DXY fell last night:

The Australian dollar roared on against DMs:

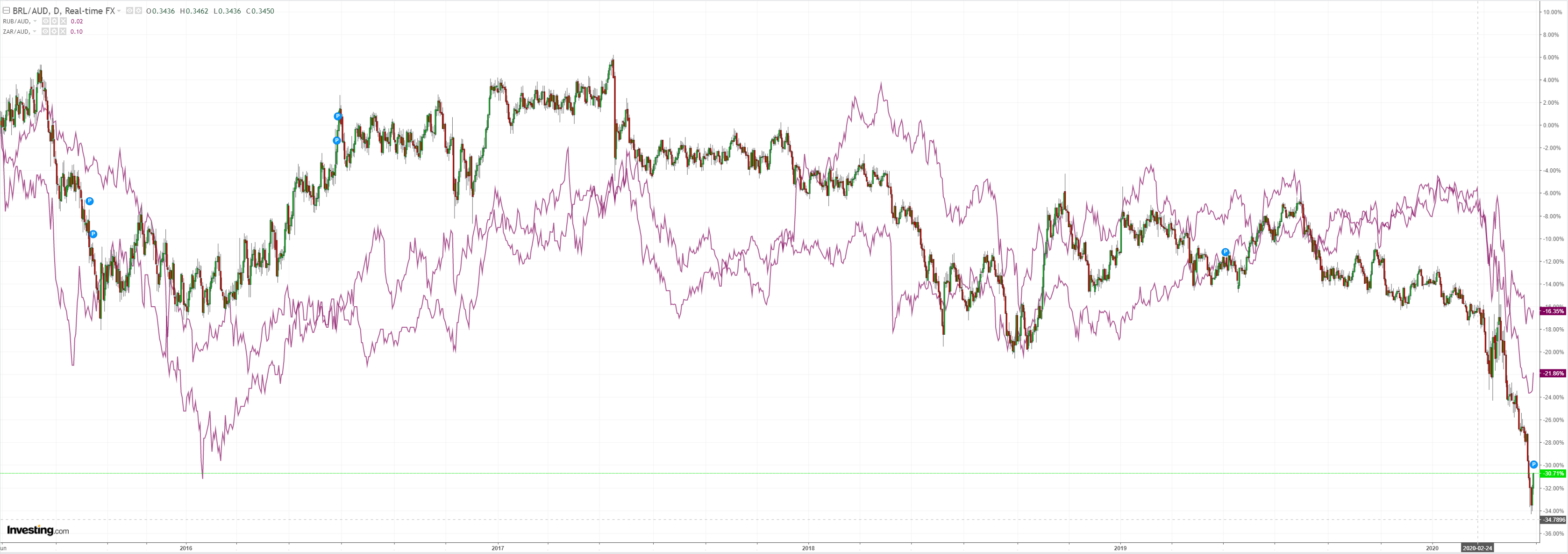

But EMs caught the bug more:

Gold was firm:

Brent oil jumped:

Dirt too:

Miners surged:

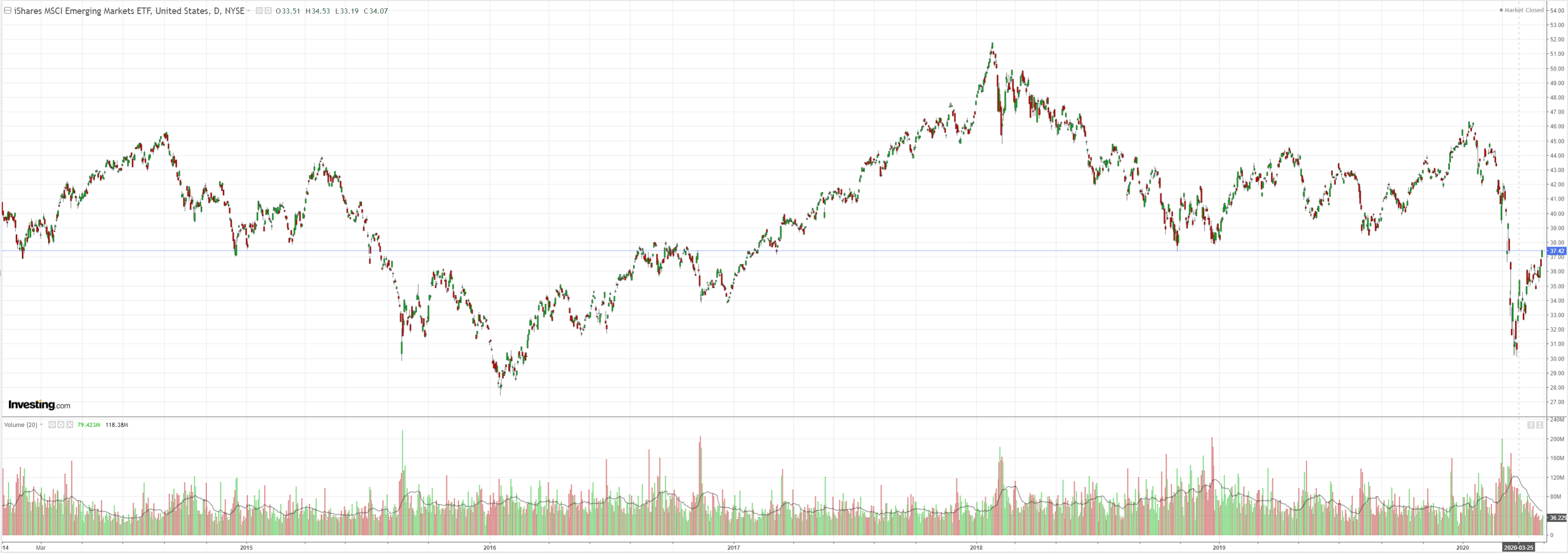

EM stocks surged:

Junk bounced:

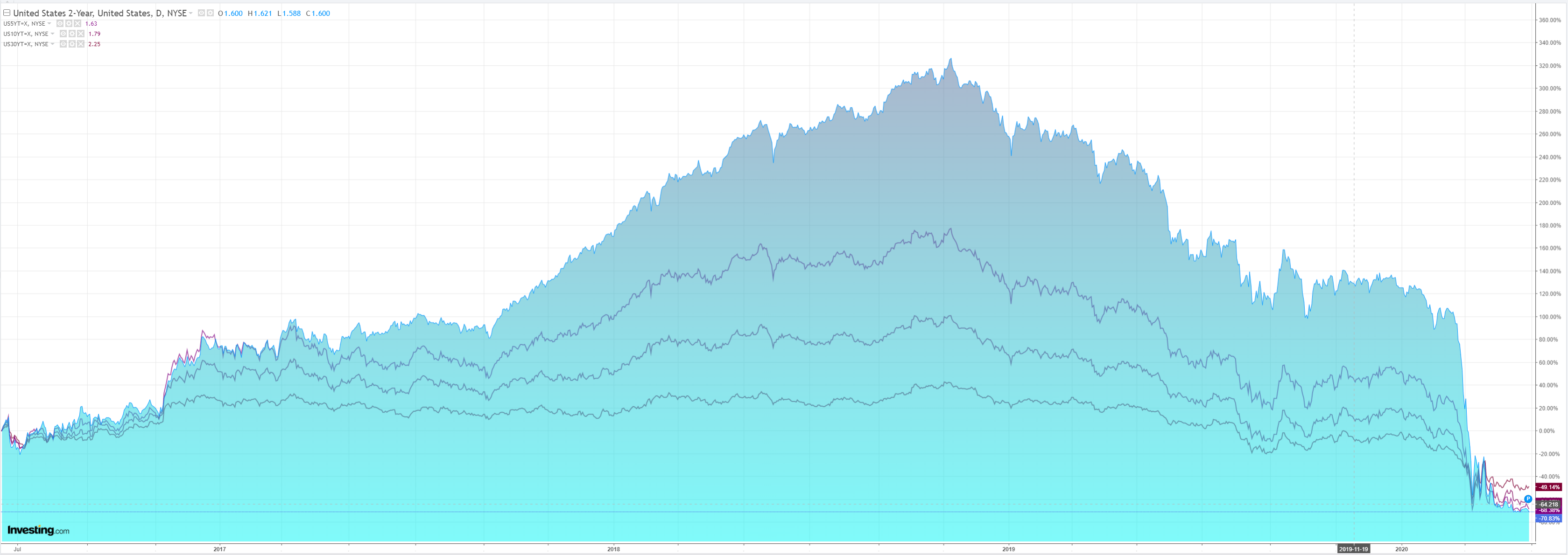

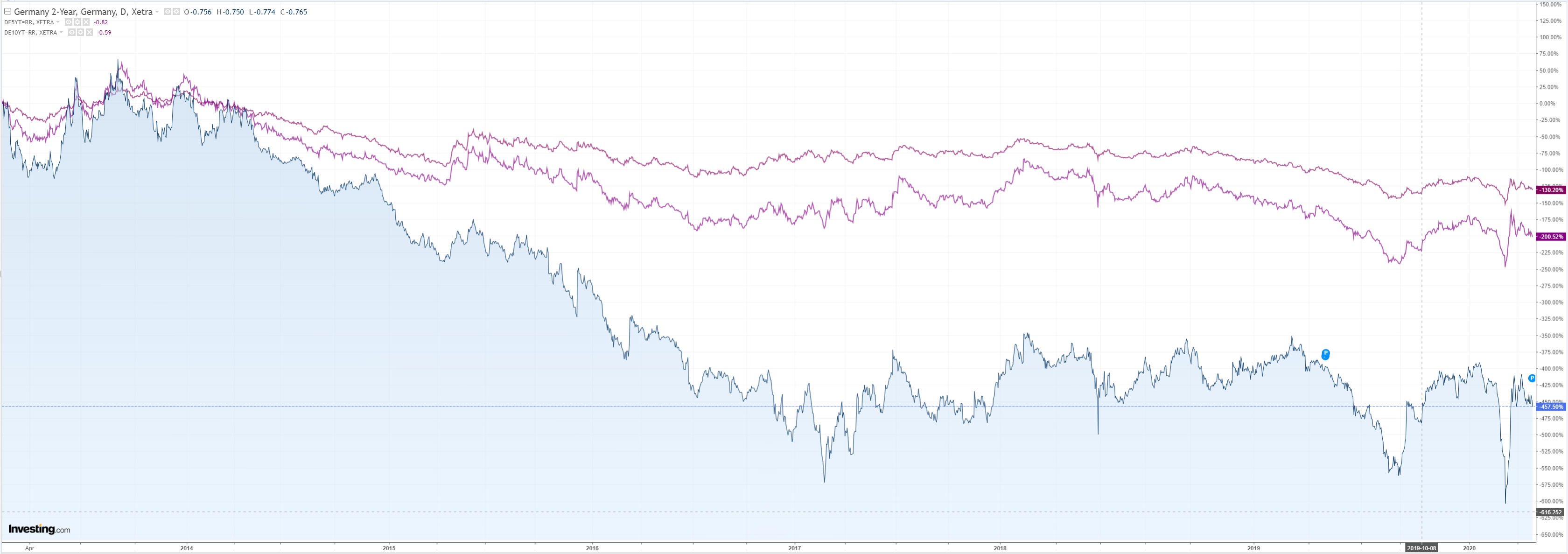

Bonds were stable:

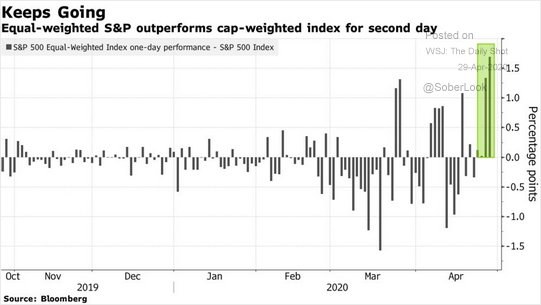

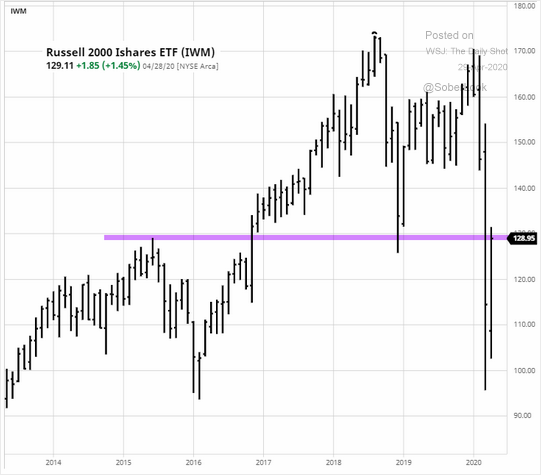

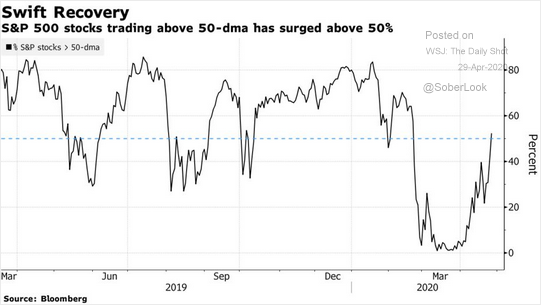

Stocks wow:

Westpac has the wrap:

Event Wrap

COVID-19 update: The global case count, according to the latest data from John Hopkins University, indicates 75k new confirmed cases worldwide on 28 April, vs 69k the previous day and vs 102k at the peak on 24 April. Whereas in March daily cases accelerated, in April they have trended sideways.

US official and infectious-disease expert Fauci said that early results of a closely watched clinical trial offered “quite good news” regarding a potential Covid-19 therapy made by biotechnology company Gilead Sciences Inc. Gilead issued a news release saying it had become aware of results from a trial showing its experimental drug remdesivir helped patients recover more quickly than standard care.

Unsurprisingly, there no major policy announcements in today’s FOMC statement. The Fed said it is committed to “using its full range of tools” and keeping the fed funds rate at near-zero “until it is confident that the economy has weathered recent events”. The statement reiterated that the Fed will continue to purchase Treasury securities to “support smooth market functioning”. The IOER rate was held at 0.1%, against speculation of a small hike to help bring the effective fed funds rate (at 0.04%) closer to the mid-point of the 0.0%-0.25% target range.

US Q1 GDP fell -4.8% annualised (vs est. -4.0%) with a sharper than expected slump in personal consumption (-7.6% vs est. -3.6%) as COVID-19 lockdowns impacted activity. This was, as anticipated, the largest quarterly drop since 2008, with a steeper decline expected in the Q2 (Bloomberg projects -37%). Non-residential investment also slumped, falling 8.6%. Q1 core PCE rose 1.8% (est. +1.7%, prior +1.3%). March pending home sales plunged 20.8%m/m, deeper than the median estimate of -13.6%.

Eurozone April economic confidence index fell to 67.0 (est. 73.2) from prior 94.5. German March CPI inflation fell to +0.8%y/y (but beat estimates of 0.7%) from 1.4% in Feb. Germany’s government statistics office forecast GDP for 2020 of -6.3%y/y and +5.2%y/y in 2021. The EU issues collated forecasts next week.

Event Outlook

Australia: Private sector credit is expected by Westpac to have risen by 0.3% in March, but measures to combat the coronavirus and the ensuing recession will see credit weaken in coming months. The Q1 import price index is expected to print at 1.0% as the softer AUD lifts import prices; however, fuel prices have fallen. The export price index is also expected to post a gain in the Q1 update (Westpac f/c 3.0%).

New Zealand: The final read for April ANZ business confidence is due. At -73.1, the preliminary result was already at a record low over the 32 year history of the survey.

China: The April manufacturing PMI (market f/c 51.0) and non-manufacturing PMI (market f/c 52.5) will be published. After recovering from a collapse in February, both indices are expected to remain in marginally positive territory.

Euro Area: The unemployment rate is expected to jolt higher to 7.8%. The labour market will continue to weaken as economic conditions deteriorate. The market anticipates that Q1 GDP will contract by 3.7%. With major disruptions to demand, April CPI inflation is set to print at a subdued 0.1%yr. The ECB will announce its policy rate decision. With little space for easing, the deposit rate is expected to remain at -0.5%; it is likely that the ECB will call on the fiscal authorities to do more.

US: March personal income (market f/c -1.5%) and personal spending (market f/c -5.0%) will both be hit by the contraction in economic activity. They will be accompanied by the March core PCE deflator, which will wane in the face of sluggish demand (market f/c -0.1%). Yet again, initial jobless claims will attract significant attention; the deterioration to date puts the unemployment rate above 15% in April. Finally, the Q1 employment cost index is expected to hold up at 0.6% before deteriorating through 2020, and the April Chicago PMI is expected to jolt lower to 37.7

The proximate trigger for last night’s rally was pretty ordinary Google results and a decent trial result for Remdesivir. As I’ve said before, treatment is actually a better outcome than a vaccine given it can be rolled out much faster.

I am beginning to doubt my own bear market rally thesis. There is no economy to speak of, the prospects for reopening remain poor, the risk of conflict and new shocks is extreme.

But, I have long thought that markets do not price recoveries in the contemporary world, they create them, simply via liquidity and wealth effects.

As we speak, the everything bubble is re-inflating no problems at all. Super aggressively. Stock gains are broadening and an EM bid is emerging. Risk appetite is extreme, seen in the sudden resurgence of Bitcoin.

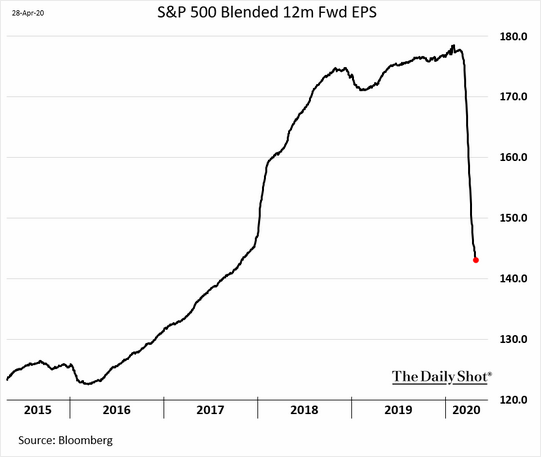

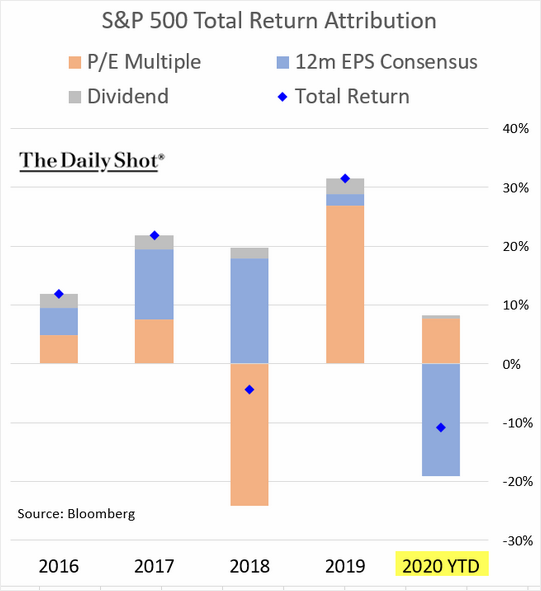

Even as earnings estimates keep falling:

It is all multiple expansion:

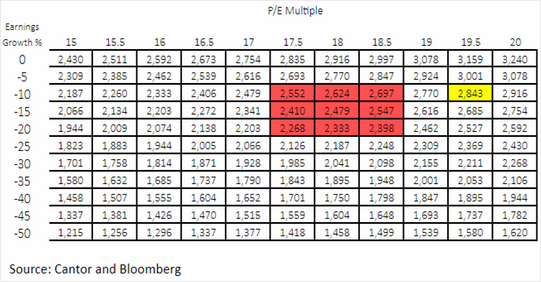

With valuations far above any sense:

Yet it is what it is.

For forex, the Australian dollar has now run so hard that it’s shot miles above fair value. Not least because the prospects for commodity prices is poor on the lack of any real economy to speak of.

But if we can re-inflate everything, with no earnings to speak of, then what is AUD fair value anyway? Nothing has any intrinsic value when it’s all measured against infinity.

If the rally keeps running purely on liquidity and bubble, then the US dollar will start falling, and the Australian dollar can keep hurtling into a wide-open universe.

At least until the only thing that matters – liquidity – is reined in.

That’s not even visible, via the FOMC statement:

The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.

The coronavirus outbreak is causing tremendous human and economic hardship across the United States and around the world. The virus and the measures taken to protect public health are inducing sharp declines in economic activity and a surge in job losses. Weaker demand and significantly lower oil prices are holding down consumer price inflation. The disruptions to economic activity here and abroad have significantly affected financial conditions and have impaired the flow of credit to U.S. households and businesses.

The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.

The Committee will continue to monitor the implications of incoming information for the economic outlook, including information related to public health, as well as global developments and muted inflation pressures, and will use its tools and act as appropriate to support the economy. In determining the timing and size of future adjustments to the stance of monetary policy, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

To support the flow of credit to households and businesses, the Federal Reserve will continue to purchase Treasury securities and agency residential and commercial mortgage-backed securities in the amounts needed to support smooth market functioning, thereby fostering effective transmission of monetary policy to broader financial conditions. In addition, the Open Market Desk will continue to offer large-scale overnight and term repurchase agreement operations. The Committee will closely monitor market conditions and is prepared to adjust its plans as appropriate.