DXY is strong again:

The Australian dollar was universally dumped:

Gold got hammered but they bought the dip:

As Brent got sucked into the WTI vortex:

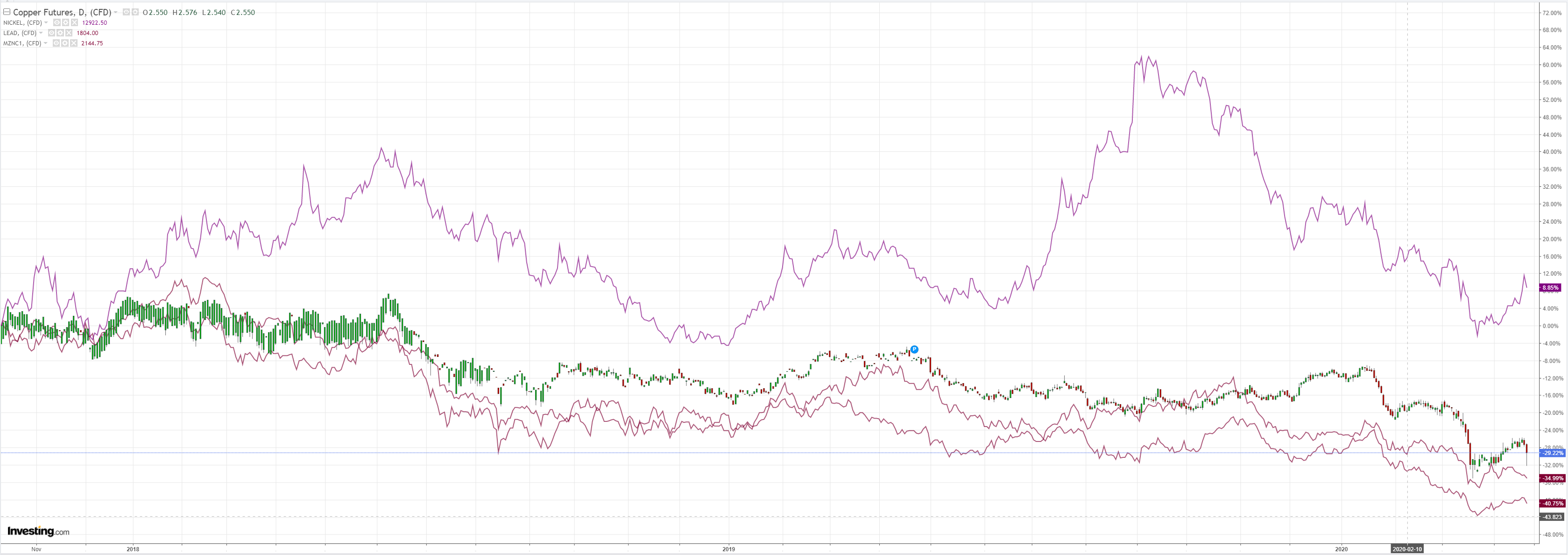

Dirt gave up:

Miners were crushed:

And EM stocks:

US junk gave way despite the Fed. EM did better for no obvious reason:

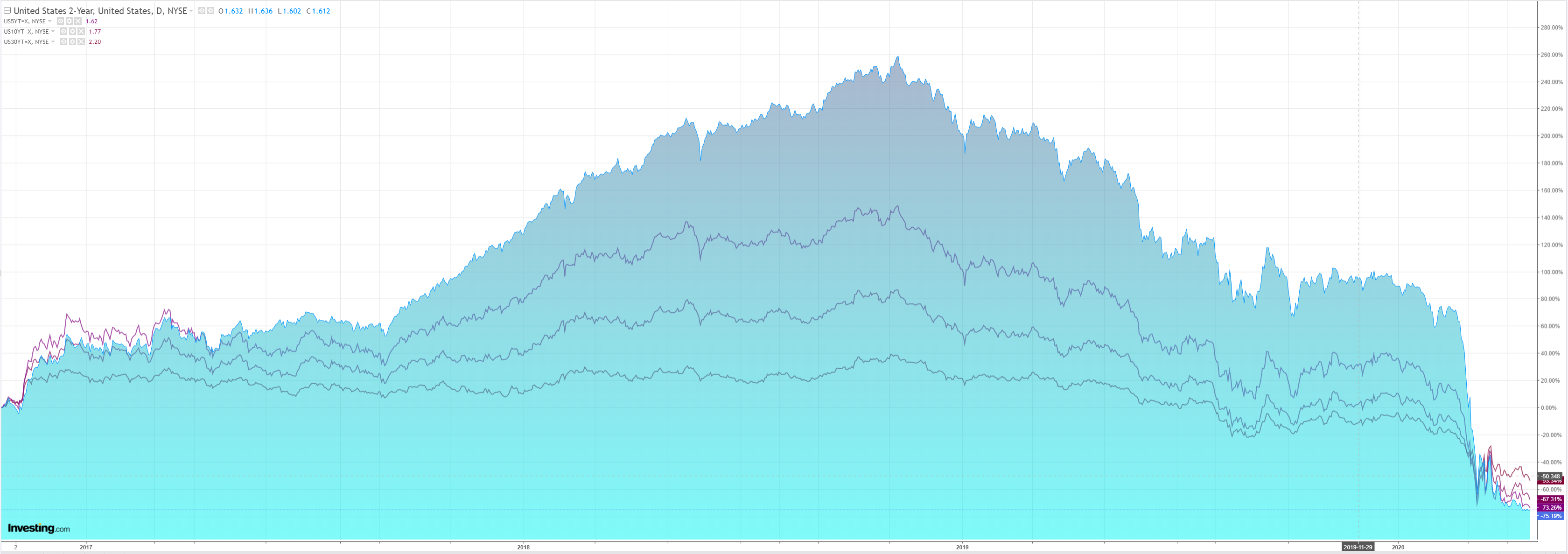

US yields are at all time lows:

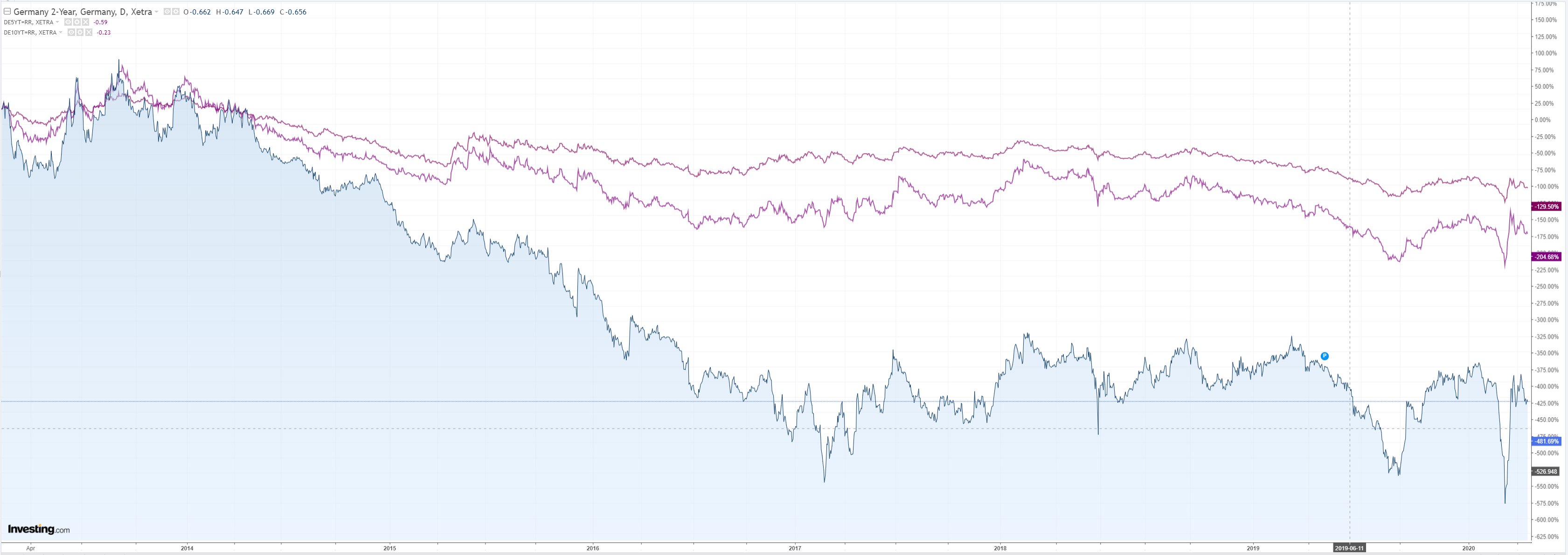

Germany and Australia were less bid:

Stocks fell sharply:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 71k new confirmed cases worldwide on 20 April, vs 84k the previous day and vs 99k at the peak on 12 April.

US officials agreed on a new $470bn pandemic relief plan, including assistance to small businesses and virus testing programs and hospitals. President Trump said he’d sign the measure and would begin discussions on further stimulus.

US March existing home sales fell 9%, as expected, to 5.3m from 5.8m.

The ZEW April survey for Germany recorded a sharp decline in current conditions to -91.5 (est, -77.5, prior -43.1). The GFC low was -92.8, and the 1993 low was 98.5. Expectations, however, rose sharply from -49.5 to 28.2 (est. -42.0), as did Eurozone expectations, jumping to +25.2 (from -49.5 in March). The details, though, showed that a sluggish return to growth was expected in 3Q and that pre-COVID activity levels were not expected to be regained until 2022.

In the UK, news of a 1.5m rise in welfare (Universal Credit) claimants by the end of last week underscored a likely sharp rise in unemployment in coming labour reports.

Event Outlook

Australia: The Westpac MI Leading Index is poised for a sharp fall this month. The March update will incorporate several extremely weak component updates, including: a plunge in the ASX200, weak consumer confidence, and higher unemployment expectations. Some support will come from robust commodity prices and dwelling approvals, and the wider yield spread.

Euro Area: The market expects that April consumer confidence will contract to -20, compounding a sizeable fall in the previous read.

UK: March CPI is expected to moderate to 1.5%yr as the demand shock and low oil prices apply downward pressure to price inflation.

US: February FHFA house prices are due and are expected to hold at 0.3%. However, this predates the spread of the virus. The price trend is set to deteriorate in coming months.

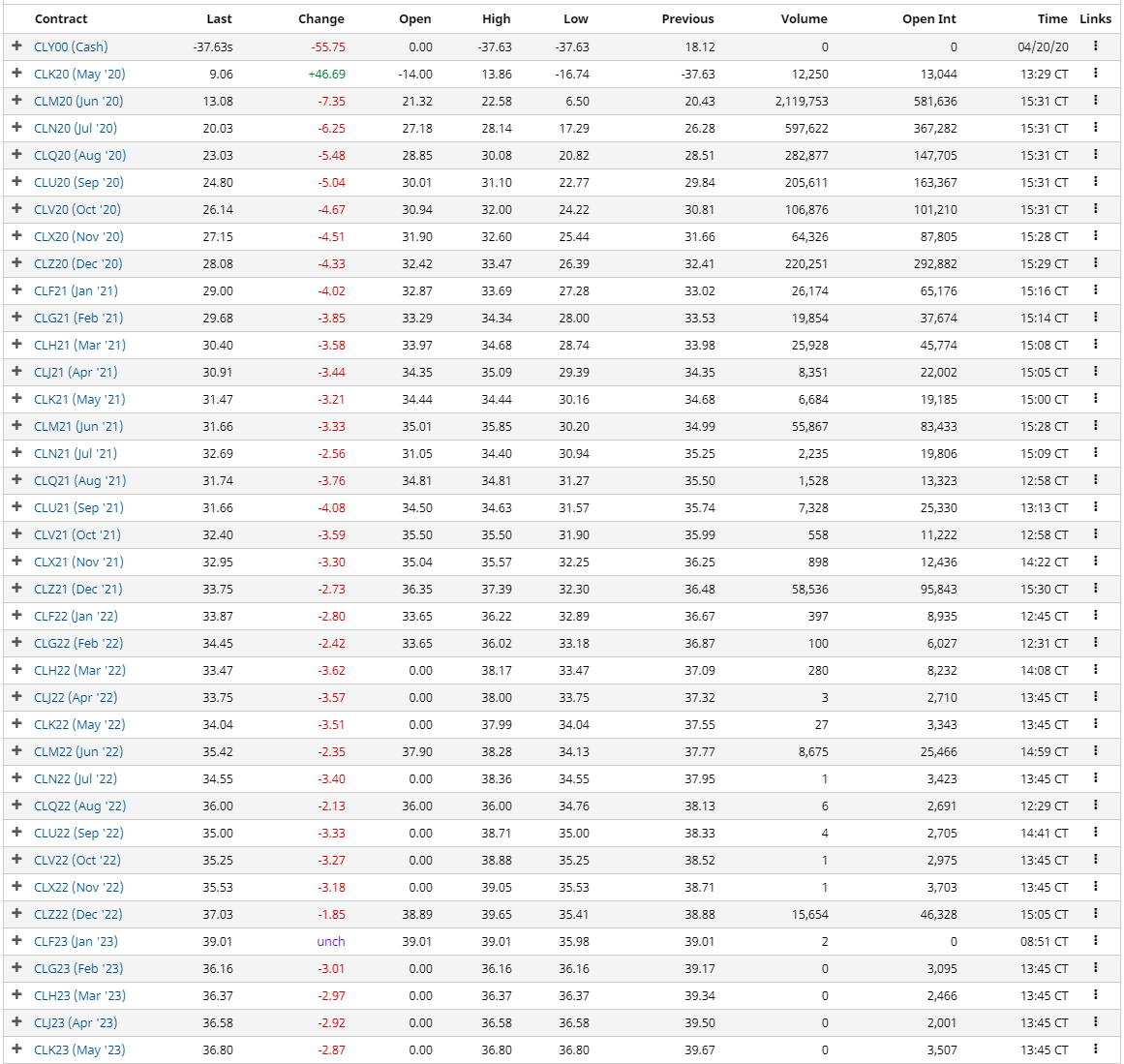

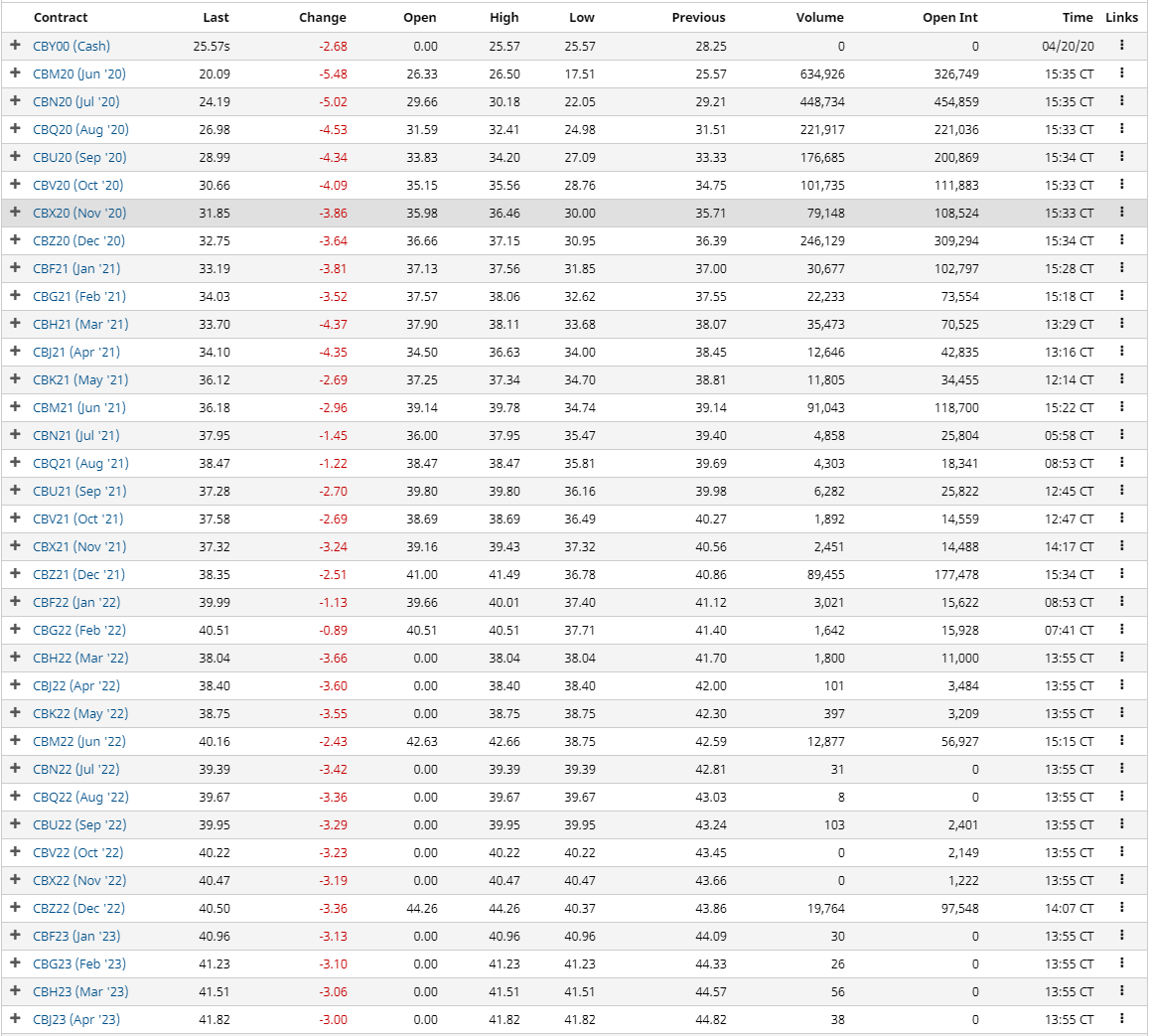

Oil is all that matters. WTI futures burned again:

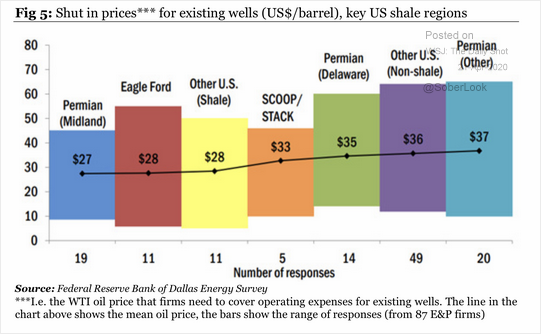

Nobody needs US shale for years, a huge hole in any recovery story:

More importantly for Australia, Brent was slaughtered:

Brent may not turn negative but I can still see it sinking below $10 no problems at all.

If it gets there, Australia will be selling LNG to Asia for $1Gj and under, the current account surplus will evaporate as the trade account is hit for a cool $30bn and the AUD crash much further.