Australian mortgage lenders are reportedly undertaking stricter employment checks of pre-approved loans, suggesting they are rationing credit in response to the COVID-19 economic shutdown:

Homeloanexperts.com.au managing director Otto Dargan said… “A mortgage approval is no longer as certain as it was before the pandemic. Borrowers shouldn’t assume that the lender will honour their pre-approval when they find a property”…

“We’ve been warning customers not to buy a home if their income is unstable so we haven’t had any customers left high and dry. From what we can see it appears that lenders are doing this check for all loans.”

Mr Dargan said most lenders have started doing employment checks as late as a day or two prior to the loan being released…

“The problem is that if you have committed to buy a property and then you fail the employment check, then you may lose your deposit and be unable to complete the purchase. Even if your loan is approved, the approval may be withdrawn.

This has negative feedback loop written all over it.

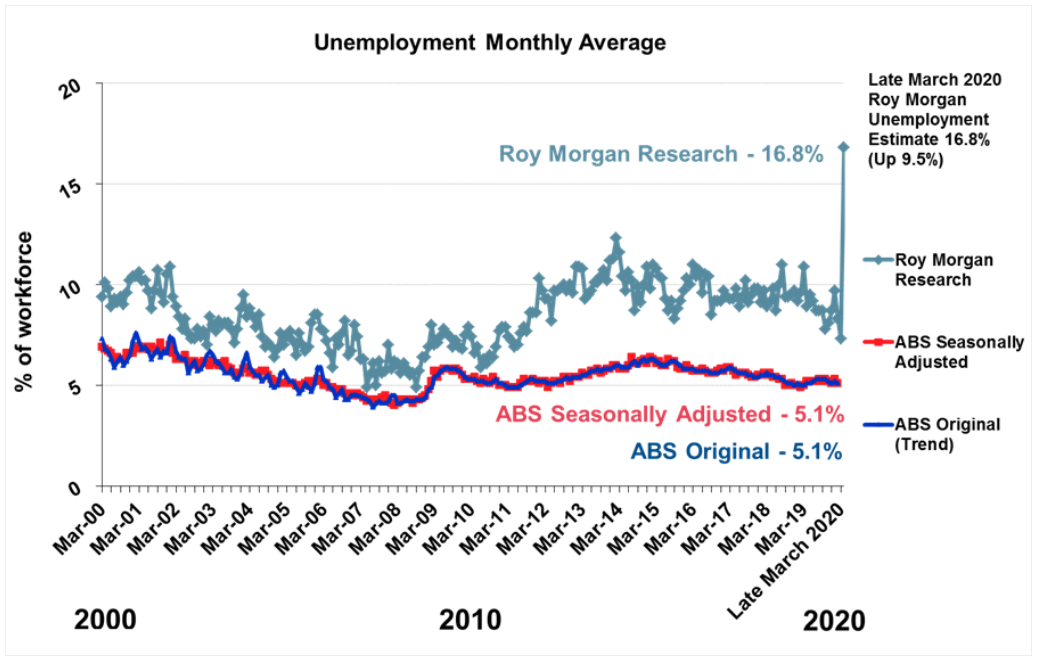

With unemployment across Australia surging (see next chart), and the Grattan Institute forecasting that up to 3.4 million Australians could lose their jobs, banks are likely to tighten mortgage credit even further.

This would shatter buyer confidence, since nobody could be assured that they can settle, as well as result in failed settlements. Both of which would send Australian property prices and transaction volumes plummeting.

Easy credit was the foundation of Australia’s property bubble. Therefore, credit tightening would necessarily send the property market into a tailspin.