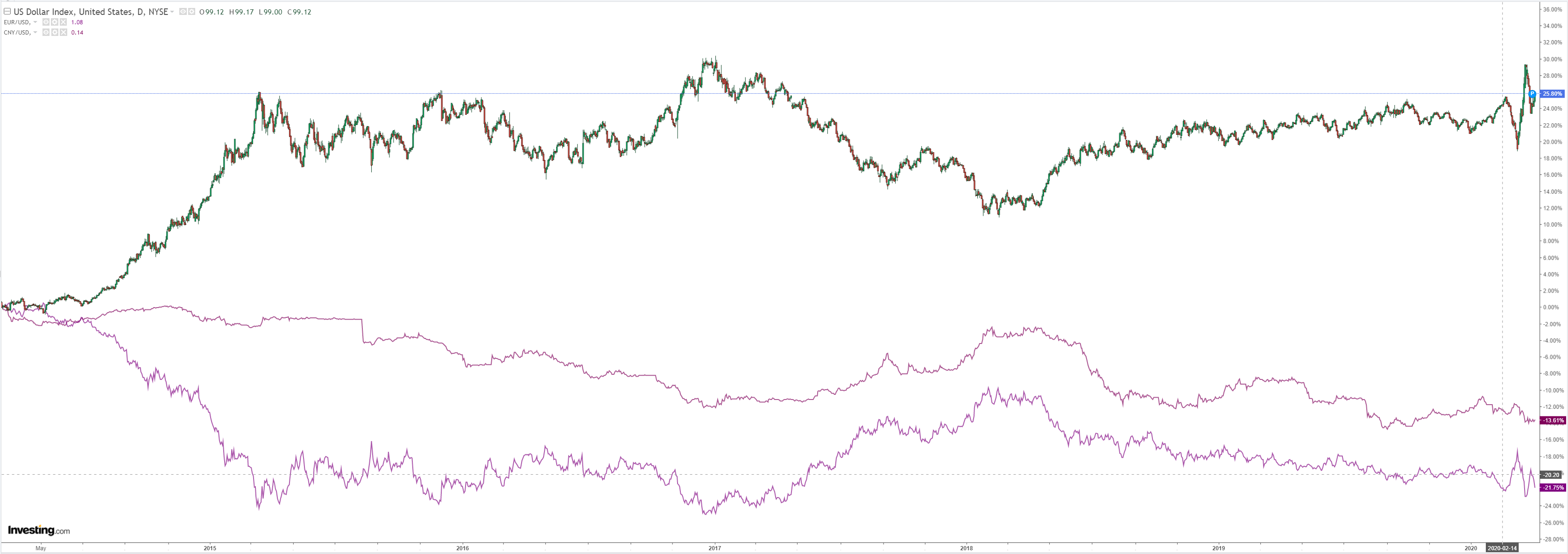

DXY was up again as EUR tumbles:

The Australian dollar hit new correction lows:

Gold jumped in another buy the dip episode:

Oil was amusing:

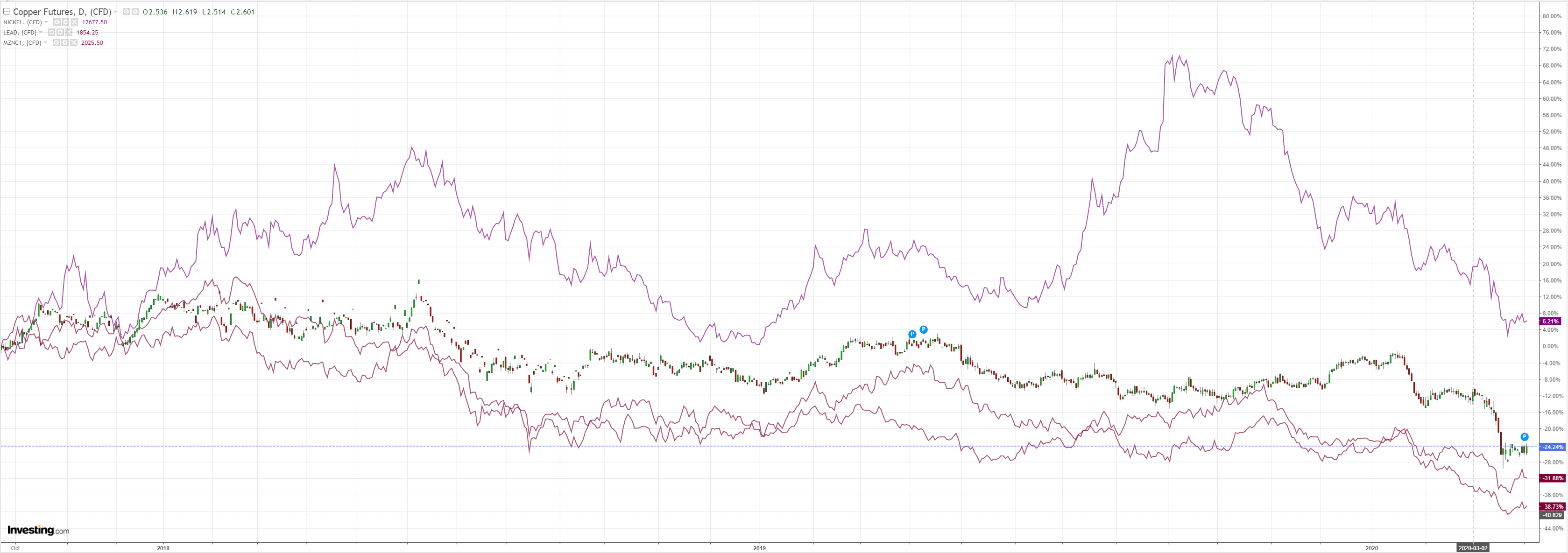

Dirt did nothing:

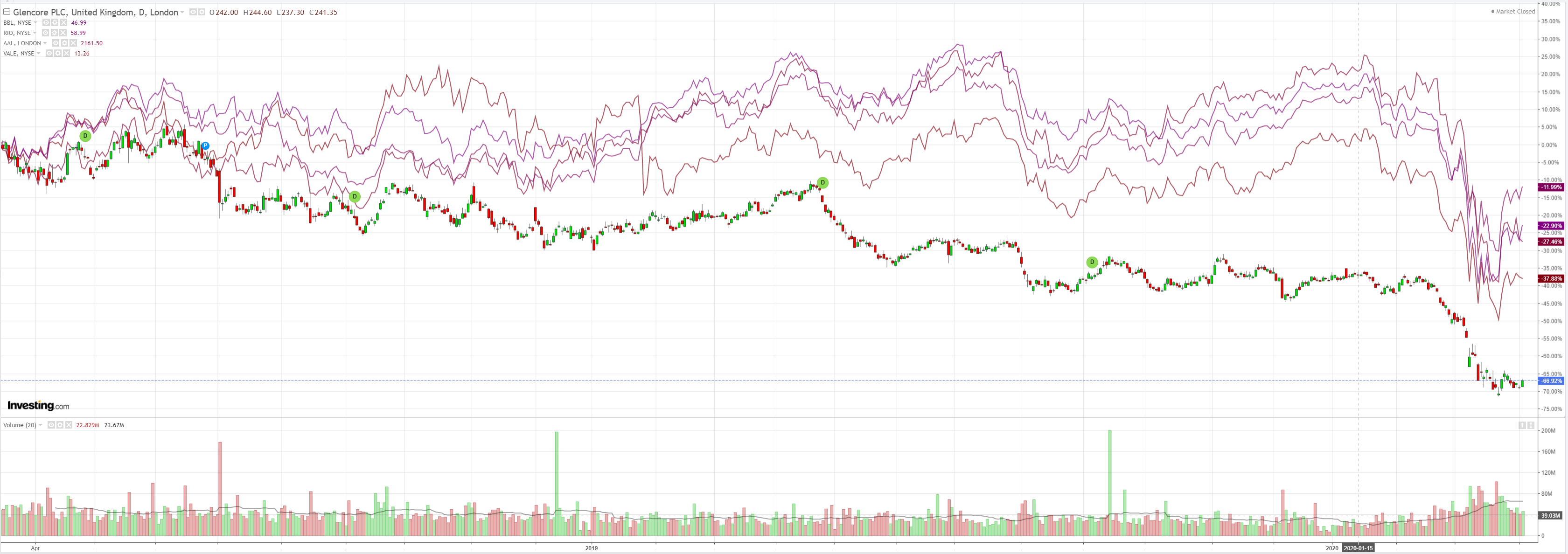

Miners firmed:

EM too:

Junk a little:

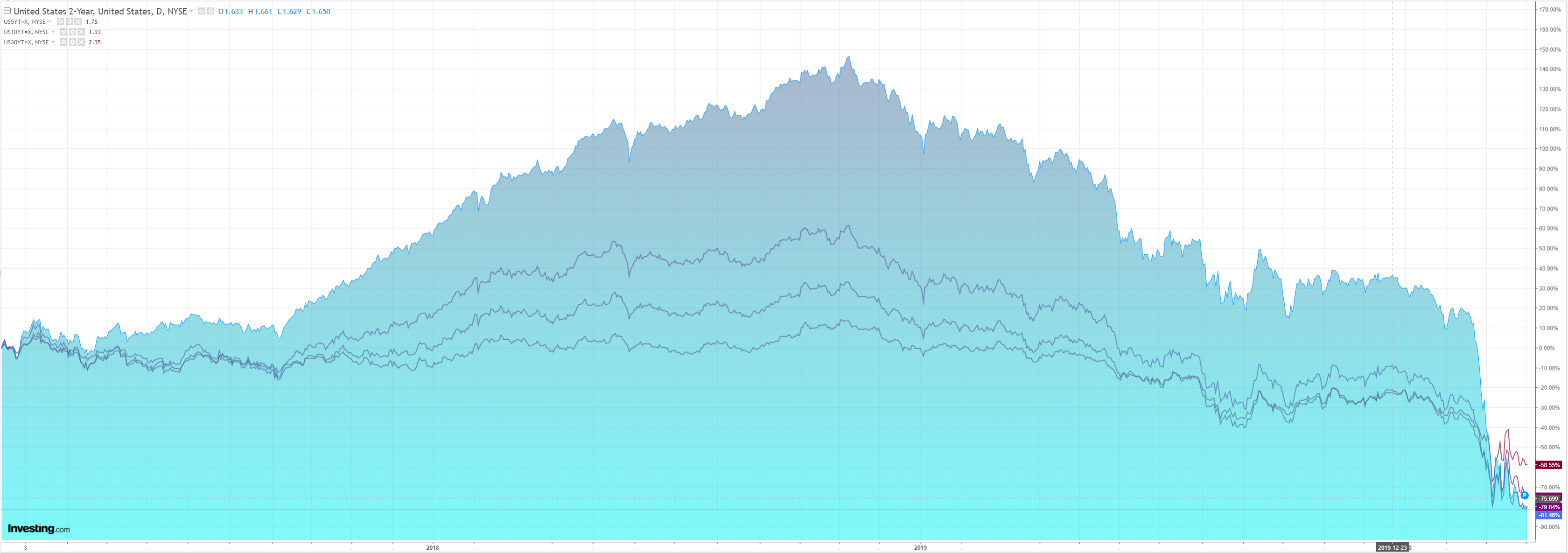

Bonds were mostly softer:

Stocks firmed:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 75,100 new confirmed cases on 1 April, vs 75,100 the previous day.

US Pres. Trump tweeted that he had held a constructive call with the Saudi Crown Prince and expected OPEC+ with Russia to agree to substantial oil production cuts of up to 15mn barrels per day. Also helping oil was an announcement from the US Department of Energy that it would prepare an immediate storage capability of 30mn barrels for Strategic Petroleum Reserves, with potential for a further 47mn barrels of storage. China is also reportedly poised to build substantial reserves.

US initial jobless claims for the week to 28th March rose 6,648mn after the prior week’s 3.307k (revised from 3.293k) – a 2-week total of almost 10m jobless claims. The outcome was within the wide band of analyst estimates.

Germany’s Economy Minister delivered updates to their economic projections for 2020. They now look for an annual contraction of -5% after a contraction in excess of -8% in 1H 2020. He also called for a substantial stimulus in order to support the economic recovery.

Moody’s affirmed NZ’s Aaa rating with a stable outlook, citing strong governance, sound monetary and fiscal positions and institutions, as well as a wealthy and flexible economy, and is resilient to credit shocks.

Event Outlook

Australia: The AiG Performance of Construction index stabilised at a soft base (printing at 42.7 in February). The March read should continue to reflect the contraction in construction, led by the housing sector. The final update for February retail trade is also due, following the preliminary read of 0.4%. Westpac expects a softer print of 0.2% in the final measure, under the assumption that the prelim survey was heavily skewed towards larger businesses such as supermarkets.

China: The Caixin services PMI is due, and the market expects a material rebound to 39.0 from 26.5 in February. Looking ahead, the outlook should continue to improve as restrictions are lifted in April.

US: Westpac expects that March non-farm payrolls will fall by 150k (market -100k). This deterioration should see the unemployment rate jolt higher to 4.0%. The rise to come in April will be much larger. In coming months, this growing slack will pass through to wages. For now, though, March average hourly earnings will hold up at 0.2%.

It’s all geopolitical rumourtage. Why would Saudi or Russia cut oil at all, let alone by such preposterous amounts which constitute 50-70 of their output? Nobody can offset the scale of Wuhan flu oil demand destruction and the US is about to see its shale sector collapse anyway so why hurt yourself as it falls? Notwithstanding the fractured nature of US oil. Trump has no hand to play beyond bluff and bluster.

Back in the real world, oil storage is running out fast, via Bloomie:

The 45 million-barrel Saldanha Bay oil storage terminal, the largest in the southern hemisphere, has been a vital outlet for surplus crude in past slumps, such as the great recession of 2008 to 2009. This time around, as the combination of the coronavirus pandemic and Saudi Arabia’s price war with Russia creates a record-breaking oversupply, its role may be more limited.

The facility is close to full, said four people with knowledge of the site’s operations. Several other people said all of the capacity there had been leased to trading houses, but space remained in some of their tanks and they expected additional crude deliveries.

Oil is still going to zero which will make the oil patch the epi-centre the US corporate debt shakeout.

In turn, that will keep weighing on the Australian dollar.