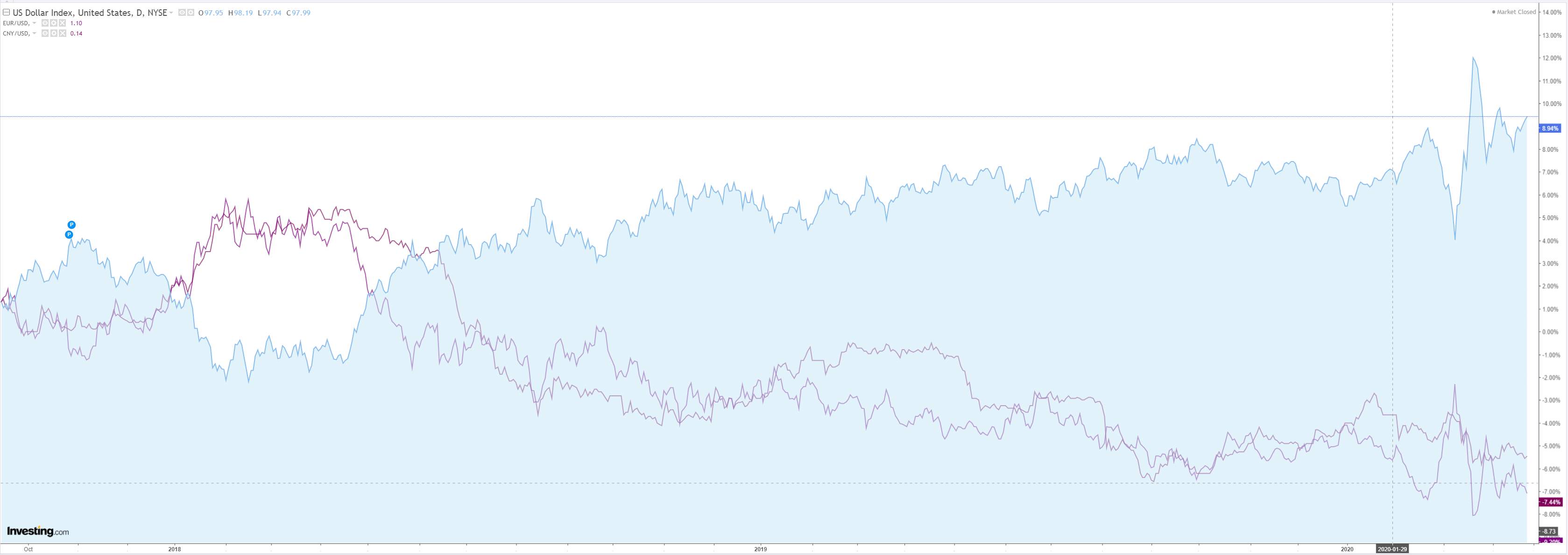

DXY was up last night:

That sat on a rebounding Australian dollar:

EMs were caned:

Gold rebounded too:

Oil a little:

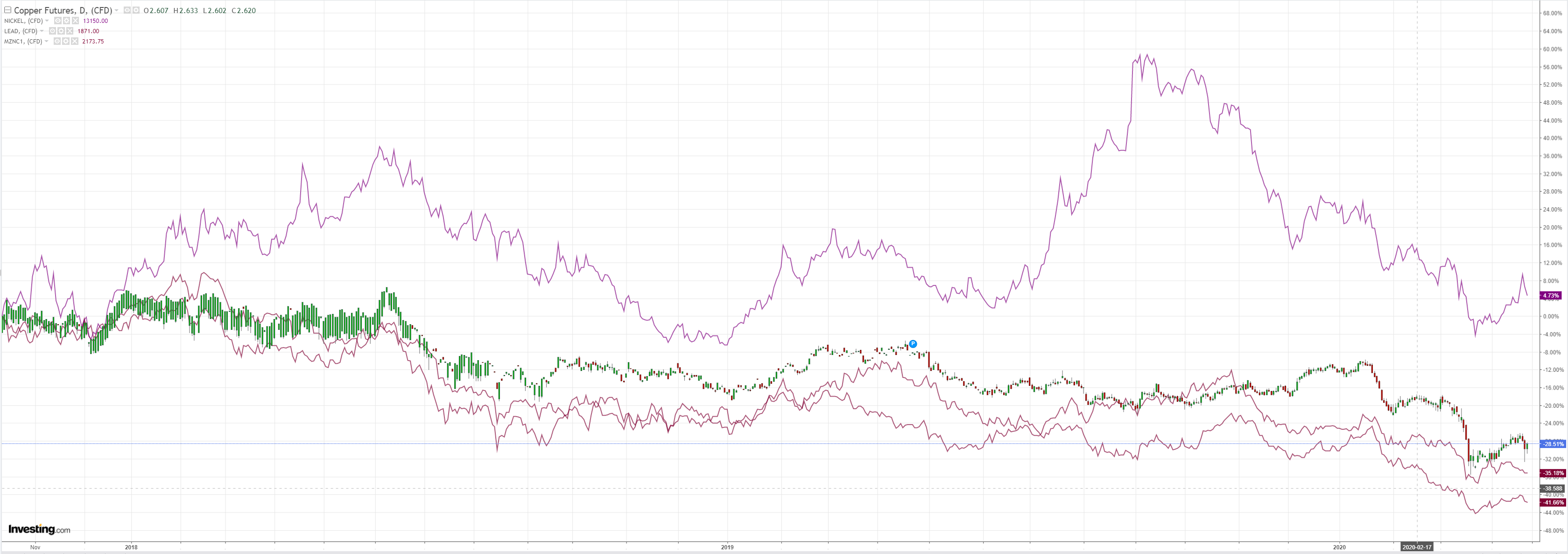

Not dirt:

But miners:

And EM stocks:

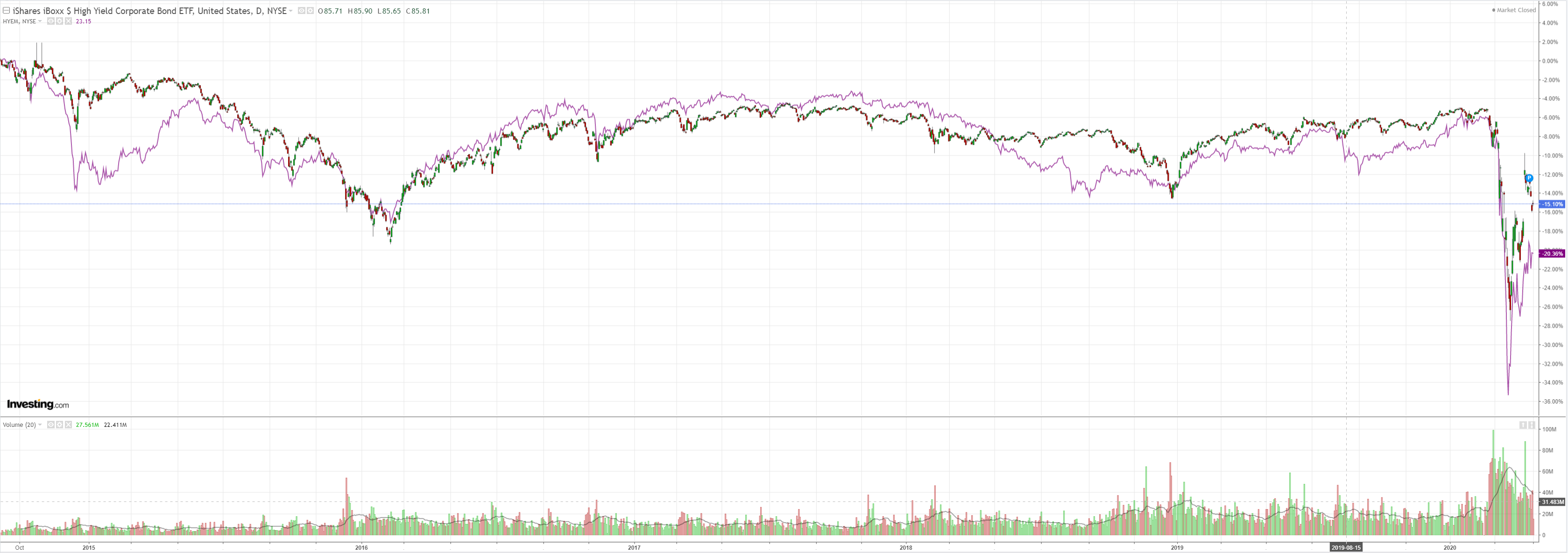

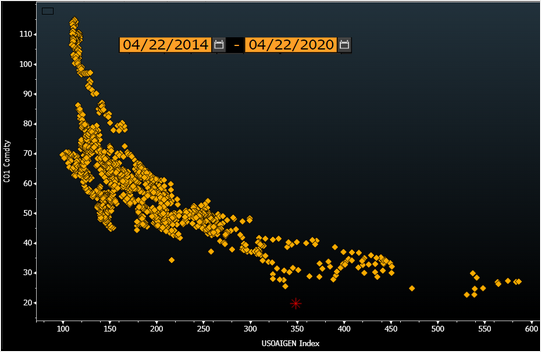

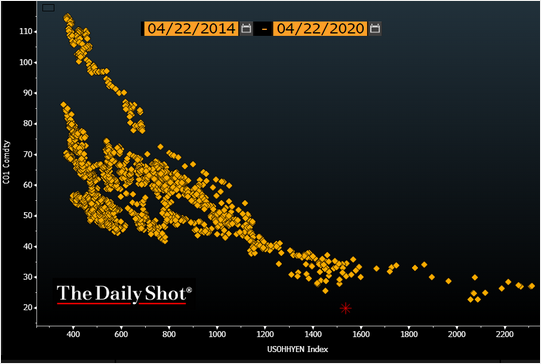

Perhaps the most important chart on the world, junk, edged higher:

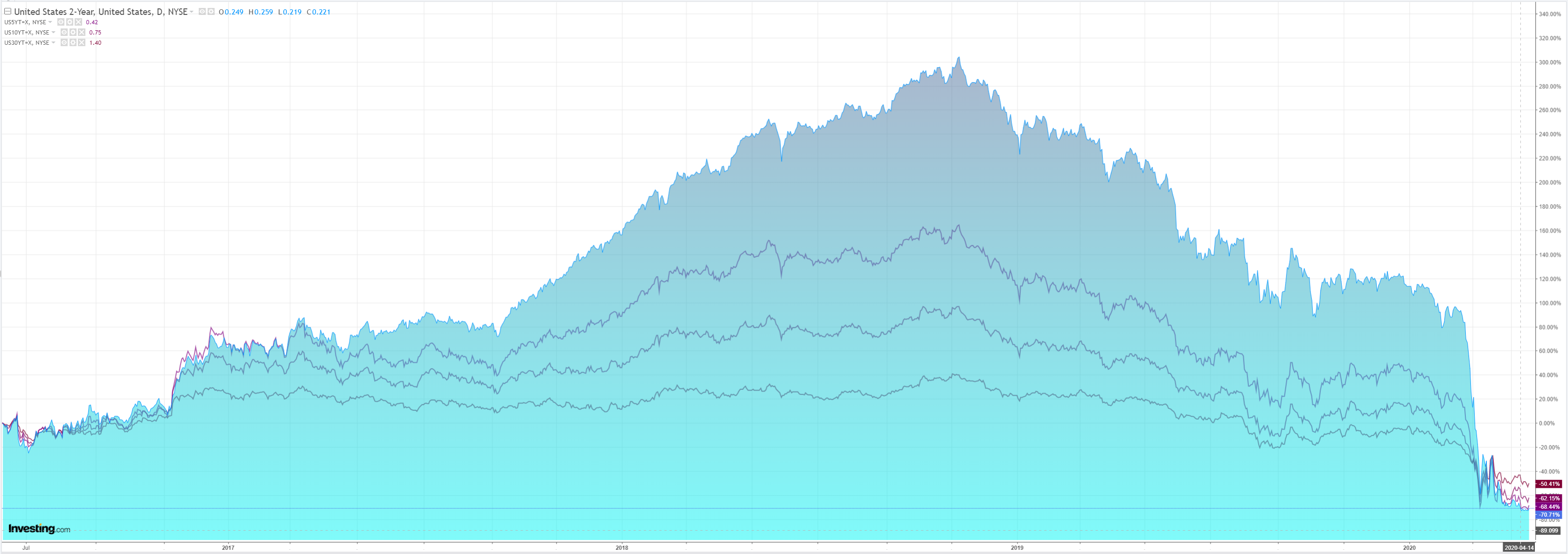

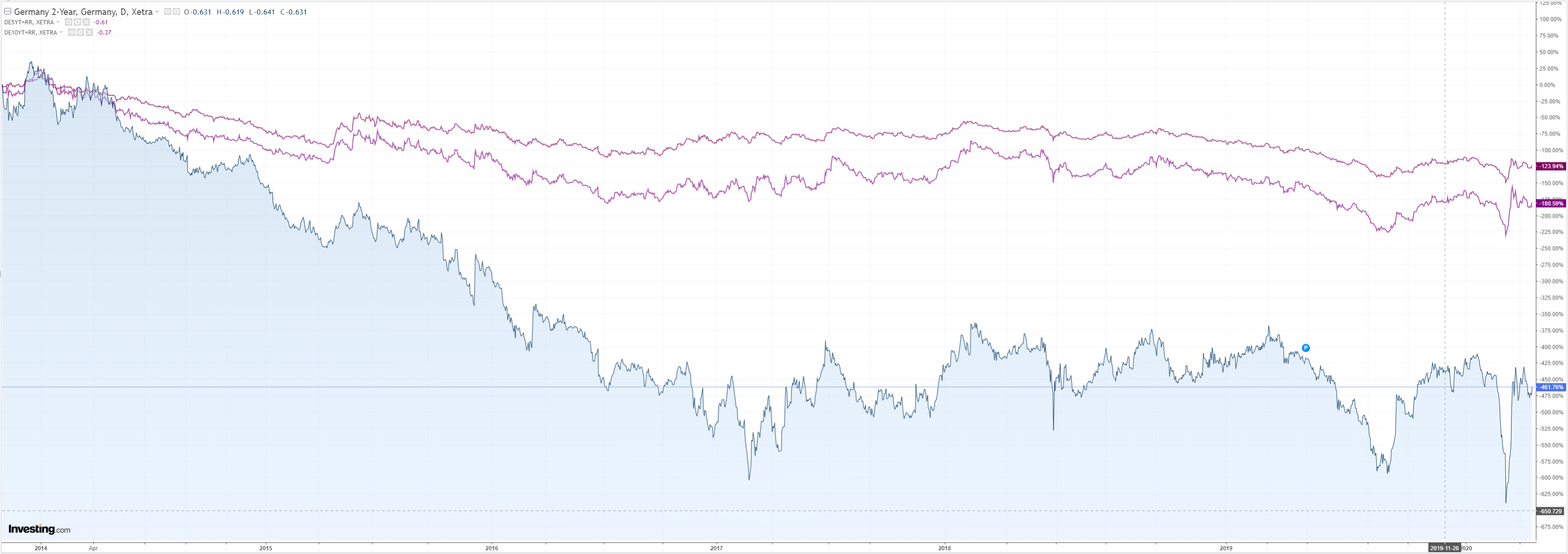

Bonds sold:

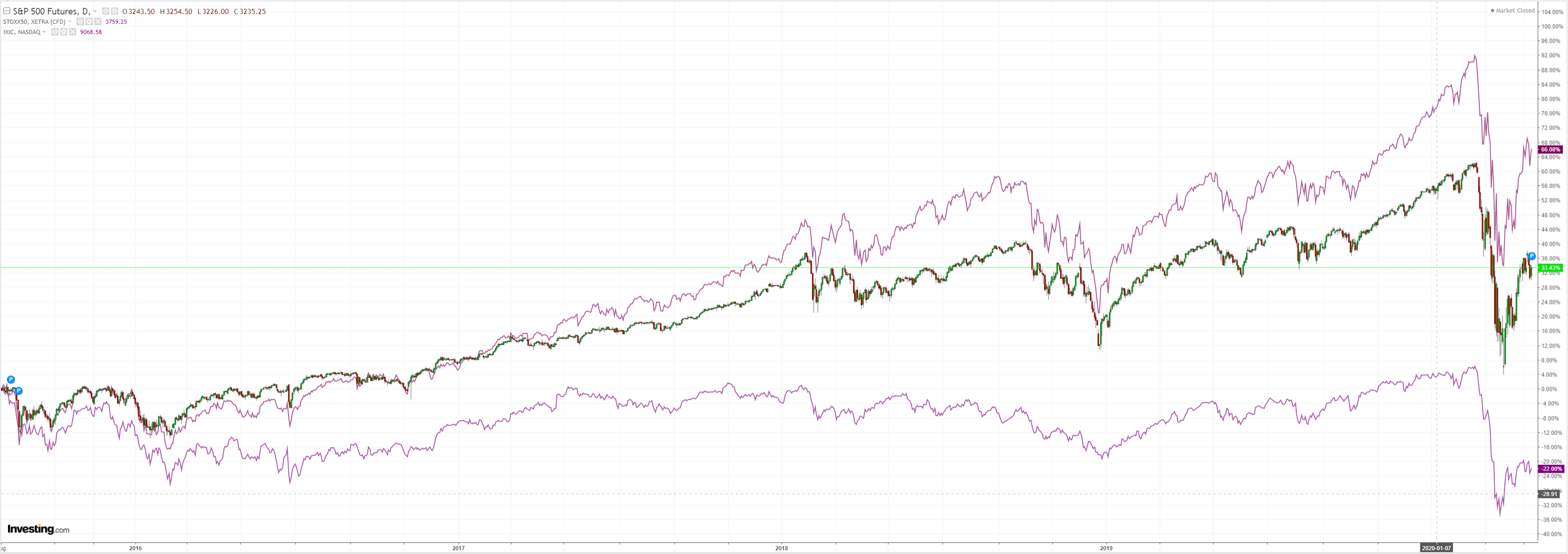

Stocks bought the dip:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 89k new confirmed cases worldwide on 21 April, vs 71k the previous day and vs 99k at the peak on 12 April.

President Trump tweeted “I have instructed the United States Navy to shoot down and destroy any and all Iranian gunboats if they harass our ships at sea”. US naval ships have recently been approached by Iranian speedboats in the Arabian gulf.

UK March CPI was in line with estimates as the headline measure slipped to 1.5%y/y (prior 1.7%y/y) and core slipped to 1.6%y/y (prior 1.7y/y%). Although RPI rose to 2.6%y/y (est. 2.3%y/y, prior 2.5%y/y) the deflationary pressures are expected to appear.

Eurostat published regional debt to GDP ratios. Eurozone stood at 84.1% with EU-27 at 77%.

Event Outlook

Australia: The NAB business survey is poised for a substantial fall in the Q1 update, with the monthly survey showing that confidence fell to -66. In addition, the ABS will release the preliminary estimate for the March trade balance. Exports and imports will both be dented further by travel restrictions and trade disruptions; however, exports will be cushioned by a rebound in iron ore shipments, post Cyclone Damien.

Japan: April Nikkei flash PMIs are due, and further deterioration is expected from an already weak level.

South Korea: The preliminary read for Q1 GDP will be released. The market expects a contraction of -1.5%, however year-over-year growth will remain positive at 1.0%yr.

Europe: April Markit flash PMIs are due for the Euro Area, Germany and the UK.

US: The April Markit manufacturing PMI (market f/c 35.0) and services PMI (market f/c 30.0) are both expected to decline sharply. Following this, March new home sales are expected to fall by 16.3% as the momentum seen prior to the lockdown dissipates. In line with other regional surveys, the April Kansas City Fed Index is set for another soft print (market f/c -37). Finally, initial jobless claims will attract significant attention after four unprecedented weeks.

Here’s the thing. With oil going below zero we would normally expect to see major spread widening in the junk debt markets that fund US shale. It’s just not happening:

Why? Because the Fed is buying fallen angels junk debt, an implicit warning that it will the rest of the market if it has to.

So, despite this:

There is no credit spreads widening feedback loop to disturb stocks and risk.

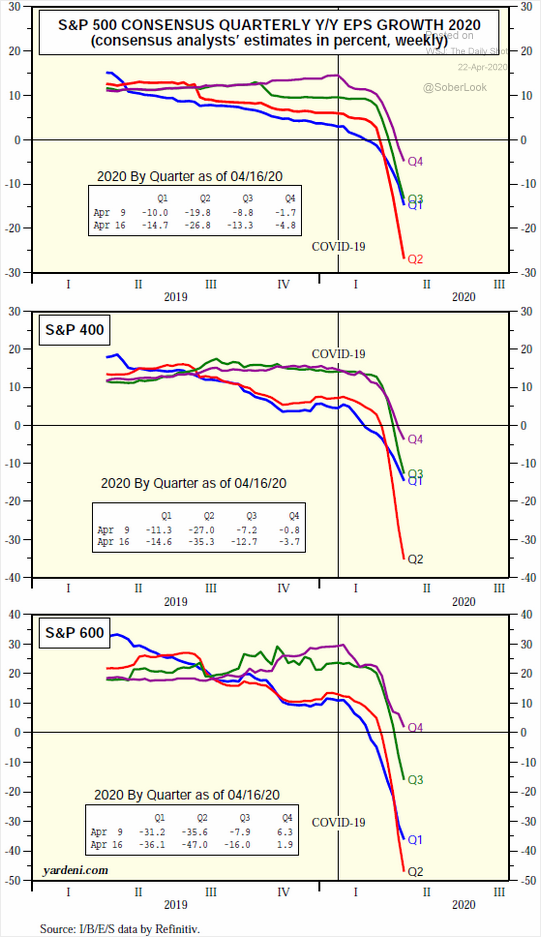

The Fed has literally frozen the US (and global) junk bond index in stasis allowing stocks to bid without earnings despite an unimaginable oil price and earnings calamity.

That protected risk appetite is driving the Australian dollar.