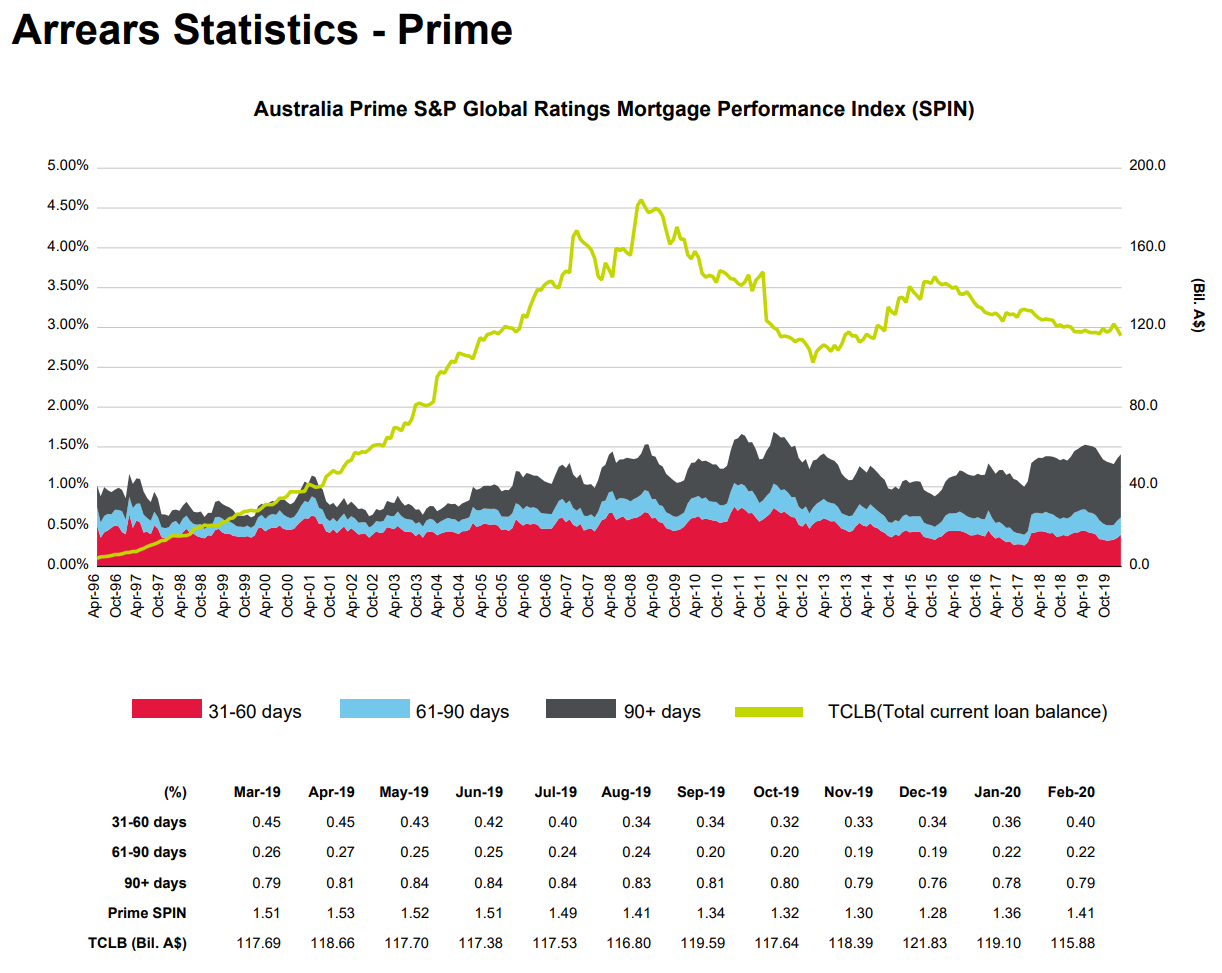

The Standard & Poor’s Performance Index (SPIN) for Australian prime mortgages increased to 1.41% in February from 1.36% a month earlier. Arrears typically rise in February, reflecting the end of the summer holidays and post-Christmas spending period.

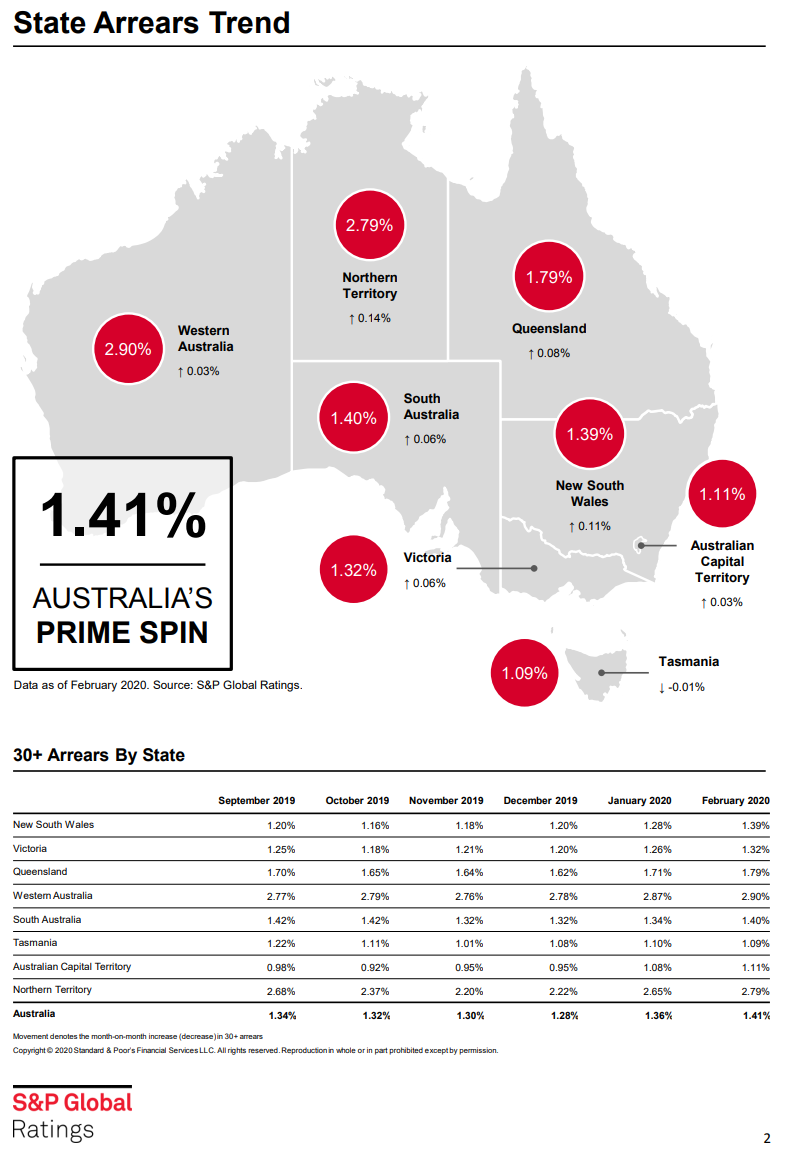

Increases in arrears were more pronounced in New South Wales, Queensland, and Victoria, reflecting the effect of bushfires, drought, and a decline in international tourism in larger coastal areas after the onset of the COVID-19 pandemic.

Social distancing measures to slow the spread of the virus did not come into effect until mid-March, meaning the effect on mortgage arrears won’t be reflected until future reporting periods. Data for April and, to a lesser extent, March will provide some insights into COVID-19’s effect on borrowers’ debt serviceability since the large disruptions to business activity.

Many lenders are offering a variety of temporary mortgage payment relief measures to borrowers whose income has been affected by the COVID-19 pandemic. The true effect of increased financial hardship due to COVID-19 will not be reflected in traditional arrears reporting until at least the third quarter of 2020. This is because lenders are not required to report loans under COVID-19 arrangements as being in arrears during the defined mortgage-relief period.

Many lenders are adjusting their reporting systems to track the level of COVID-19 hardship applications and the duration of these arrangements, however. Based on initial observations from data provided by some lenders, around 3% to 7% of loans in securitized trusts are under COVID-19 hardship arrangements. We expect the level to increase in the coming months, but the rate of increase will likely slow, and depend upon the economic path to recovery.

The large forecast increases in unemployment for 2020 will lead to rises in arrears and defaults in the next 12-18 months, albeit from low levels. Mortgage payment relief measures will help to cushion some of the effects of rising unemployment on households’ debt serviceability. A longer path to economic recovery could diminish the efficacy of these measures over time, though.

Expect it to be worse than S&P thinks and more enduring. Extend and pretend will stretch out the distress and impact on bank profits.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.