DXY reversed upwards last night:

The Australian dollar reversed downwards:

Gold retraced:

Oil is at new lows:

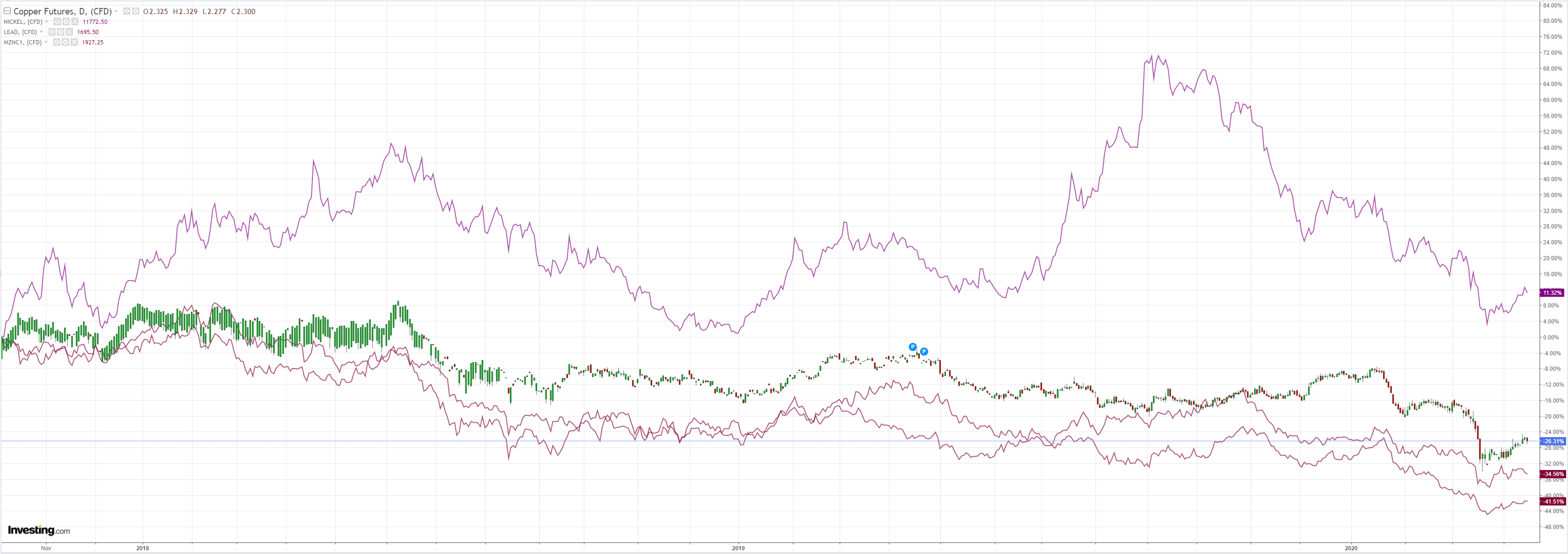

Dirt faded:

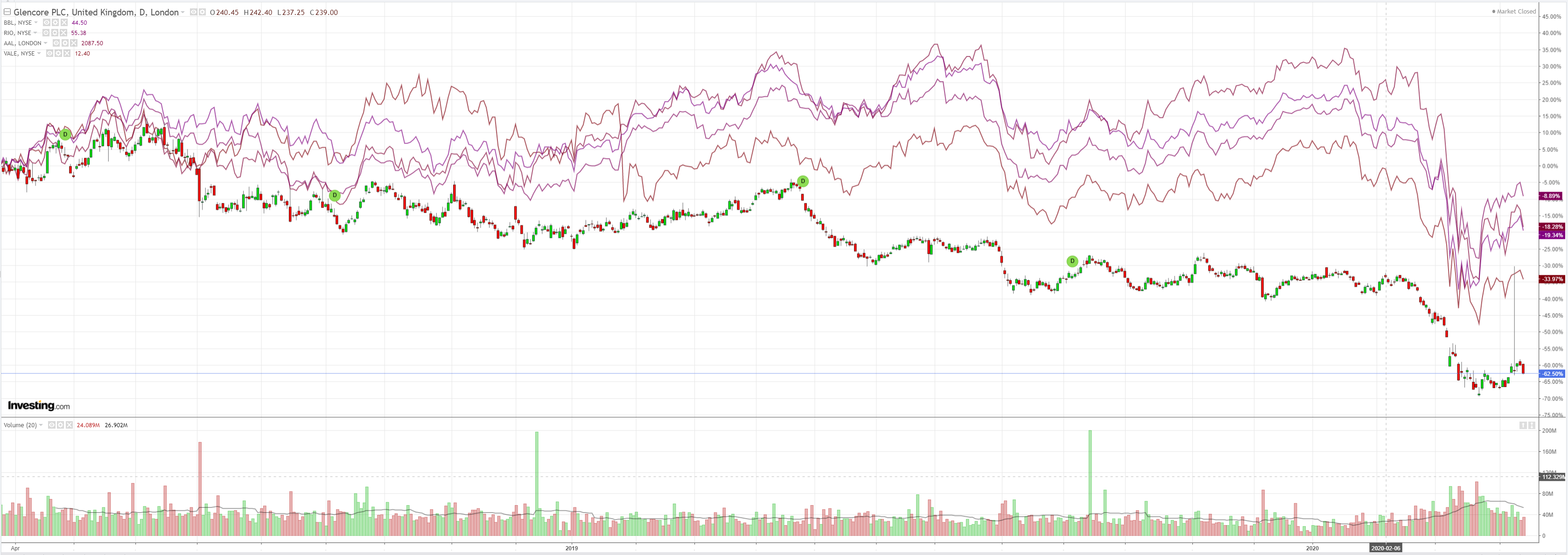

Miners were hit:

EM stocks gapped:

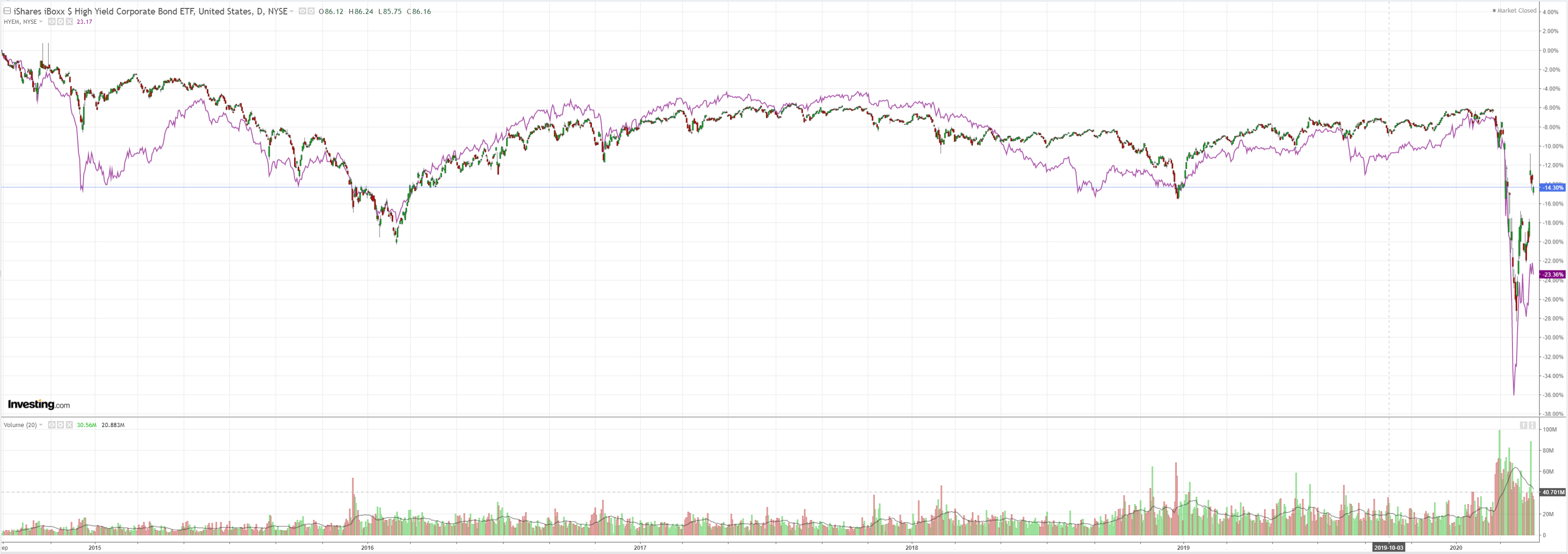

Even junk fell!

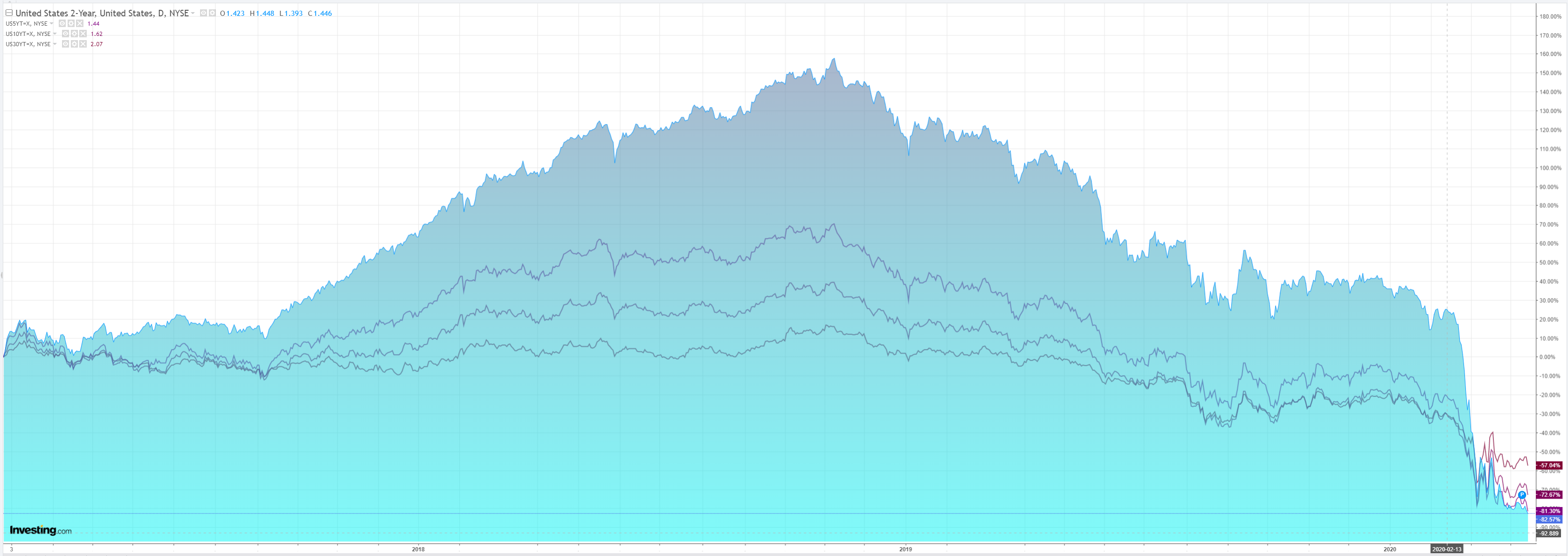

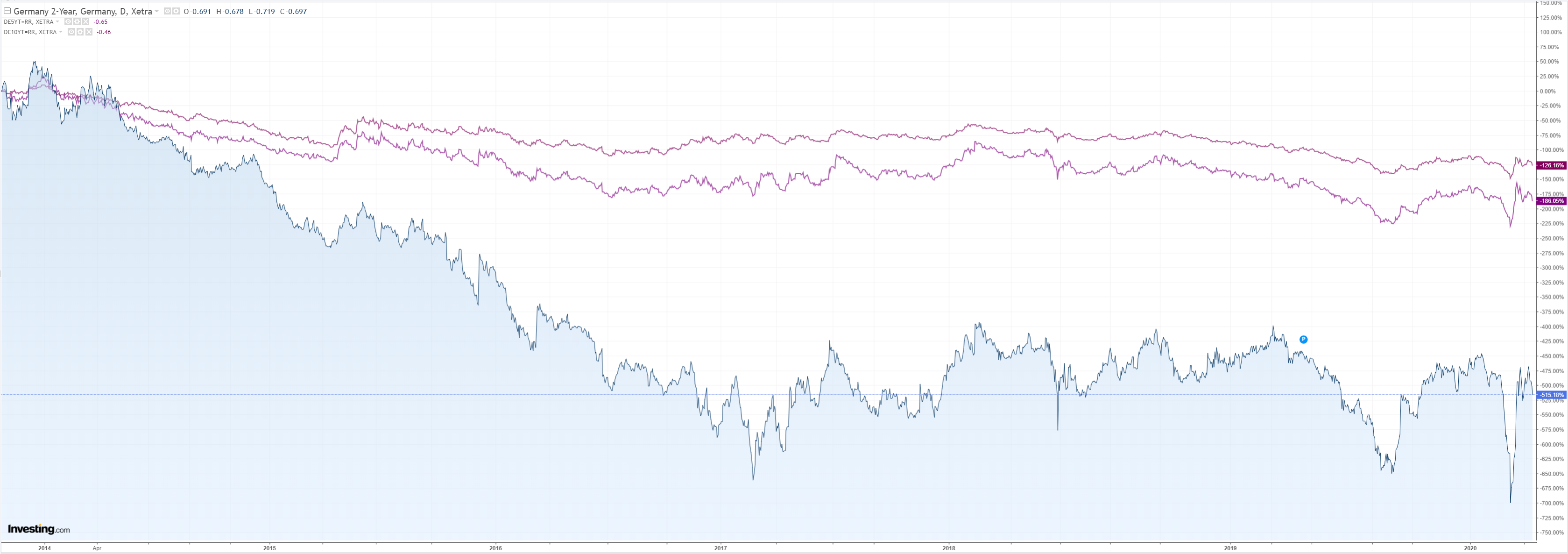

As bonds boomed anew:

Stocks flamed out:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 59k new confirmed cases worldwide on 14 April, vs 70k the previous day.

Some countries in Europe announced lockdown loosening. Germany may allow smaller shops to open next week, and schools to open in early May in a phased manner. Denmark will allow a phased schools reopening, starting with kindergartens. Italy is hoping to reduce restrictions from 4 May. The EC released (early) a road map for exit strategies being coordinated across the European region.

US March retail sales fell 8.7% – the worst monthly move on record (and vs -8.0% estimated), the ex-auto measure falling 4.5% (est. -5.0%). The scale of certain sector declines raised eyebrows: clothing -50.5%, furniture -26.8%, sporting goods -23.3% and restaurants -26.5%.

The Empire (NY) Fed April manufacturing business survey fell a record 34.4 to -78.2 in March (est. -35), with sharp falls in employment to -55.3 (from -1.5) and the average work week to -61.6 (from -10.6). US March industrial production also fell sharply, by 5.4% (est. -5.0%). NAHB April homebuilder sentiment survey also fell by a record amount, to 30 (est. 55) from 72. Despite the fall, the survey still reported a need to build homes, suggesting it would be a key sector in a recovery programme.

Bank of Canada left rates unchanged at 0.25% (as expected) but added further liquidity measures (including extending term repo maturities up to 24 months), and increased their bond-buying program (currently CAD5bn of government bonds per week). Total purchases will include up to CAD50bn of provincial debt, and up to CAD10bn of corporate bonds (investment grade) The BoC said that the measures could be altered, if needed, in both scope and scale.

Event Outlook

Australia: The major release of the day will be the March ABS labour force survey. The survey was conducted in the first two weeks of the month (prior to the introduction of lockdowns and other restrictions), so the brunt of the virus’s impact may not be felt until April. Westpac expects an employment change of -20k (market -30k). That should lift the unemployment rate to 5.3% (market 5.4%). April MI inflation expectations will also be released today. Falling petrol prices are likely to drive expectations lower.

NZ: PM Ardern is expected to reveal what the various lockdown levels (1 to 4) will look like, ahead of an announcement on 20 April about the current lockdown state (at level 4).

Euro Area: February industrial production is due, and the market expects a contraction of 0.1%. This is down from a robust +2.3% in January. Production is set to deteriorate further as headwinds mount.

US: For the April Phily Fed survey index, the market expects a decline to -32.0 as the business outlook deteriorates. Housing starts (market f/c -18.7%) and building permits (market f/c -10.7%) are also expected to have been adversely affected in March. Finally, initial jobless claims are poised for another substantial rise (market 5500k).

A bunch of “worst ever” falls for US data did the trick. There are so many devastated charts that I don’t know where to look.

In terms of forex, the AUD is trading as a pure risk on/risk off play. Given I still see much worse economic damage ahead it’s safe to say that Aussie dollar volatility is here to stay.

And if stocks return to the lows so will the Australian dollar.