The wildly volatile Australian dollar is still…running wild:

Brent and WTI have massively diverged:

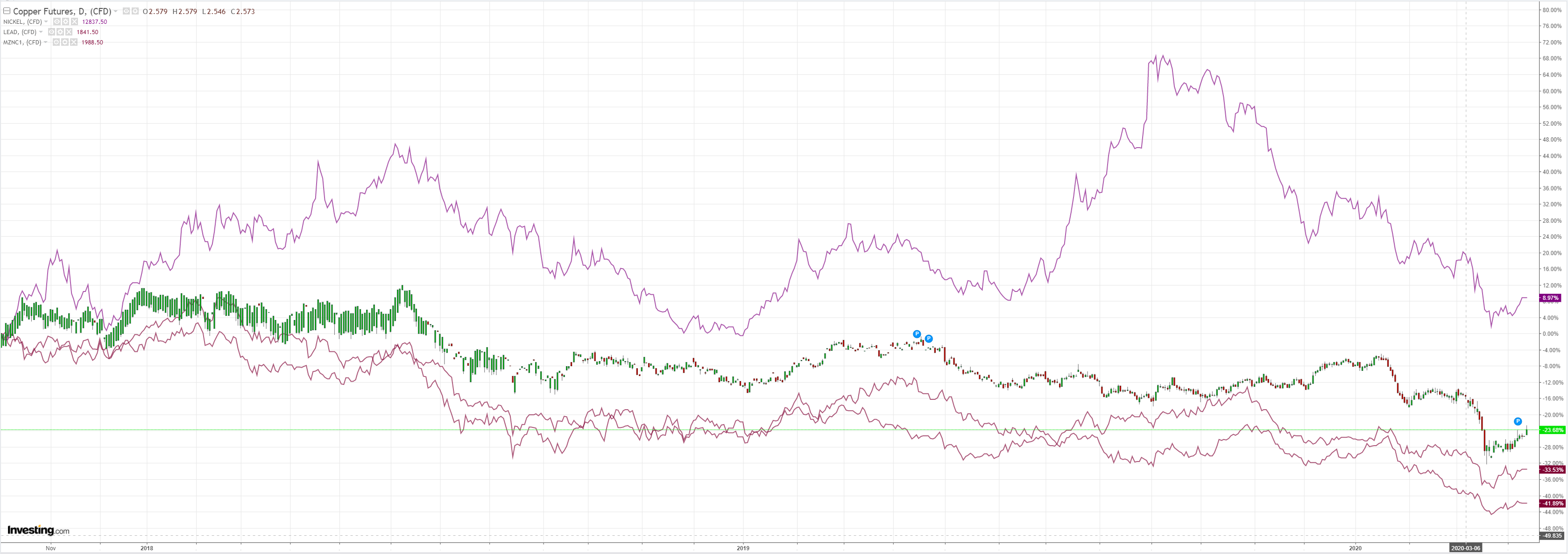

Dirt is mildly interested:

Advertisement

Gold has broken out:

Miners tacked on gains:

EM stocks didn’t:

Advertisement

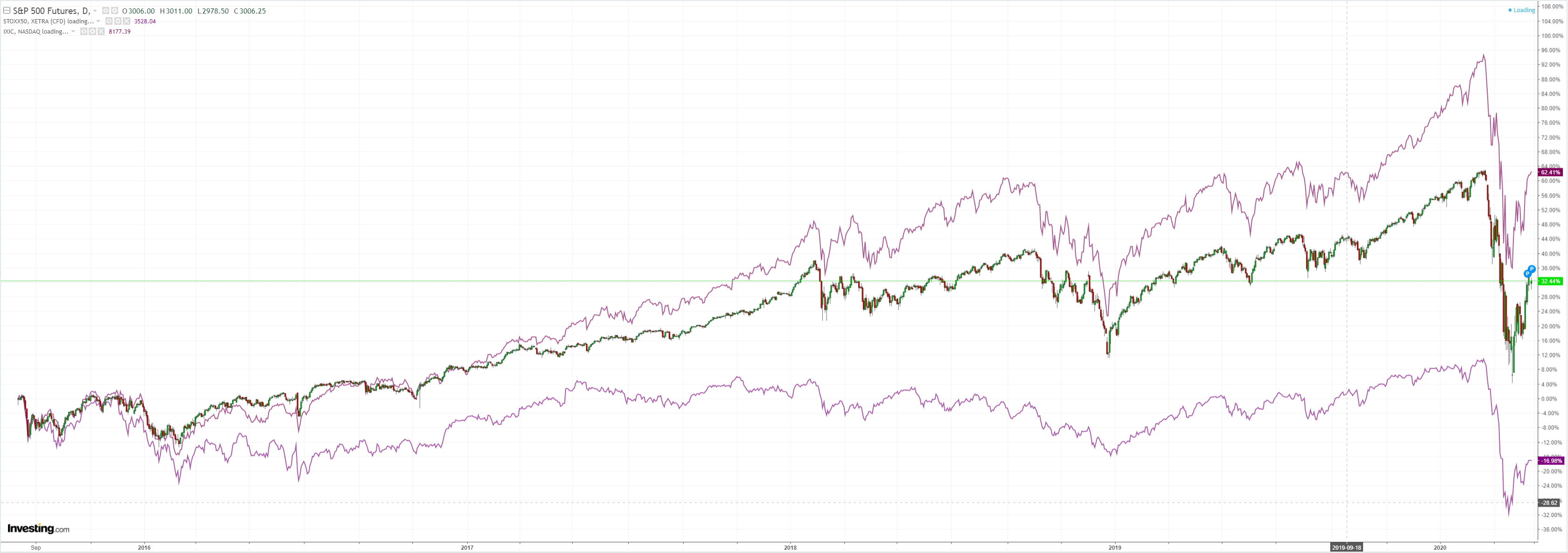

US gapped massively higher as EM sank:

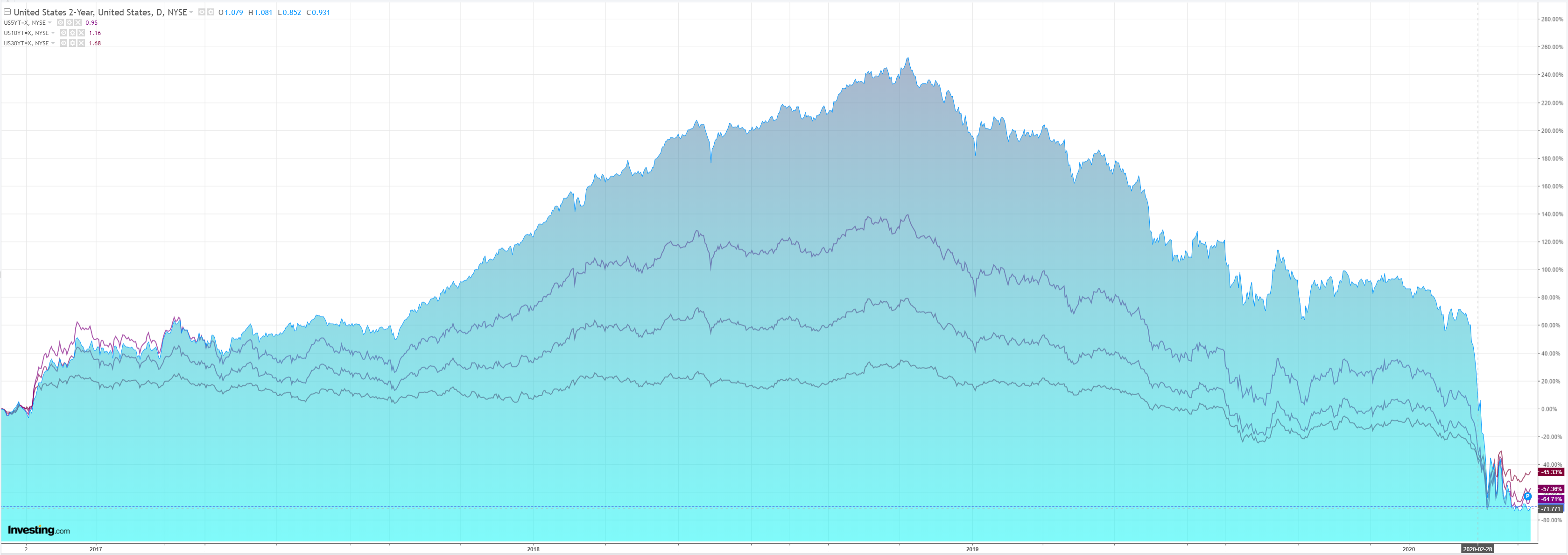

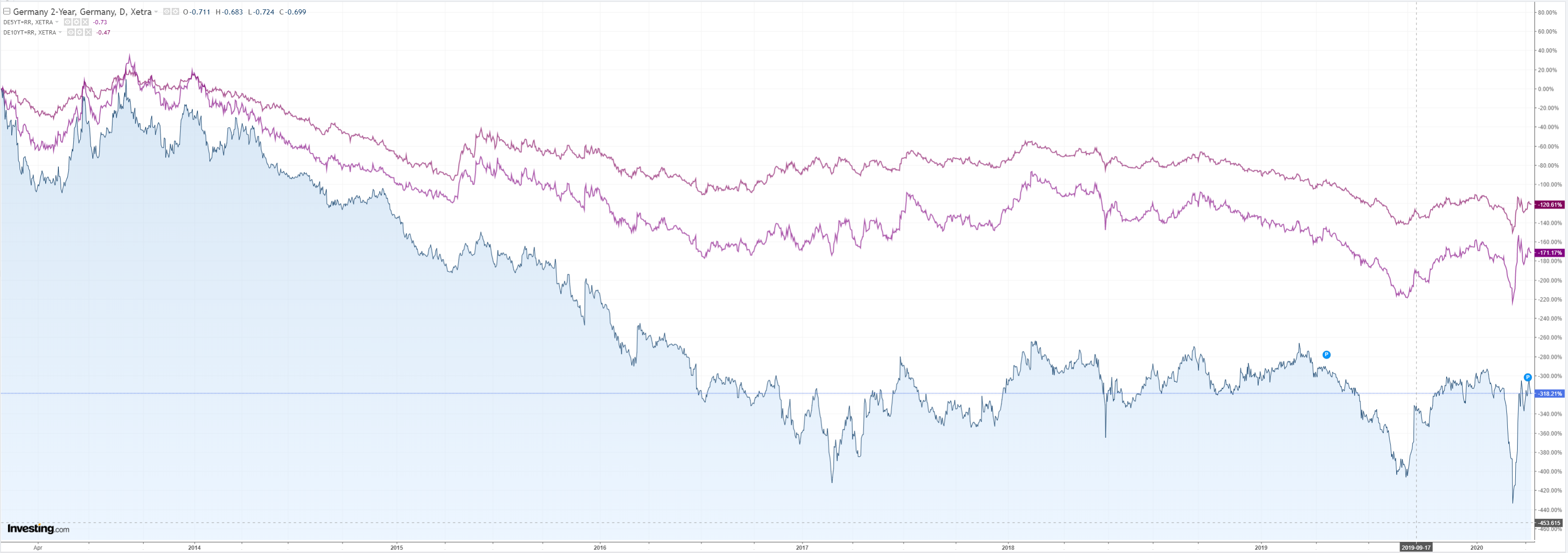

Bonds were mixed:

Stocks were mostly soft:

Advertisement

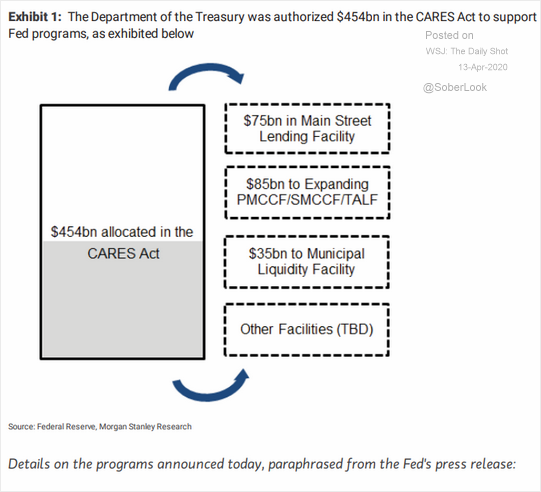

It was quite an Easter. From the top, the FOMC virtually nationalised US capital markets and is now funding:

Small and mid-size business loans (Main Street Lending Program, up to $600 billion).

Municipal debt (Municipal Liquidity Facility, up to $500 billion).

Corporate debt, including high-yield bonds that were recently downgraded from investment-grade (“fallen angels”).

The program will even include corporate bond ETFs that are “mostly” investment-grade, collateralized loan obligations (CLOs), and commercial mortgage-backed securities (CMBS).

The US Treasury is providing the first-loss (equity) tranche for the Fed’s financing facilities:

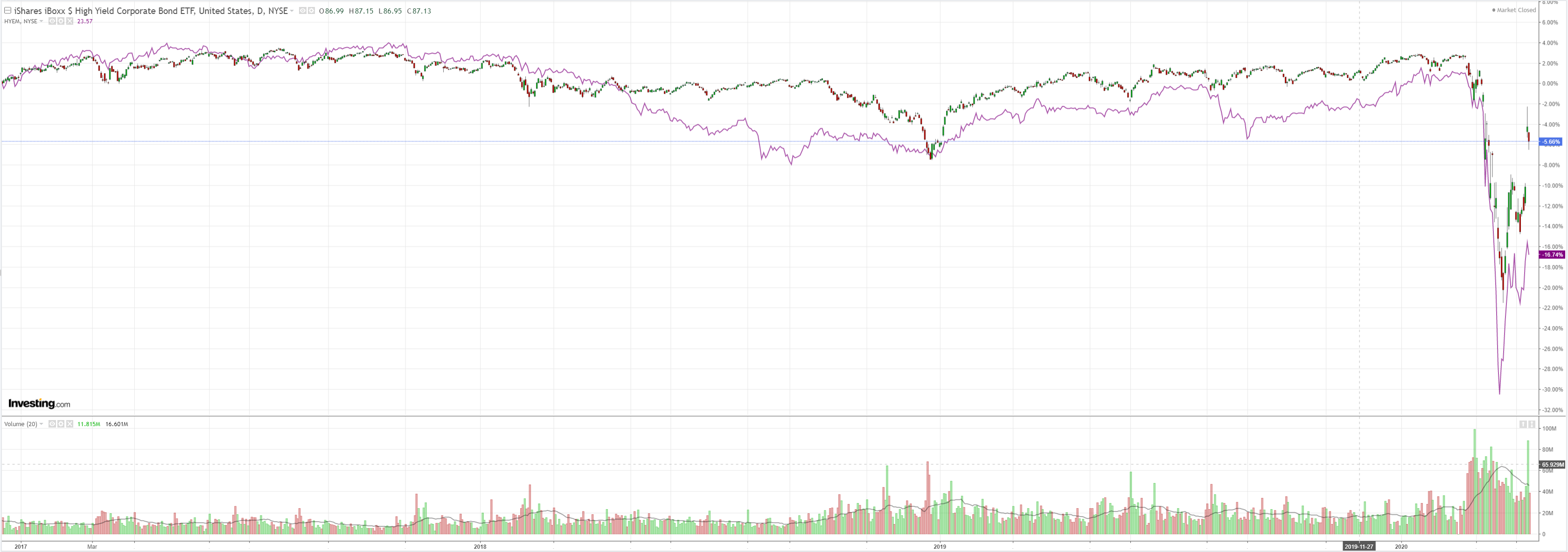

Even so, it cannot prevent massive cash flow hits from sending businesses under. What it has done is slow it all down as debt spreads can’t price the distress. Hence the huge jump in junk. SMEs remain a much larger problem because they are subject to banker credit risk, despite fiscal funding for loans.

The world’s biggest oil producers, including Russia, Saudi Arabia and the United States, have agreed to slash the world’s oil supply by 10 per cent in a desperate bid to lift prices, which have been hammered by the coronavirus outbreak.

Measures to slow the spread of COVID-19 have destroyed demand for fuel and driven down oil prices, straining budgets of oil producers and hammering the US shale industry, which is more vulnerable to low prices due to its higher costs.

The group, known as OPEC+, said it had agreed to reduce output by 9.7 million barrels per day (bpd) for May and June, after an emergency virtual meeting on Sunday.

All it has done is front-run the overflow of global capacity by a few weeks. I still see oil lower. Also Japanese in nature as deflationary pressures build.

Advertisement

In the Eurozone it’s all political extend and pretend, via the FT:

Eurogroup finance ministers have agreed an emergency rescue package aimed at responding to the coronavirus crisis but left unresolved questions on how to pay for a later economic recovery plan for the bloc.

The breakthrough on immediate economic measures supporting businesses, workers and sovereigns was achieved on Thursday night after the Dutch government backed away from prior demands that lending from the region’s bailout fund be made subject to tougher conditions.

Eurozone governments have been struggling to unlock a co-ordinated rescue package as they debate the degree of burden sharing needed to underpin economic activity across the bloc. While ministers agreed on a €500bn package of palliative economic measures in their meeting, they did nothing to lay to rest the festering dispute over how to pay for the longer-term economic reconstruction effort that will follow the crisis.

In other words, there was no breakthrough at all. Massively deflationary. Sushi anyone?

Advertisement

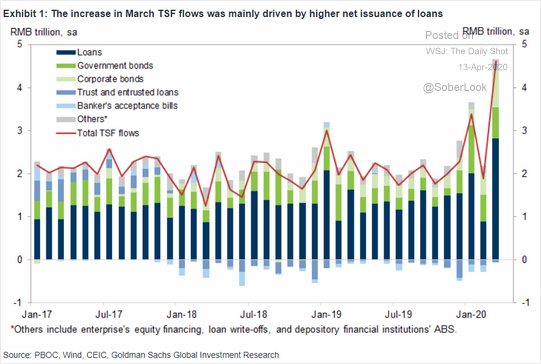

Finally, in China, we see the very thing it swore it would never do again, flood stimulus in the true Japanese tradition:

Policymakers have bulwarked everything now. It will not prevent a recession but will extend the pain via a weak recovery for many years. That’s the price we pay of our finely-tuned global debt machine that lends in the good times and collapses into public embrace in the bad.

Advertisement

The Australian dollar is still running wild with risk as markets substitute a catastrophe narrative with a Planet Japan narrative that can absorb the COVID-19 losses.

What it cannot do is prevent them. And the Australian dollar will roll when that becomes obvious.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.