DXY was up last night:

The Australian dollar paused:

Gold eased:

Oil is still falling:

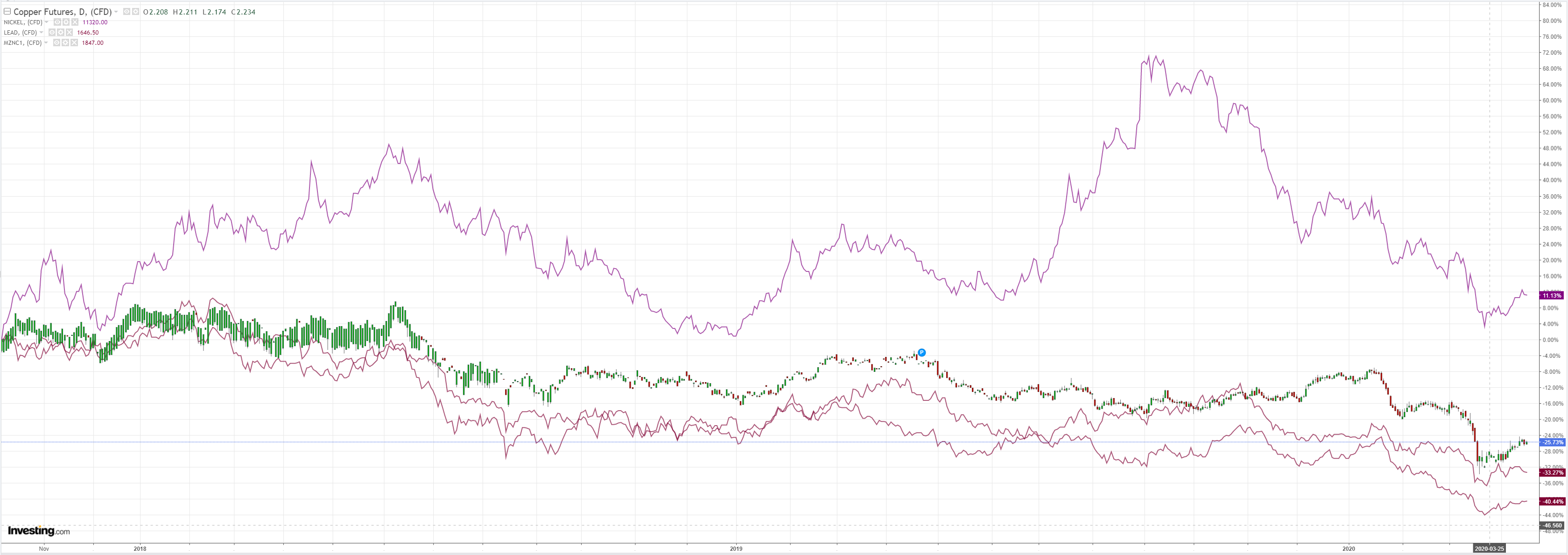

And dirt:

Miners firmed:

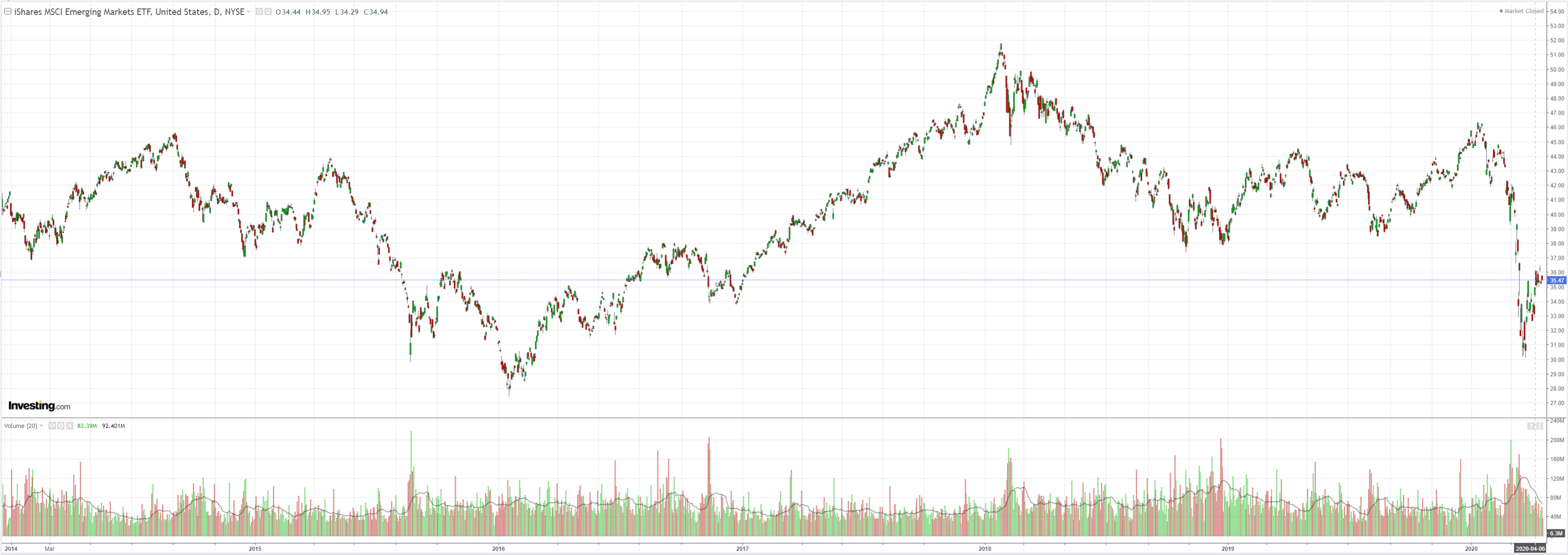

EM stocks were flat:

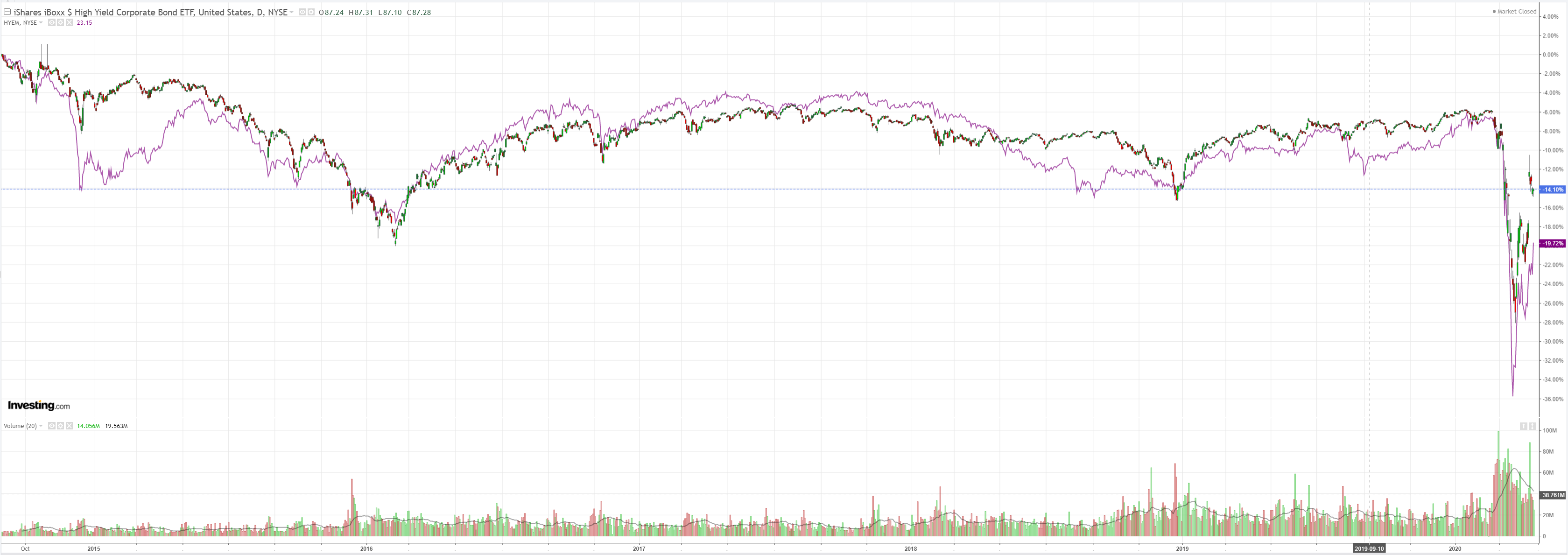

But junk took off:

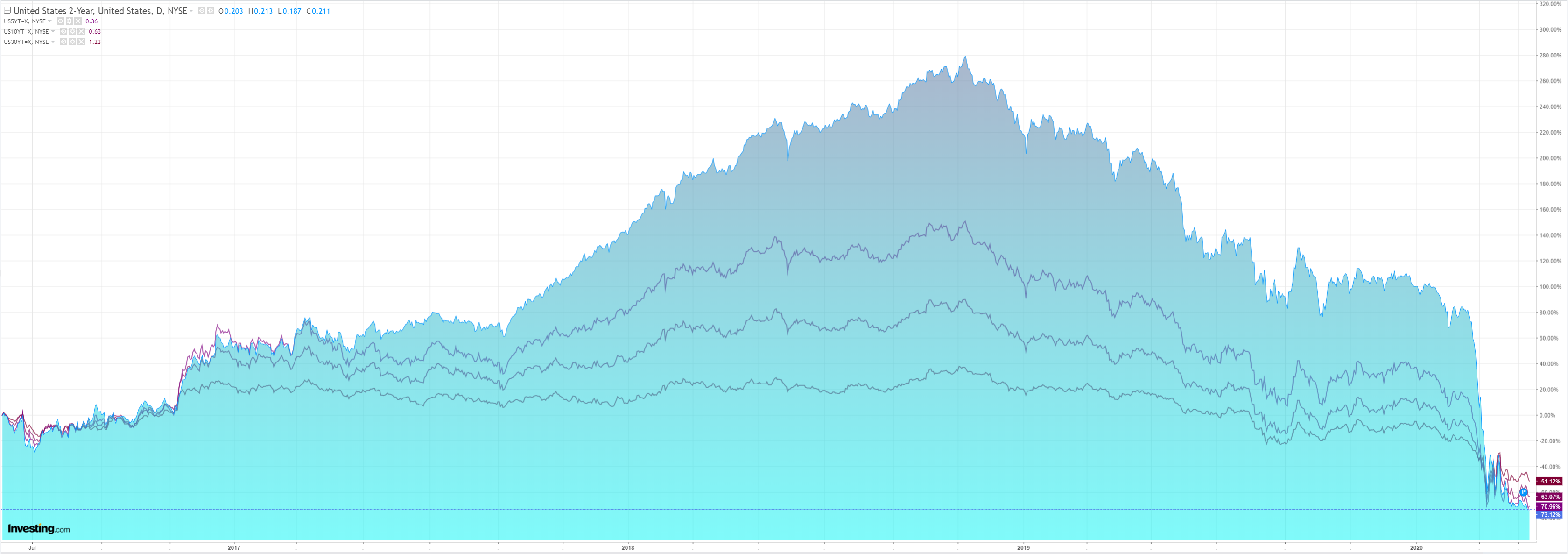

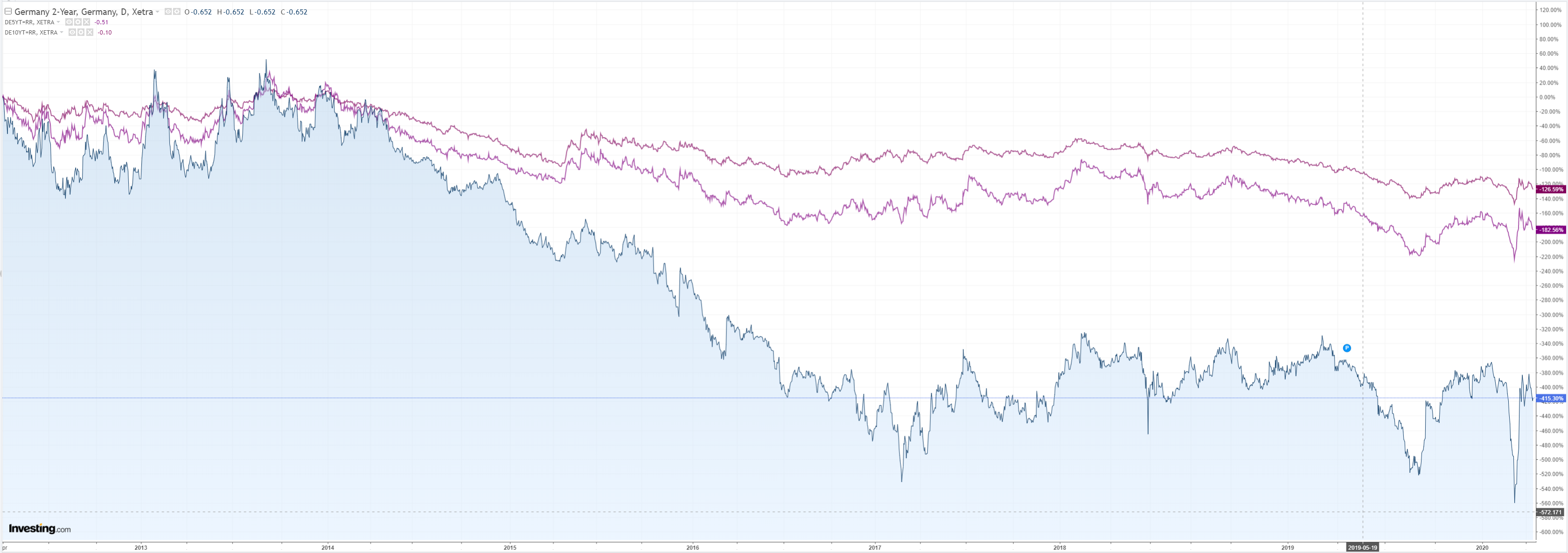

Bonds were bid:

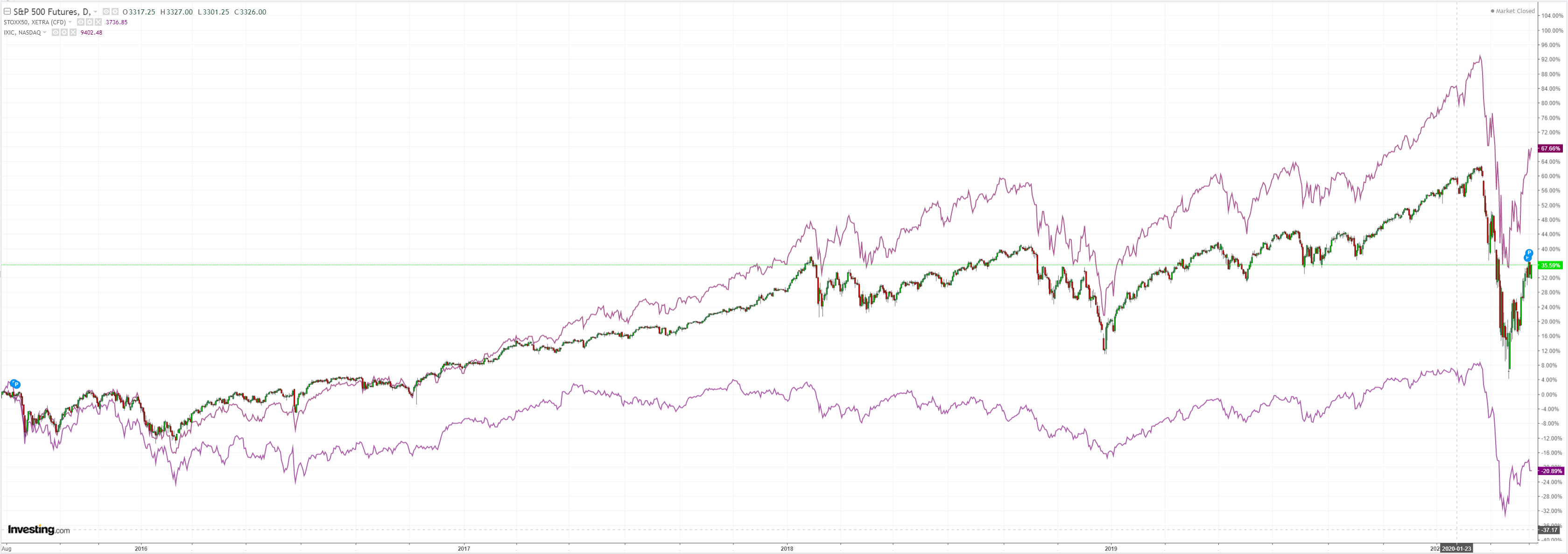

Stocks were firm. Nasdaq is in bizarro world:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 80k new confirmed cases worldwide on 15 April, vs 71k the previous day and vs 99k at the peak on 12 April.

The U.K. government will extend the country’s lockdown by at least three more weeks in an effort to stem the spread of coronavirus. Foreign Secretary Dominic Raab said the 23 March decision had helped to slow the spread of the virus but not yet to a manageable level. NY Governor Cuomo announced that he was extending the state’s lockdown by at least another month, to at least 15 May.

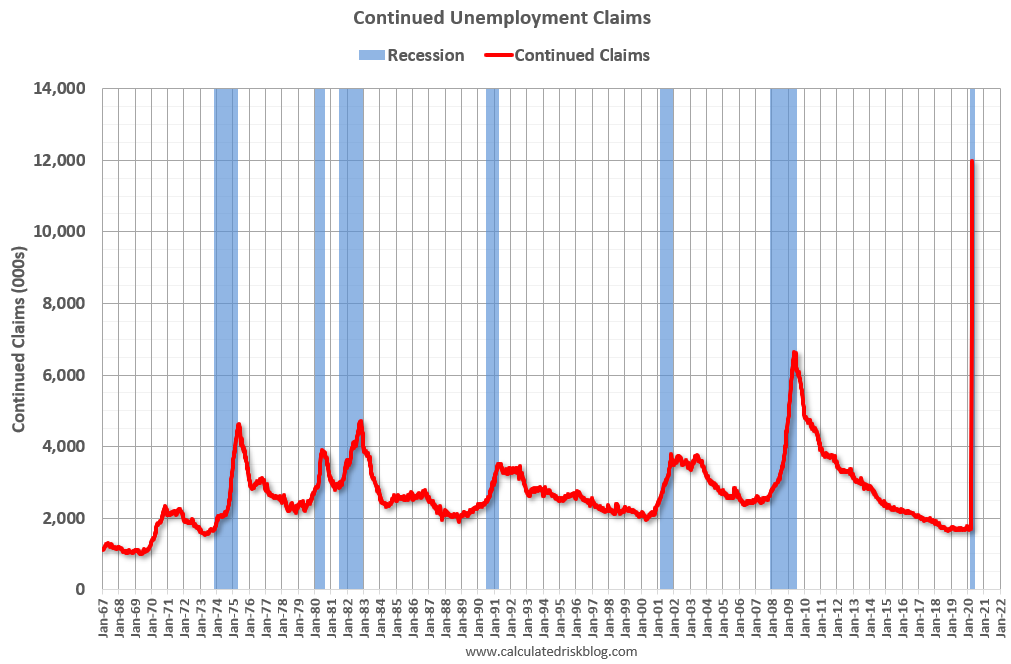

US weekly initial jobless claims fell 5.3mn (vs est. -5.5m) for the week to 11 April, bringing the total to 22m over the past 4 weeks. Continuing claims for the prior week at 12.0m (est. 13.3m), rose from 7.5m previously. US April Philly Fed survey slumped to -56.6 (est. -32.0, prior -12.7), reflecting the sharp falls seen in yesterday’s NY Empire survey. The sharpest falls were in the new orders, employment and hours worked sub-indices. US March housing starts fell more than expected: -22.3%m/m (est. -18.7%m/m) with permits falling -6.8%m/m (est. -10.7%m/m).

Event Outlook

China: There will be a number of key releases today, starting with Q1 GDP. The market expects a substantial contraction of 6.0%yr, well below the +6.0%yr posted in Q4 2019. March industrial production (market f/c -10.0%yr YTD), March retail sales (market f/c -12.5%yr YTD) and March fixed asset investment (market f/c -15.0%yr YTD) are also expected to be weak, albeit up on the February outcomes. This rebound should continue in coming months.

Singapore: March non-oil domestic exports are expected to reflect the disruptions to trade in the region and fall by 8.0%yr.

US: The March leading index will round out the day, the market expects a deterioration to -7.1%.

Here’s the chart that matters. US dole recipients:

Yeh.

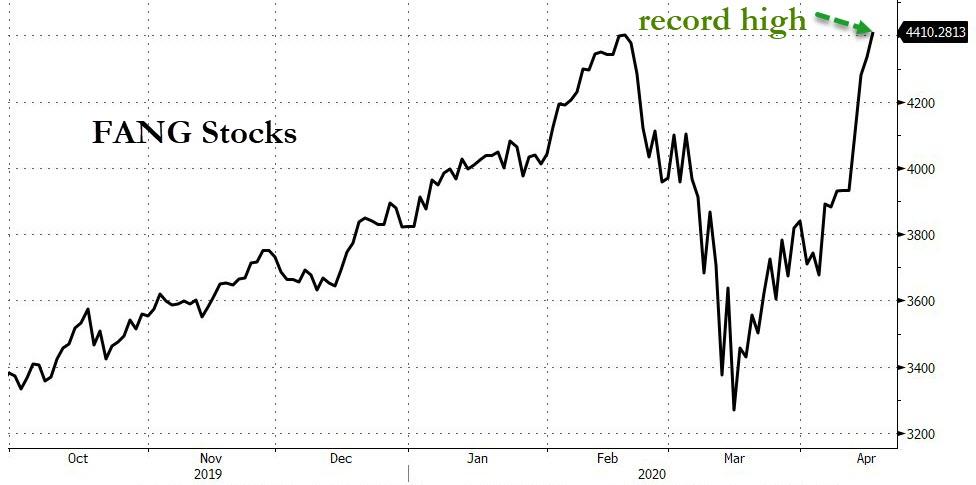

Just don’t tell the Nasdaq:

I have sympathy with tech outperformance. Companies will be chasing productivity gains more than ever after this shock. Some stocks, such as Netflix and Amazon, will benefit enormously. We’ve held some FANGs and other tech for these reasons.

But this is la la land stuff. Capex is going to be destroyed short and medium term. Tech earnings will get creamed with everything else.

Alas, for now, the Australian dollar is taking its lead from this crazy trade.