressive monetary policy easing has resulted in record low variable and fixed mortgage rates, which acts as a support to dwelling prices (chart 3). And debt relief via deferred home loan repayments for impacted households will mean less distressed sales arising from job losses than would otherwise be the case.

This note outlines our views on dwelling prices, our underpinning assumptions and the risks to our forecasts. Our quantitative assessment of the residential market, overlaid with our qualitative views, means that we now expect national property prices to fall by around 10% over the next six months (i.e. 20% annualised). We would caution, however, that there is a great deal of uncertainty at present and there are scenarios where prices could fall by both more or less than we expect.

Within the mix there is likely to be variation in outcomes by capital city. More specifically, we expect Sydney and Melbourne to underperform relative to the national average. The NSW and Victorian economies have more exposure to the most heavily impacted services sectors and less exposure to some of the more insulated sectors (i.e. mining and agriculture). In addition, the Sydney and Melbourne housing markets are more reliant on strong population growth, particularly by immigration, to underpin demand.

Recent story

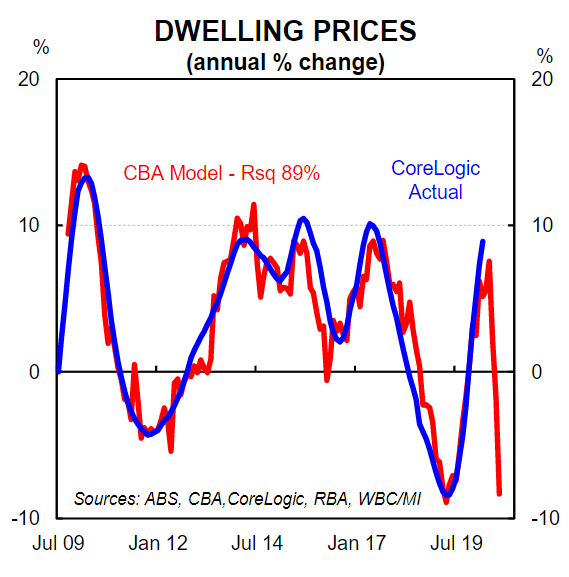

National dwelling prices have risen strongly since mid-2020. Dwelling prices were 8.9% higher over the year to March. Price rises have been greatest in Sydney (13.0%/yr) and Melbourne (12.0%/yr). The reasons behind the surge in prices have been well documented: RBA interest rate cuts, coupled with extra borrowing capacity from the APRA induced changes to loan serviceability assessment and a surprise election outcome that removed some taxation risks around housing.

All of these factors still remain in play. But the bigger issue of COVID-19 and its impact on the Australian economy supersedes them. At this stage the daily CoreLogic residential price data, which is the industry benchmark, has not turned downwards. But other timely indicators of the property market have moved sharply lower. We expect the CoreLogic daily dwelling price data to turn down very soon.

Why will prices fall?

In summary, there are five reasons why dwelling prices will fall:

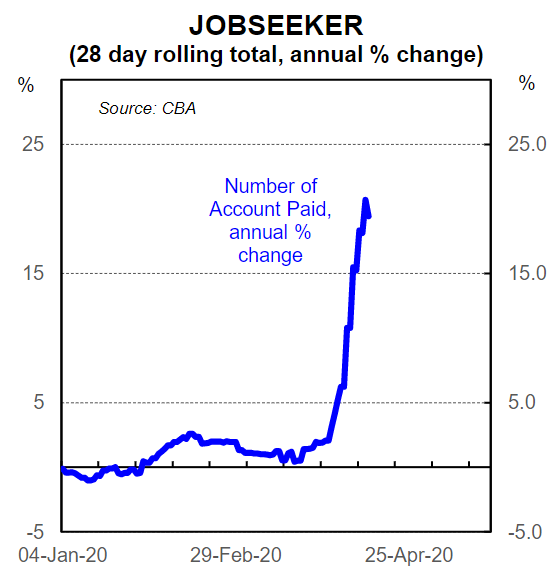

(i) Unemployment is rising very quickly. The government enforced shutdown has led to mass job losses. The ABS official figures are dated and do not capture the big lift in unemployment that has occurred since mid-March. Our internal data on unemployment benefits (i.e. JobSeeker) paid to CBA accounts shows that there has been a surge in the number people receiving JobSeeker payments (chart 4). This will continue to rise given the lag between applying for JobSeeker and receiving payments. We expect the unemployment rate to peak at ~8%.

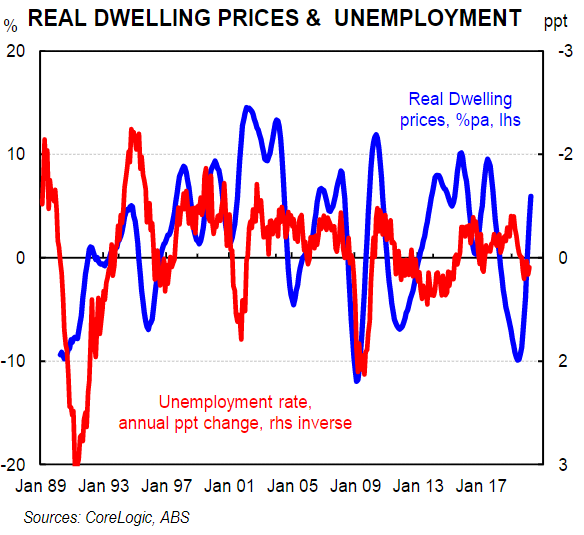

It is not always the case that rising unemployment leads to falling house prices. And in some instances the housing market tends to lead the labour market rather than the other way around. However, a shock to the labour market of this magnitude will put significant downward pressure on dwelling prices. By way of comparison, during the 1990s recession the unemployment rate peaked at 11%. Dwelling prices fell by 6.2% over a 20 month period. But inflation was a lot higher over that period than it is today. In real terms, i.e. adjusting for inflation, house prices fell by ~15% over a 20 month period (chart 5).

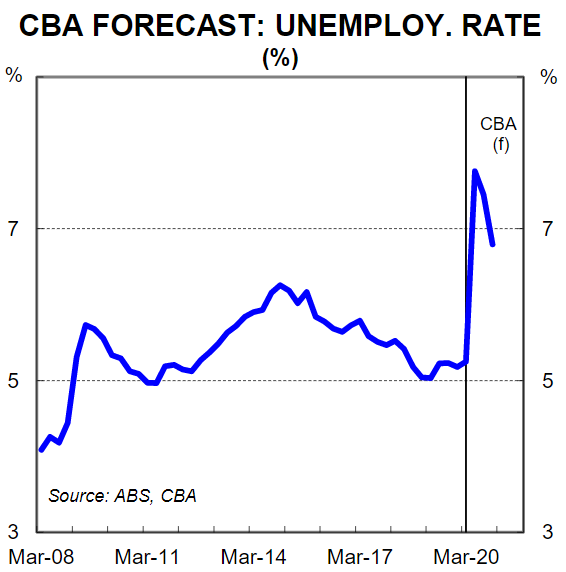

The profile for the unemployment rate is expected to be quite different this time around. It will rise very quickly, but should start falling over the second half of 2020 (chart 6). The sudden spike in unemployment will mean the impact on the property market is immediate but should not be as long lasting.

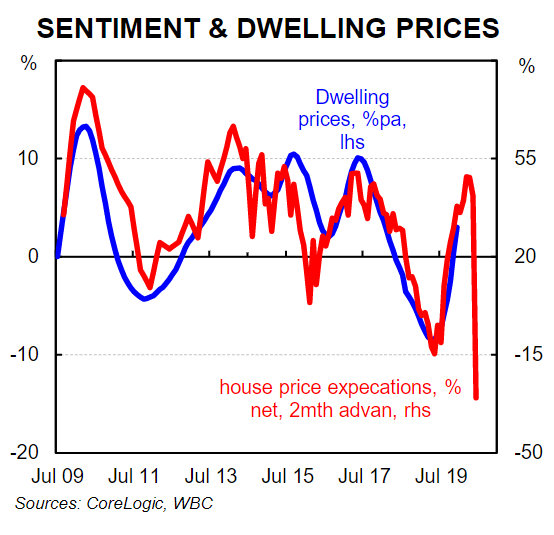

(ii) The household perception around prices has shifted dramatically. According to the AprilWBC/Melbourne Institute Consumer Sentiment report, the proportion of households expecting dwelling prices to rise over the next twelve months has plunged to its lowest level since the question was first asked in late 2009(chart 7). This index has historically had a very strong leading relationship with dwelling prices. If households as a collective expect prices to fall then they will.

(iii) The rise in unemployment will put downward pressure on rents. Falling rents generally mean falling prices. In addition, there is significant uncertainty right now over the contractual obligations between a tenant and their landlord because policy changes are occurring at the state level. In NSW, for example, the government has introduced an interim 60-day stop on landlords seeking to evict tenants due to rental arrears as a result of COVID-19, together with longer six month restrictions on rental arrears evictions for those financially disadvantaged by COVID-19. To be clear, we are not questioning such policy changes. But rather we are highlighting how short term intervention in the housing market that changes the existing governance and contractual obligation between landlords and tenants will act as a major deterrent over the next six months from would-be investors.

(iv) Foreign investment in Australian property is likely to drop to close to zero during the enforced shutdown. To be fair, the foreign investor share of property purchases has fallen over the past few years. But there has still been foreign buyers which adds to aggregate demand for housing and supports dwelling prices.

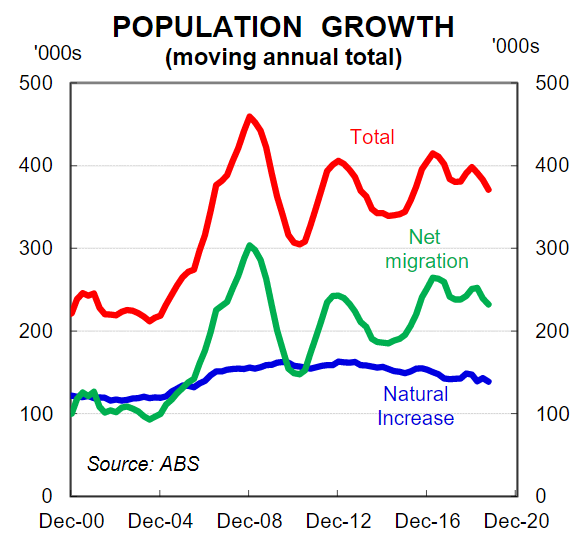

(v) Net overseas immigration has effectively dropped to zero because the border is shut. We would envisage that the border is only reopened once all of the restrictions on the domestic economy have been lifted. That looks to be some distance away. There are implications for the housing market because Australia’s population growth has been very strong over the recent past because of the high migrant intake each year (chart 8).

Everybody needs a roof over their head and the strong level of net overseas migration has added significantly to the demand for housing. Indeed strong population growth has also kept vacancy rates in most capital cities anchored despite the boom in apartment construction across Australia. The rapid halt to net overseas migration is a material negative demand shock to the Australian property market. It will have an impact on both prices and residential construction.

How far will prices fall?

Forecasting is a tricky art at the best of times and right now it is incredibly challenging. Indeed predicting property prices can look foolish retrospectively and right now it is verging on the impossible given all of the dynamics at play. Nonetheless, we have input the latest leading indicators of the property market into our model as a starting point and the results tell their own story (chart 9).

The model puts the annual change in national dwelling prices as a function of the annual change in mortgage rates (1 year advanced), the annual change in the flow of credit (six months advanced), auction clearance rates (four months advanced) and the house price expectations index from the WBC/MI Consumer Sentiment survey (2 months advanced). The collapse in auction clearance rates and house price expectations has led to the model estimate of home prices plunging.

When we overlay the model driven results with a qualitative assessment of the housing market based on our assumptions1for the economy (GDP -7.5%/qtr Q2 20, unemployment rate to rise to ~8%) we have a central scenario that national dwelling prices contract by 10% over the next six months (i.e. average monthly falls of ~1¾%and an annualised pace of 20%). We would then expect prices to stabilise before gradually rising as the unemployment rate begins to decline and restrictions on activity, including the housing market, are eased. It is possible that prices rise briskly in 2021as was the case from mid-2019 given the incredibly low interest rates.

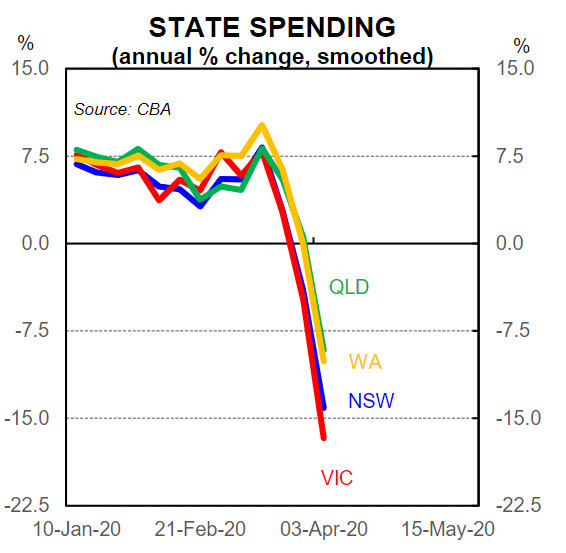

Table 1 details our point forecasts by capital city. We expect both Sydney and Melbourne to underperform relative to the national benchmark. Both NSW and Victoria have more exposure to the most heavily impacted services sectors and less exposure to the more insulated sectors (i.e. agriculture and mining).Indeed our latest internal data shows that the biggest annual declines in CBA credit and debit card spending are in Victoria and NSW (chart 10). In addition, the Sydney and Melbourne housing markets are more impacted by the abrupt temporary halt to net overseas migration as well as the expected fall in foreign demand.

Risks

There are both downside and upside risks to our dwelling price forecasts. The risks both hinge on the length of the enforced shutdown and restrictions placed on economic activity.

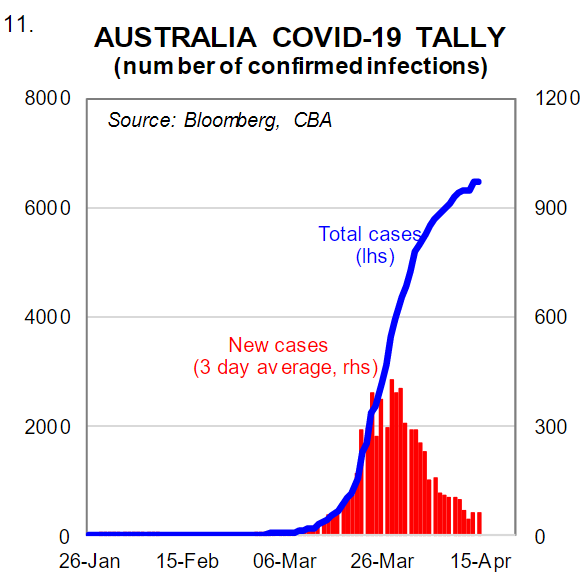

In a best case scenario government restrictions on economic activity could start to be lifted by the end of May. For that to occur, it would probably take several days of zero or very low community transmission of new COVID-19 cases. That is a possible scenario given the current trend in new COVID-19 cases (chart 11).

If that were to occur the plunge in economic activity that we expect would not be as large and the impact on the property market would not be as severe. Indeed the fall in property prices would be significantly smaller than our central scenario, particularly given the extraordinary low borrowing rates currently on offer.

There are scenarios, however, that are significantly worse than our central scenario. If restrictions are eased in Q3 20, as we expect, but a second round of COVID-19 new cases emerge then both the economy and housing market would be adversely impacted again. We would see restrictions return but the hit this time around on the economy and labour markets would be more significant and the damage would be longer lasting. Falls in dwelling prices far greater than our central scenario would be plausible. We believe that policymakers will be acutely aware of the risk of this scenario and as a result they will take a cautious approach to reopening the economy.

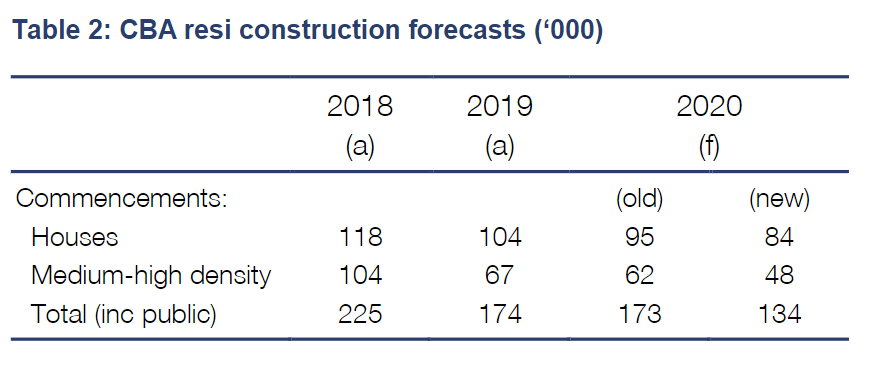

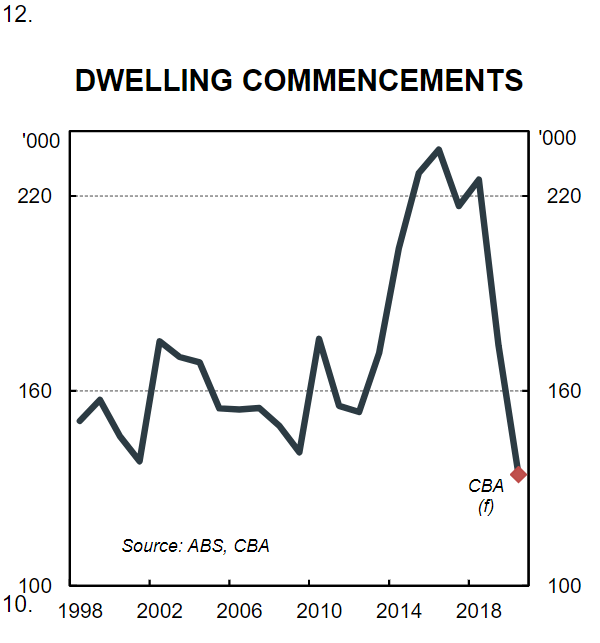

Housing commencements

Residential construction will also be impacted by COVID-19. The combination of rising unemployment, falling dwelling prices and a halt to net overseas migration will see dwelling commencements slow significantly in 2020 (chart 12). Our new forecasts for dwelling commencements in 2020 are tabled below: