Not for now, but the risks are growing. In the end, it will to a significant degree come down to hard to forecast subjective or qualitative assessments around the sovereign’s risks.

• Australia’s AAA S&P sovereign rating will come under renewed surveillance over coming weeks. The heightened uncertainties around the economic impacts of the COVID-19 virus, combined with the significant Federal fiscal response – to be largely debt funded – and the Commonwealth’s well-known weak “external position” are all central to concerns.

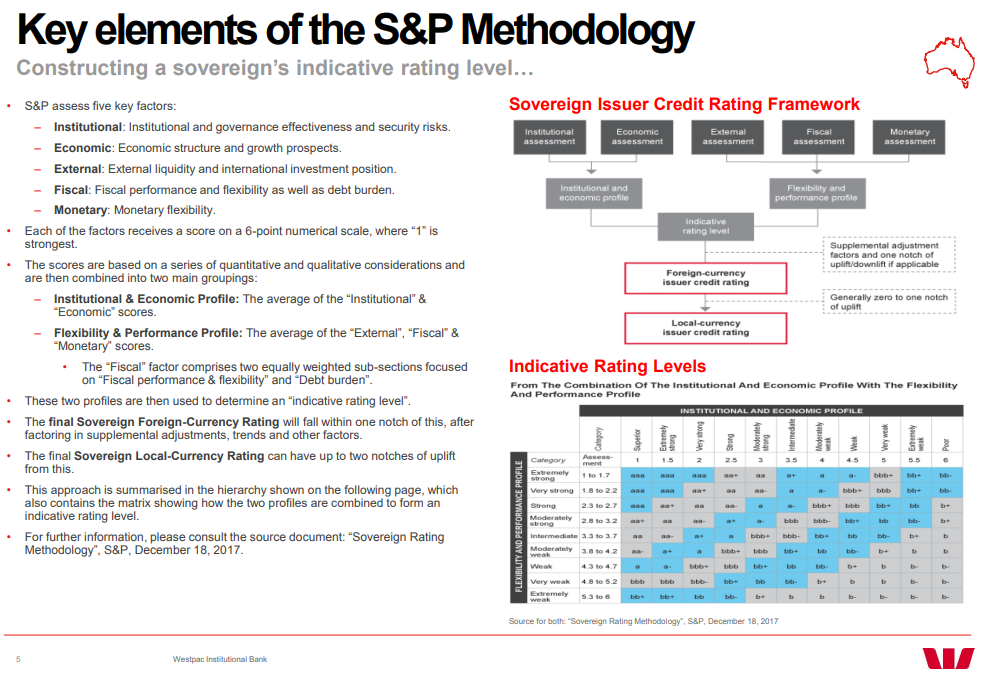

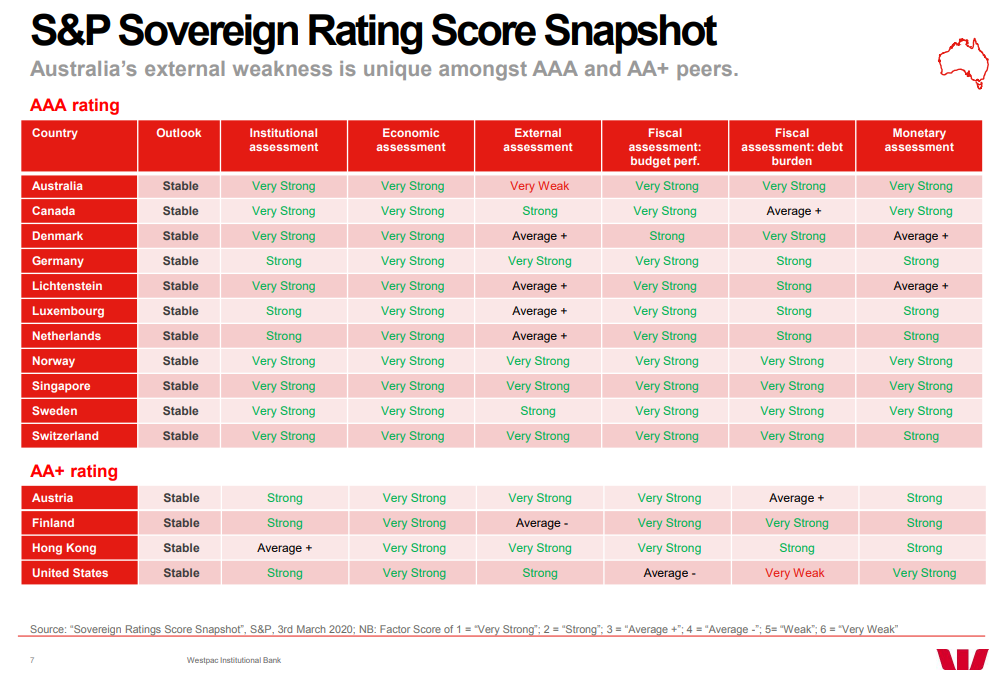

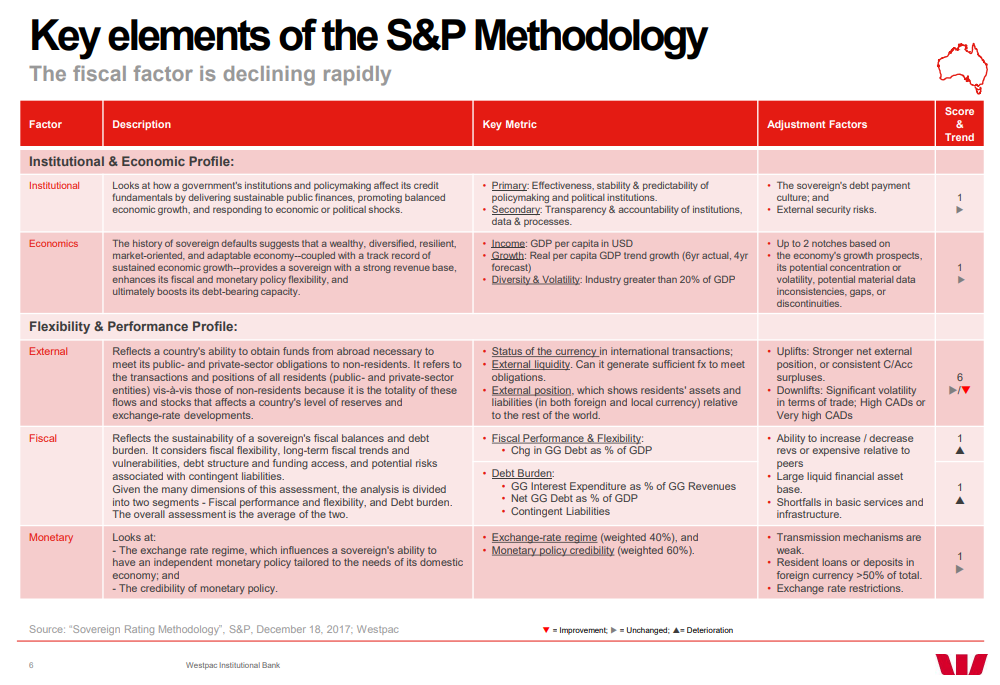

• The weak external position arises out of Australia’s historical dependence on global funding to compensate for a deficit of domestic savings relative to investment opportunities. While this has lessened recently, as the current account moved into surplus, it remains the greatest source of vulnerability for Australia’s sovereign credit rating. The fact most global economies are materially increasing their fiscal spending, and hence borrowing programmes, puts Australia in a delicate position as we compete in the global market for investment dollars. However the current contribution to the quantitative ratings methodology (refer next few pages) from this factor cannot fall any further. So it is up to other factors to deteriorate sufficiently to put the rating at risk.

• When, in July 2016, S&P put Australia’s sovereign rating on “negative outlook”, the main reason was that Australia had been slow to return to budget surplus, with forecast revenues continually falling short and deficits continuing to widen. That situation had improved sufficiently by 20 September 2018 for the outlook to again move back to “stable”. However, even before the COVID-19 virus began its destructive influence, Australia’s economy was slowing such that the projected surpluses for 2019/20 and beyond were again a forlorn hope. So adding the virus impacts to an already weakening economy has increased the risks to the credit rating substantially.

• To make an initial assessment of those risks, on the next few pages we outline the S&P methodology as a starting point in assessing what sort of criteria are crucial to the ratings outlook. Having established what the S&P methodology is, and Australia’s starting point within them, we can then move on to assess what the quickly changing current circumstances may mean.

• With the pace of change so rapid, it is a difficult task, but our initial thoughts are:

– For now, Australia will not be downgraded, although a return to a “negative outlook” is possible. The primary source of concern will around the fiscal position. The debt burden, on current estimates, looks like almost doubling over the next 12-18 months. If we take that fact on its own, then it would, from a purely quantitative approach, open the route to a downgrade. That is because what was previously one of Australia’s very strong attributes, would decline to an average/neutral contribution. However, as mentioned, we are reminded that there is some subjective “give” in the metrics. As S&P itself recently commented (refer next page): “While a stimulus package would temporarily weaken the general government budget, this, by itself, is unlikely to strain Australia’s creditworthiness. Importantly, we believe the Australian government remains committed to medium-term fiscal discipline.” So S&P’s view as to that medium-term commitment will be critical. It is way too early to assume that the Government has lost that commitment.

– With all of that in mind, it is our sense that the sovereign’s AAA rating is not under immediate threat but it is certainly nearing limits. We think that the ratings agency will be slow to penalise the government for its current responses in a time of unprecedented uncertainty. To the contrary, by exhibiting the flexibility, resilience and institutional

processes necessary to offer a targeted stimulus, maintain social cohesion and underpin the health and job security of its citizens, the sovereign will have demonstrated some of its strengths. With that in mind, we think that S&P would, if it undertook any action, be more likely to return the Commonwealth to a “Negative Outlook” before it put it on a downgrade watch-list or undertook an actual downgrade.

– In the end, whether or not S&P choose to shift their rating will come down to what parameters they assume for the economic outlook and it’s rebound pace. More importantly, it will rely largely on their subjective calls with regard the factors in their credit rating framework, especially given that quantitative inputs into that analysis are currently very difficult, if not impossible, to calibrate. Indeed, we are even questioning whether the current equal weights given to each factor might even change in favour of one overall consideration given theses extraordinary circumstances. In the post-GFC environment, ratings agencies were known to shift a number of their ratings methodologies. They could easily “move the goalposts” again given the current extraordinary circumstances.

Of course the rating is cooked. By the time the crisis is done in years, I expect we’ll be shoved out of high grade:

UBS gives nice snapshot:

Advertisement

The JobKeeper subsidy materially raises the total Government (Federal + State) fiscal stimulus, so far, to ~$206bn, or ~10.3% of (2019) GDP. Of this, ~$71bn is in Q2-20 alone, equivalent to an extraordinary ~14% of quarterly GDP. In addition, the authorities (RBA/AOFM/Treasury) also created credit support & guarantees of $125bn (or 6.3% of GDP). Together, these measures total ~$331bn, or ~17% of GDP. Notably, total Government (Federal + State + Local) debt is now ~$1tn or ~48% of GDP. But fiscal measures are likely to increase ahead as “The Government will continue to do what[ever] it takes”, and “provide updates on further business cashflow support in coming days”; while State (& Local) Governments also defer various taxes and charges including rent. There will also be a hit to the budget from economic parameters (estimated for the Commonwealth to be ~$5bn for each 1%pt downgrade of nominal GDP). Hence, the total Government budget deficit in 19/20 is set to be somewhere around ~$200bn, or ~$150bn larger than Budgets currently project. Furthermore, in 20/21, the total deficit could be $250bn more than expected at ~$290bn or ~16% of GDP, the largest since WW-II. This would see total Government debt leap by ~$500bn (from now) towards $1.5tn or ~80% of GDP in 20/21, the highest since the 1950’s, albeit still far below other major economies. Indeed, the impact on bond yields will likely be significantly offset with RBA Lowe promising “no limit on what we can buy” – with bond purchases in just over a week already $24bn. While at some point the RBA will slow its daily average of ~$3bn, if it kept buying at the current pace, it would absorb all our projected ~$500bn increase in debt within ~two quarters.

The problem is, we have no way to grow the economy and budget revenues once the virus has passed:

easy China bribe options are over and mass immigration will become highly problematic;

mining booms are over;

house price inflation and conspicuous consumption is over.

It will be a very difficult economic grind made worse by endless, self-defeating austerity.

Advertisement

That is, until we get over ourselves and MMT our way out of it, rendering ratings agencies redundent.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.