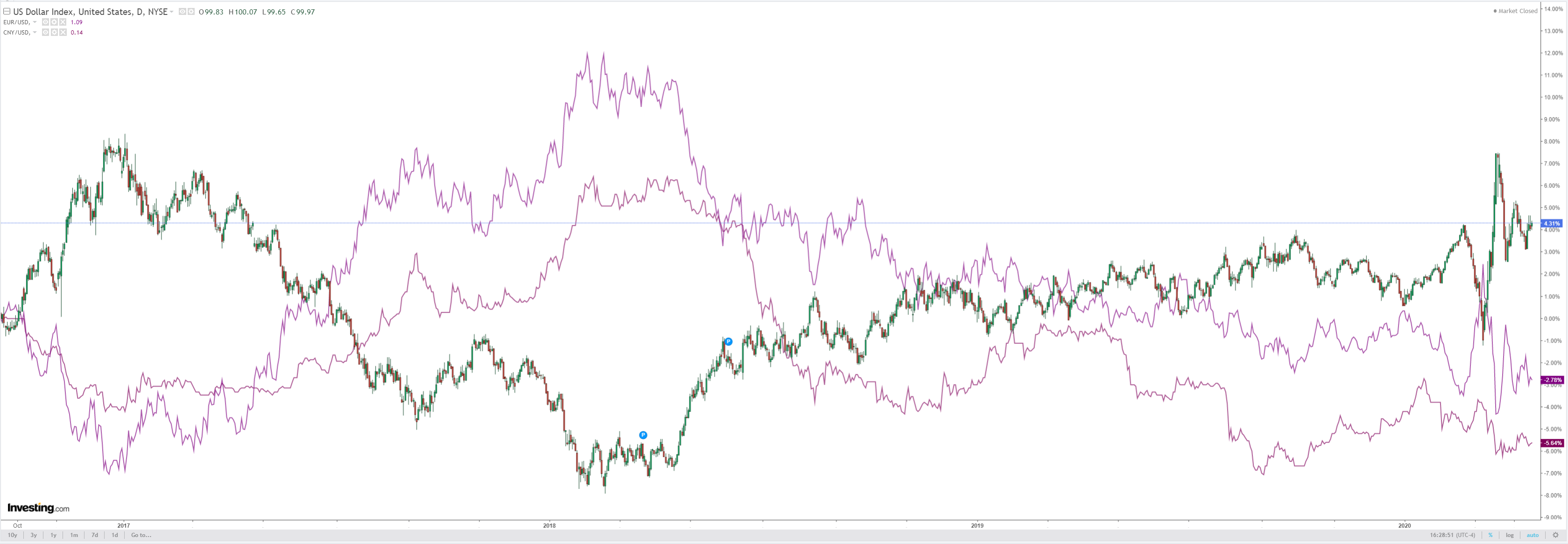

DXY firmed overnight as oil chaos engulfed markets:

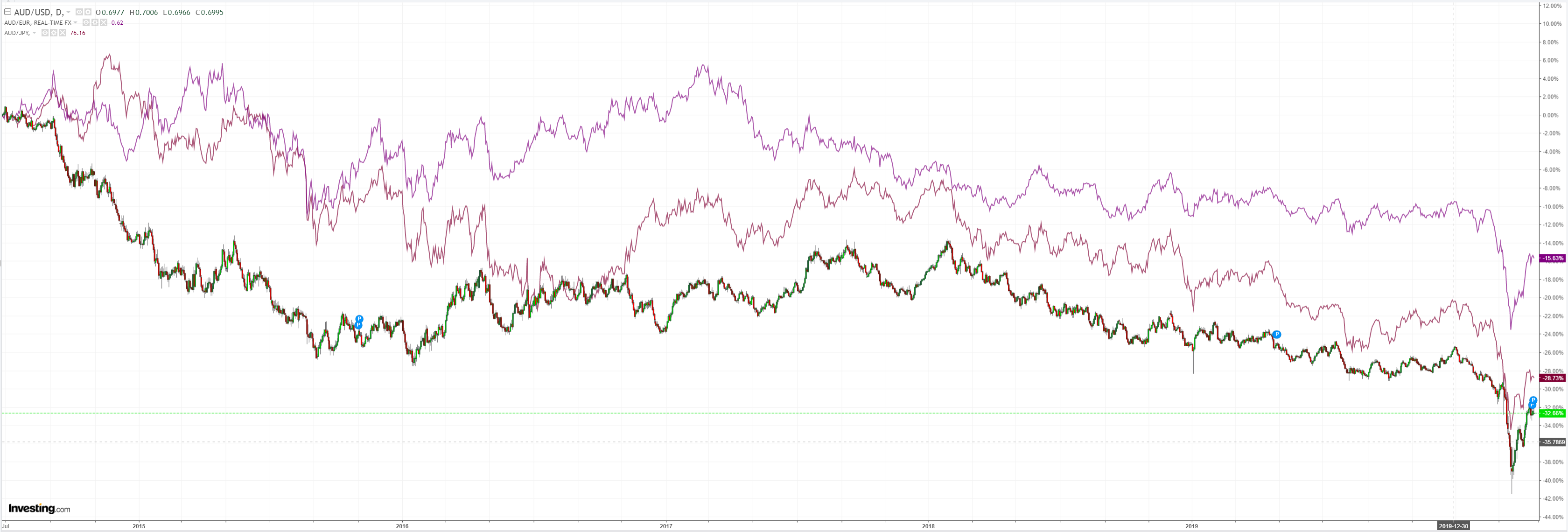

The Australian dollar rolled versus DMs:

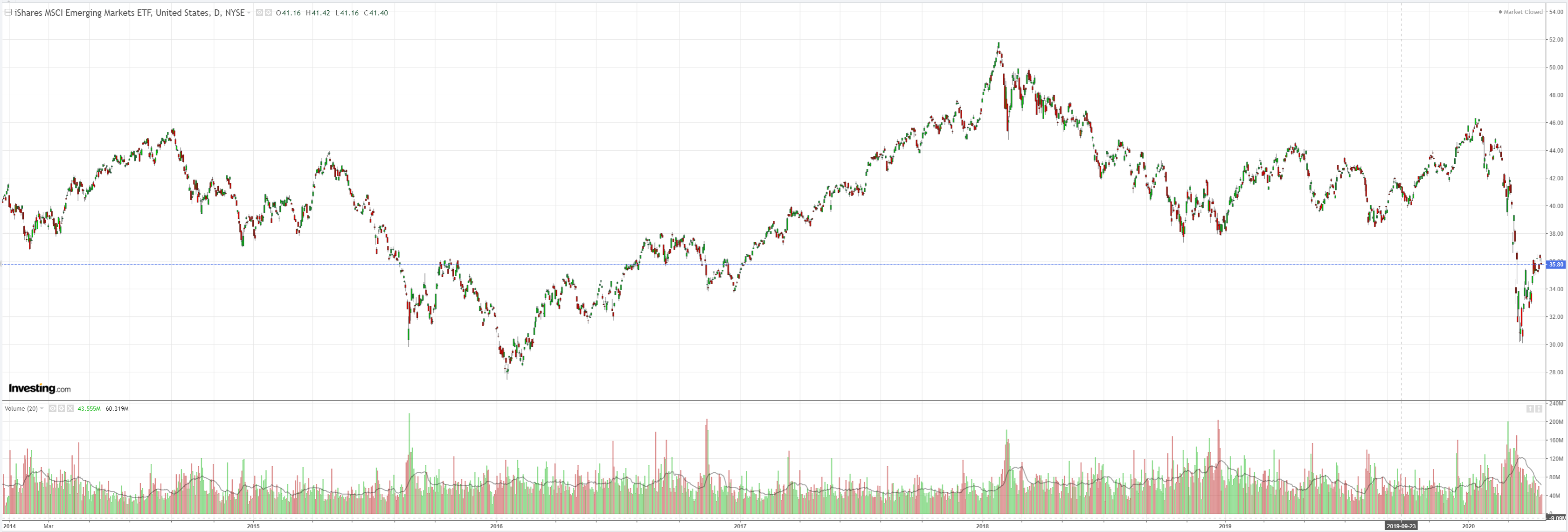

But EMs cratered:

Gold bounced off its breakout line:

Oil melted down:

Dirt mostly rolled as well:

And miners:

Plus EM stocks:

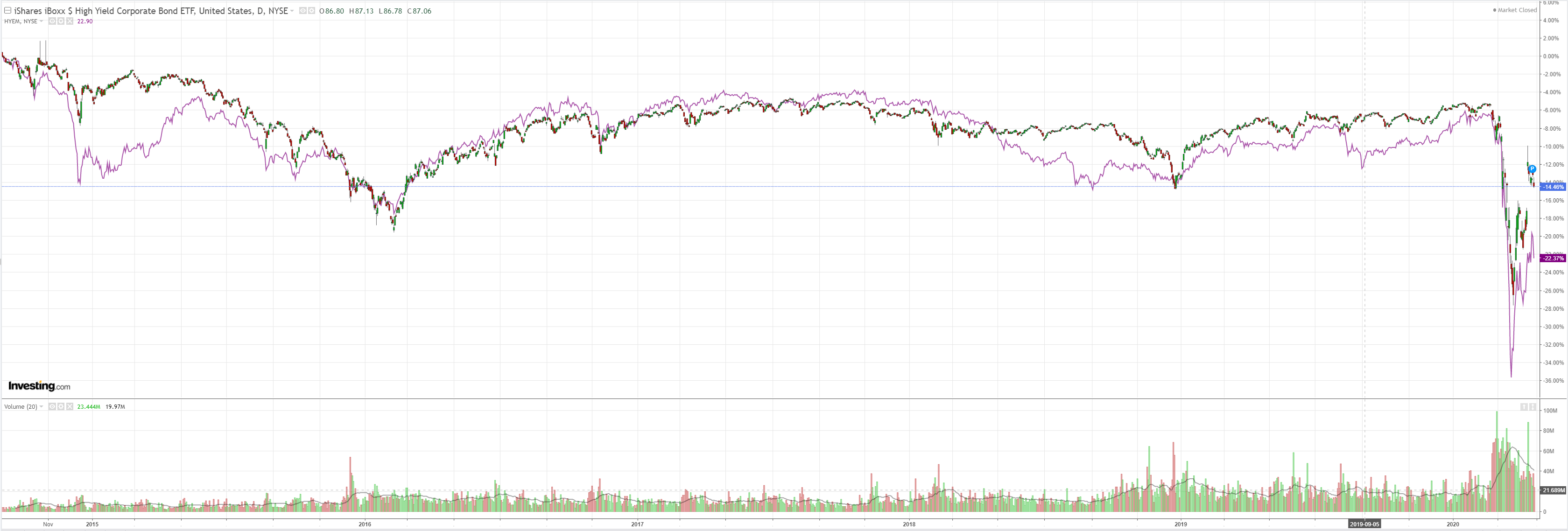

Importantly, junk fell. Without the Fed, this market would be leading us into GFC 2.0:

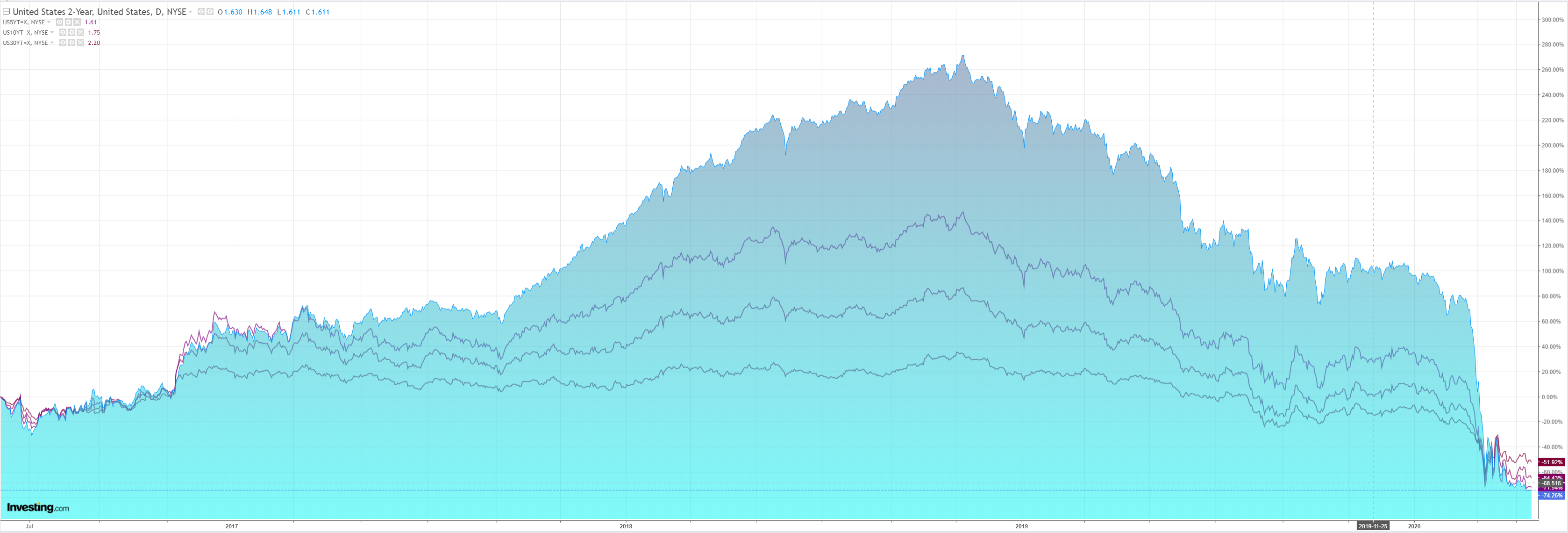

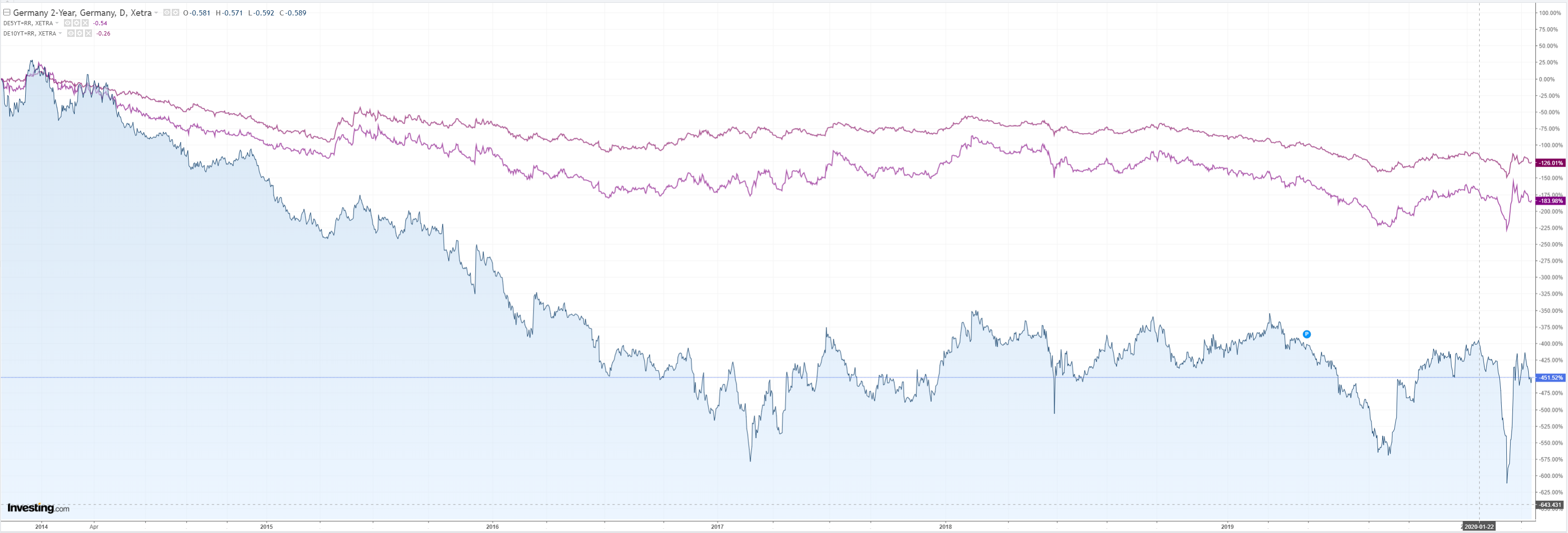

Bonds were mostly calm:

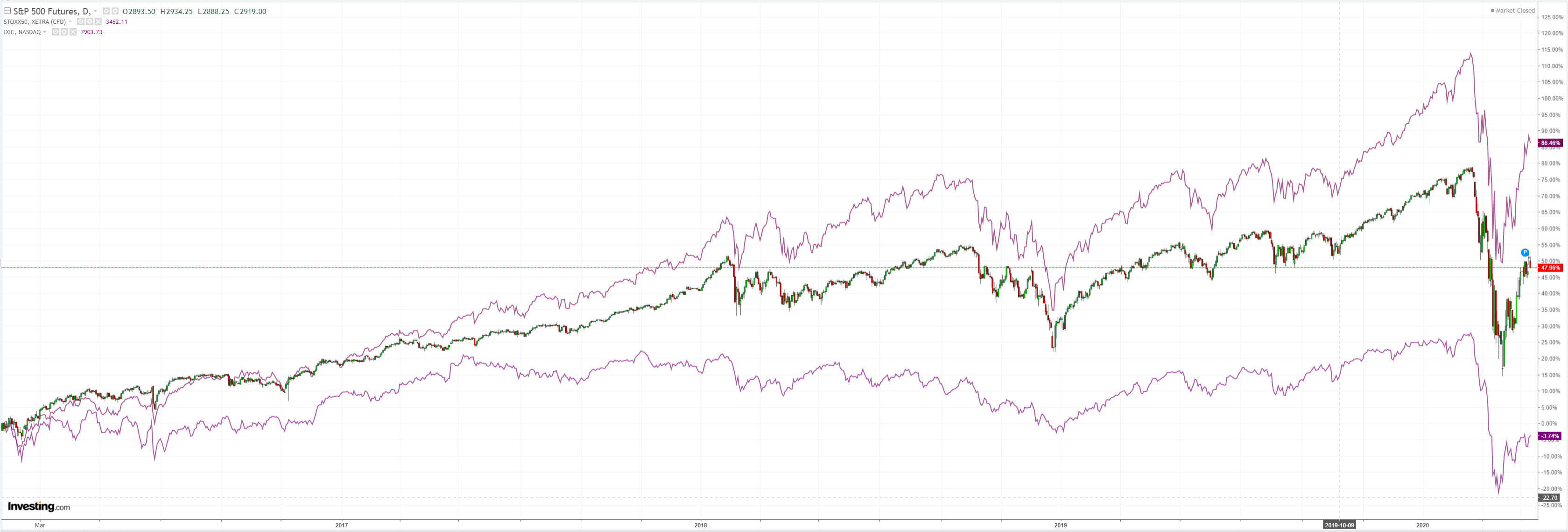

Stocks took a hit:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 84k new confirmed cases worldwide on 18 April, vs 78k the previous day and vs 99k at the peak on 12 April.

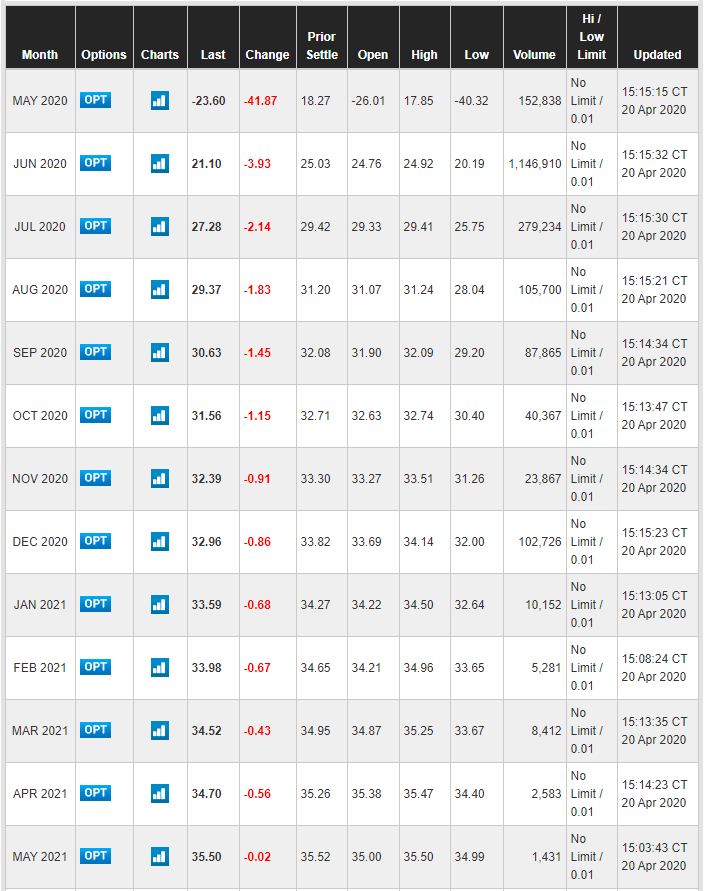

West Texas crude oil futures prices which are due to expire on Tuesday fell to a negative number — minus $40 a barrel, and the lowest on record. At that price, sellers would pay buyers for the oil. The situation has arisen due to extreme oversupply in the US, with some storage facilities unable to accept any more product. Potential owners of oil via the May contract are thus rolling their positions into June to avoid taking physical delivery.

US Chicago Fed March national activity survey fell -4.19 (within the wide range of estimates which were centred on -3.0) from prior +0.06 (revised from +0.16). The GFC low was -4.76.

Eurozone Feb trade surplus widened to EUR25.8bn, est. EUR20bn).

EC officials stated that a possible Bad Bank option to solve persistent NPL issues was not being discussed, despite ECB comments that such a possibility was being discussed.

BoE Dep Gov Broadbent and Chief Economist Haldane held an online presentation in which they agreed that the OBR’s scenario of a 35% contraction in GDP in Q2 was plausible and that scarring to the economy could mean a longer recovery path. They also said that their low rate policy was in line with inflation policy.

Event Outlook

Australia: The RBA will publish the minutes of its April meeting. The market will be looking for commentary around the Bank’s yield curve control, and guidance on the impact of the shutdown. Following this, Governor Lowe will deliver a speech titled “Economic and Financial Update” (3:00 pm).

New Zealand: The results of the GlobalDairyTrade auction are due; the futures market is pointing to little change in WMP prices.

Euro Area: The April ZEW survey of expectations will be released. This follows an abrupt deterioration to -49.5 in March.

UK: The February ILO unemployment rate is expected to remain unchanged at 3.9%. This release predates the brunt of the lockdowns, and the unemployment trend is set to turn in coming months.

US: March existing home sales are poised for a substantial contraction (market f/c -8.2%). Until conditions ease, disruptions from the virus will continue to suppress turnover.

The oil carnage is nicely captured in futures:

Do not adjust your TV. That is the May contract falling $42 to -$23.60. How is that even possible?

If we forget about the negative, it is actually normal. We now have what is called a “super contango”. That is, future prices are much higher than today so market players buy oil to store it and sell at a higher price in the future.

The negative number on near term futures is the cost of storage.

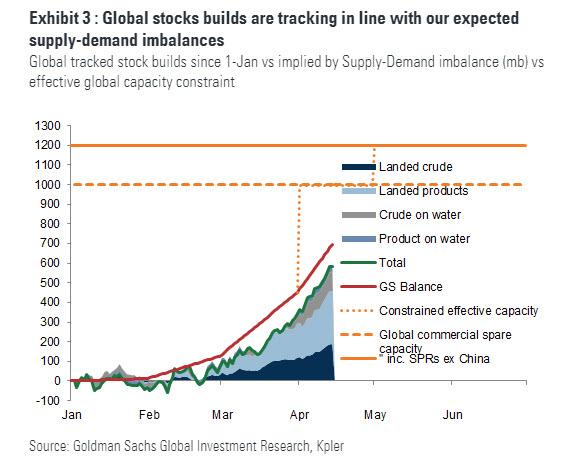

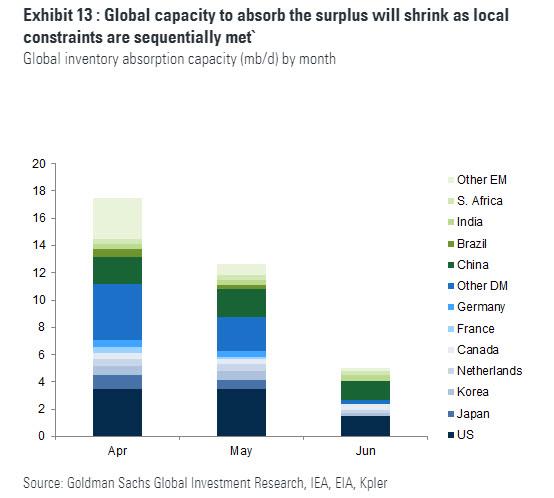

The US and WTI are leading it because its oil storage capacity will run out first. But it will come for Brent soon as well as global capacity also brims over:

Because Australian gas exports are priced off Brent the Aussie dollar is a little protected at this point.

If and when Brent buckles as well the AUD will find it much harder to hold as we will be paying Asian customers to take our gas (as we still pay full whack at home of course).