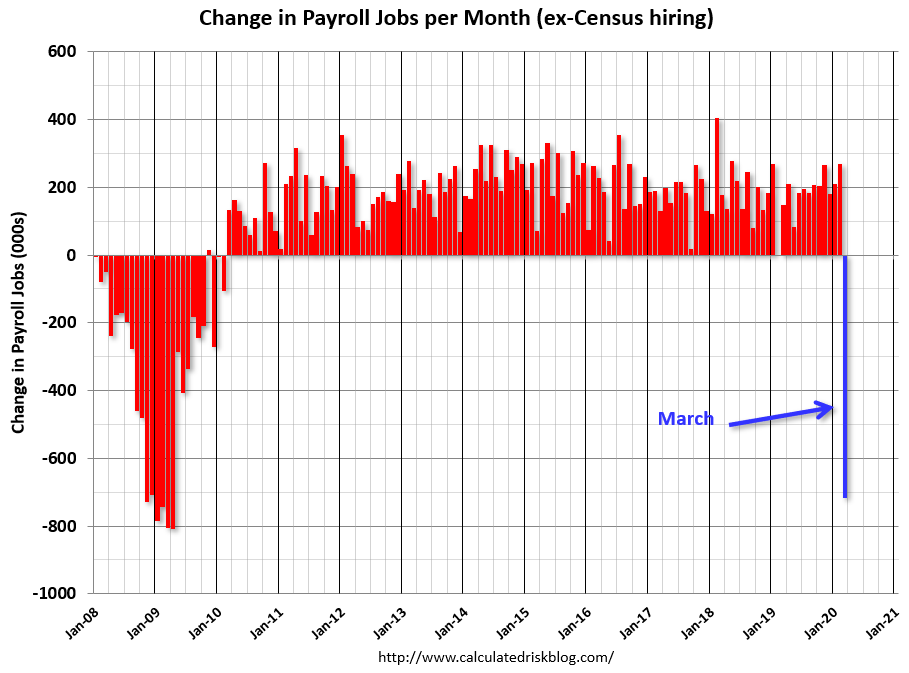

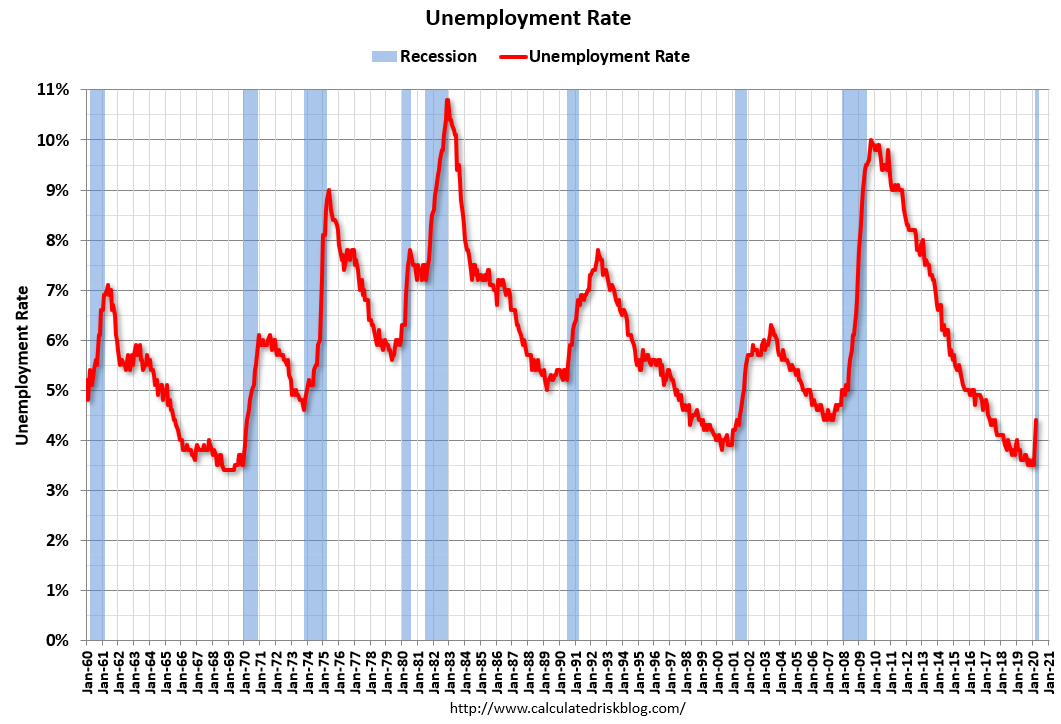

Total nonfarm payroll employment fell by 701,000 in March, and the unemployment rate rose to 4.4 percent, the U.S. Bureau of Labor Statistics reported today. The changes in these measures reflect the effects of the coronavirus (COVID-19) and efforts to contain it. Employment in leisure and hospitality fell by 459,000, mainly in food services and drinking places. Notable declines also occurred in health care and social assistance, professional and business services, retail trade, and construction.

…Federal government employment rose by 18,000 in March, reflecting the hiring of 17,000 workers for the 2020 Census.

…The change in total nonfarm payroll employment for January was revised down by 59,000 from +273,000 to +214,000, and the change for February was revised up by 2,000 from +273,000 to +275,000. With these revisions, employment gains in January and February combined were 57,000 lower than previously reported.

…In March, average hourly earnings for all employees on private nonfarm payrolls increased by 11 cents to $28.62. Over the past 12 months, average hourly earnings have increased by 3.1 percent.

Morgan Stanley offered some sobering analysis of how much worse it will get:

Advertisement

Disruptions to economic activity and closures of nonessential businesses have increasingly weighed on the labor market. In the past two weeks alone we have seen nearly 10 million workers file for unemployment benefits, indicating that upcoming employment data on payroll growth in April and through the second quarter is likely to be deeply negative.

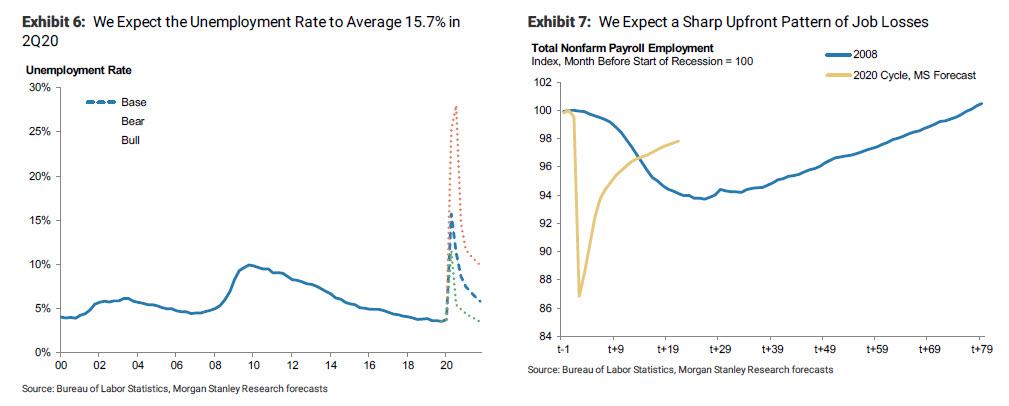

For the second quarter as a whole, we expect this will lead to a sharp rise in the unemployment rate to an average of 15.7% (Exhibit 6), the highest among records dating back to the 1940s. That builds in an assumption of cumulative job losses of 21 million in the second quarter, with a peak in the unemployment rate at 16.4% in May. In our bear case scenario, job losses amount to almost 40 million in 2Q, driving the unemployment rate up to 25%, and further economic weakness in 3Q20 leads the unemployment rate to drift up further to a peak of 28%, and the unemployment rate remains persistently higher over the forecast horizon in this scenario.

The pattern of job losses will largely follow the GDP pattern, although we do foresee some long-term job losses persisting over our forecast horizon. That may be particularly the case among small businesses (<100 employees), which BLS data indicate comprise more than 55% of total employment. We expect that payroll employment will begin to expand in June 2020, but will remain 2.7% below its pre-recession peak at the end of 2021. Nevertheless, that would feel like a stronger recovery compared to the persistent labor market weakness seen in the 2008 cycle (Exhibit 7).

The base case seems right to me. The one upside to US failure in containing the virus is greater herd immunity and reduced possibility of a second virus wave which is what underpins the MS worst case.

Note that MS sees swift recoveries from these unemployment levels. That is fair enough versus previous downturns but they are too aggressive. The delinquency shock emanating from such levels of unemployment, despite public support, will choke the banking system and delay recovery. Perhaps not as badly as the GFC but badly enough.

Advertisement

This is a US earnings cataclysm in the making and that matters to forex. The one relationship with the Australian dollar that has been unshakable throughout this crisis is with the S&P500:

If stocks haven’t bottomed then neither has the Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.