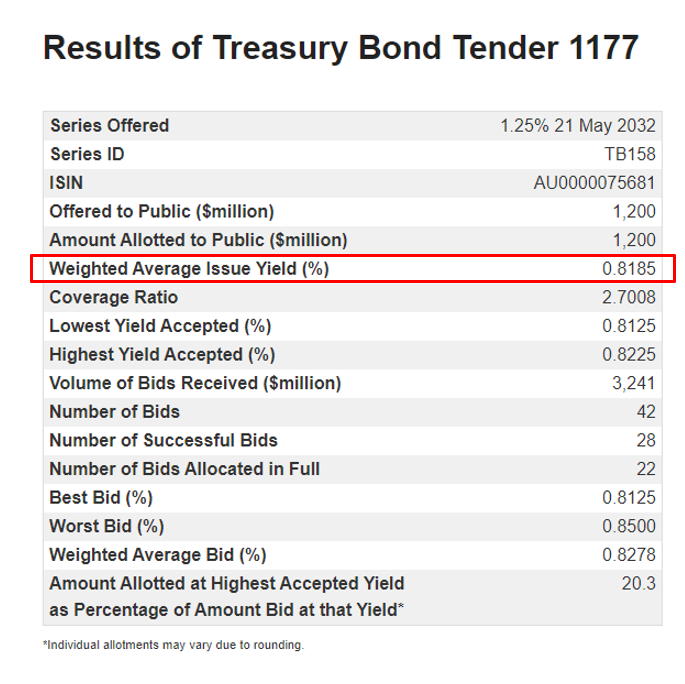

Last week, the Australian Office of Financial Management (AOFM) issued a $1.2 billion 10-Year Treasury Bond at a yield of only 0.82%:

Thus, with Australia’s inflation rate running at 1.8% currently, the federal government effectively borrowed at a negative real interest rate of nearly 1%.

Put another way, even if the federal government only returns inflation on whatever it uses these borrowings for (e.g. infrastructure investment), then the Australian taxpayer will still come out ahead.

Advertisement