DXY took off Friday night and is suddently in the frame for its traditional safe haven melt-up:

The Australian dollar was trashed to GFC lows:

Gold has begun liquidating. If the selling gets moving, this is the time of cycle to buy it:

Oil tried but is stuffed:

Likewise metals:

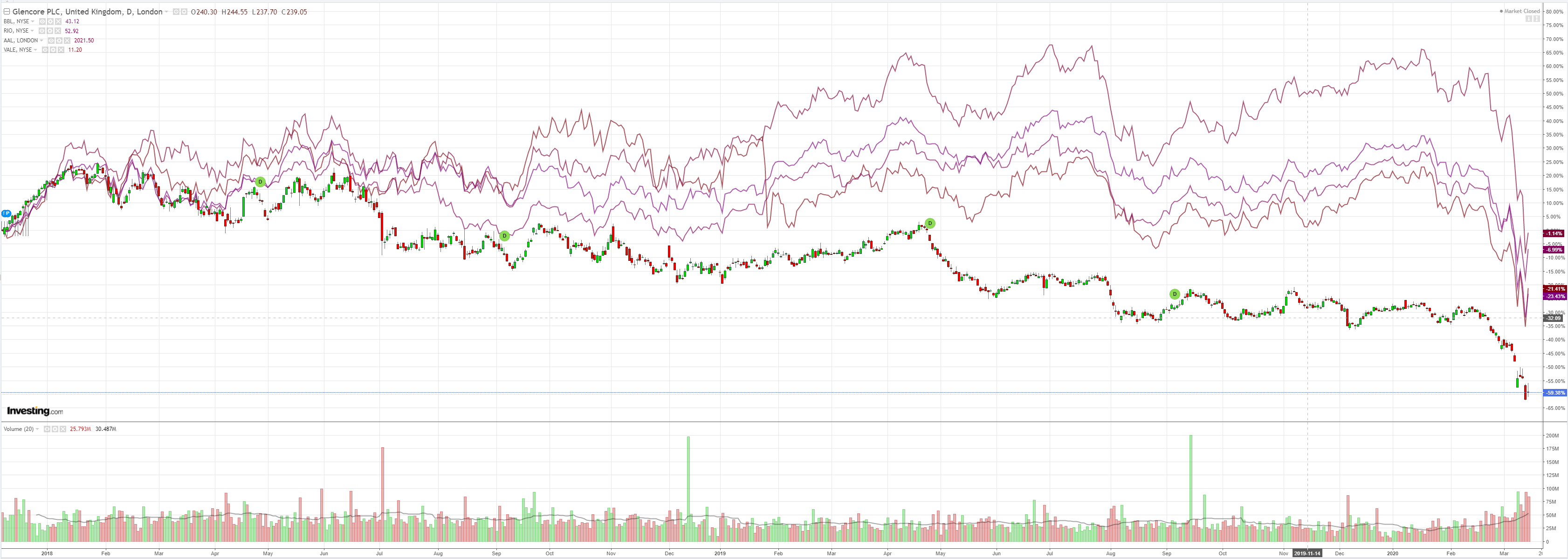

Miners dead bat bounced:

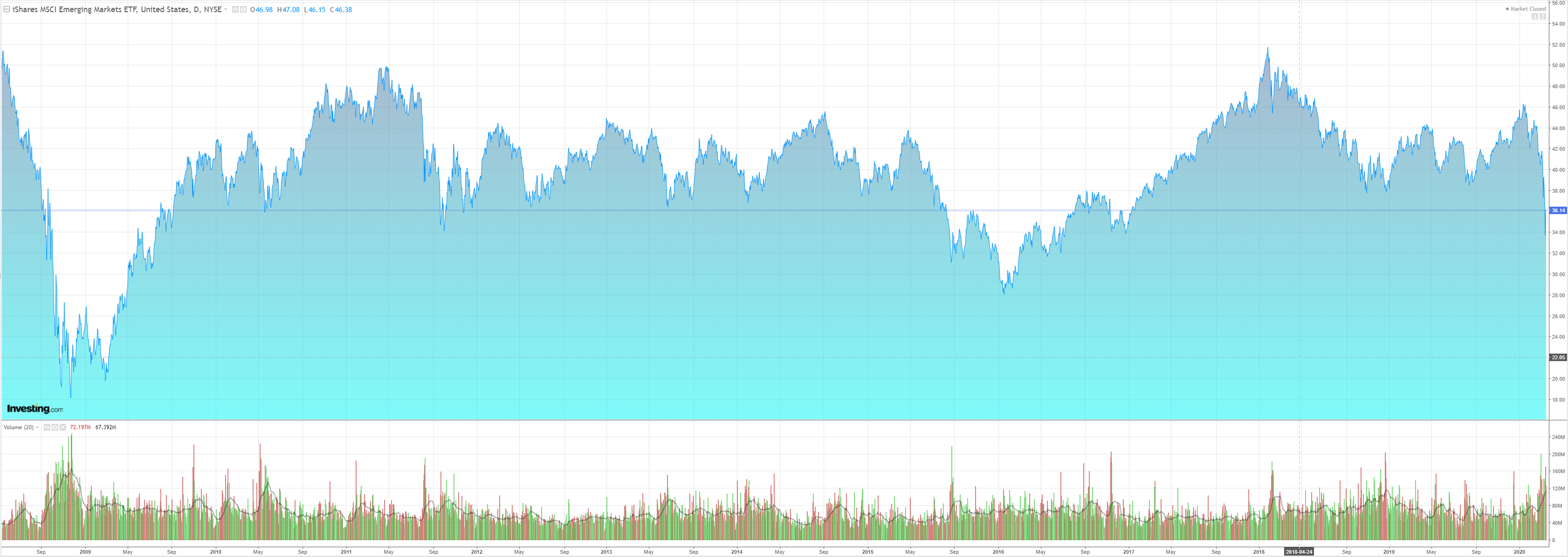

EM stocks too:

High yield is cratering:

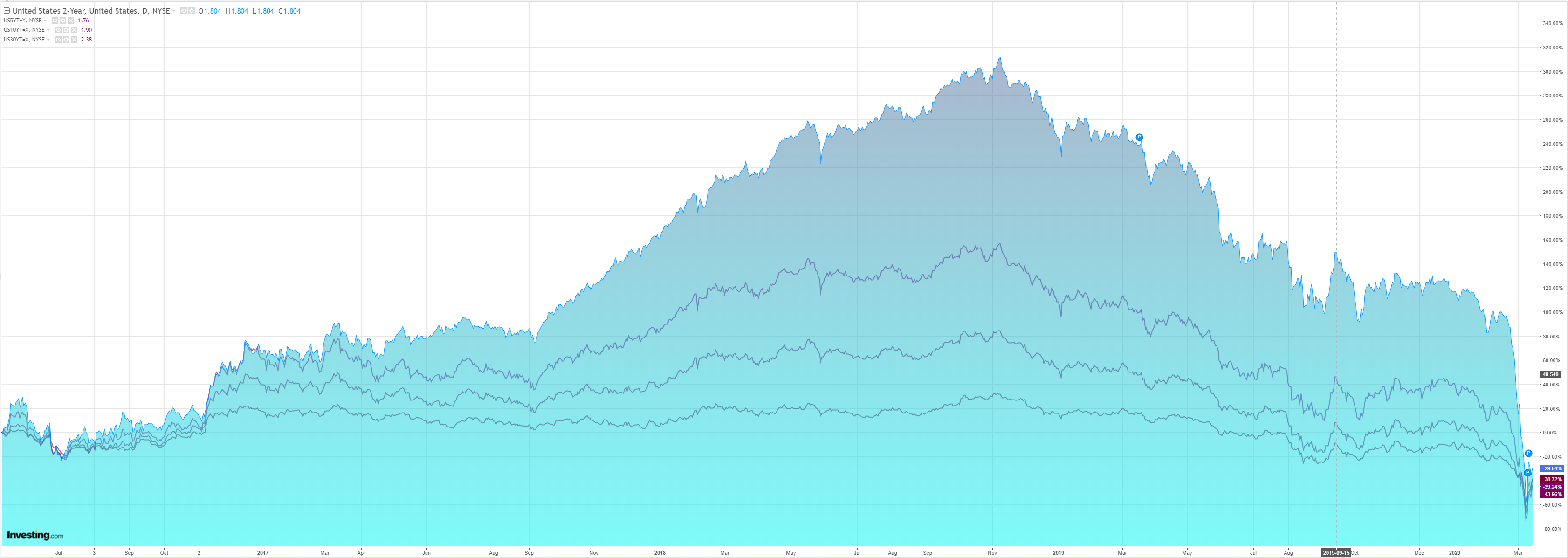

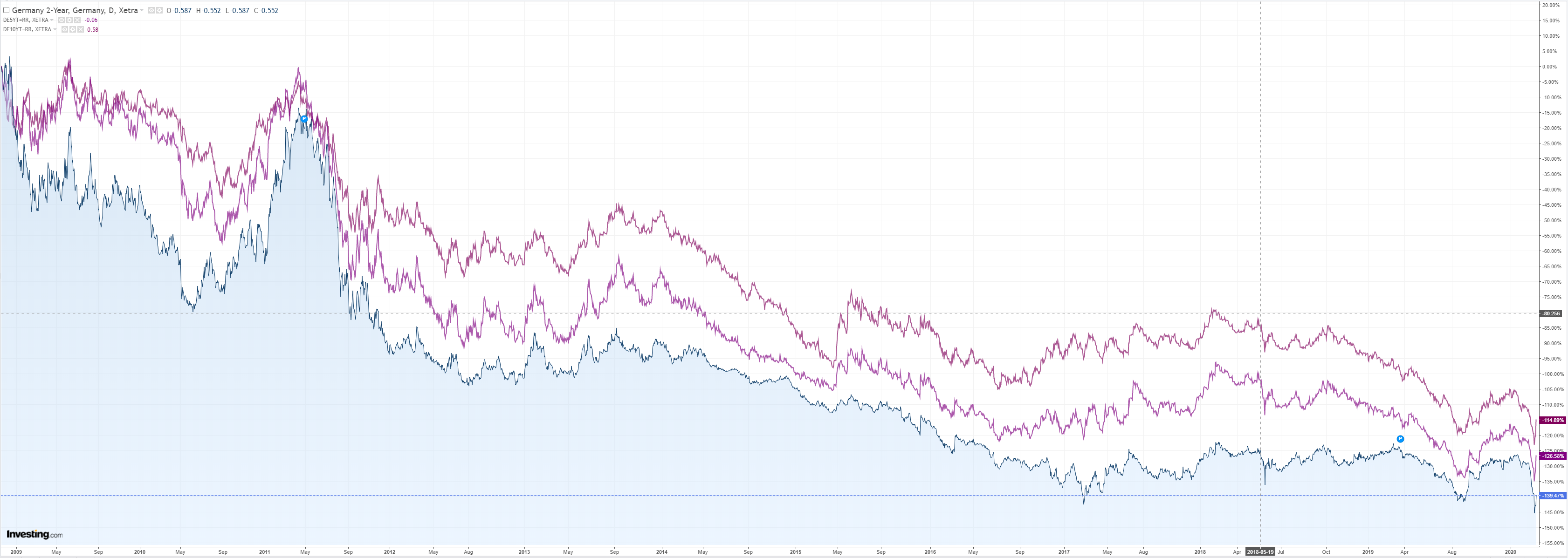

Soverign yields jack-knifed higher but the Fed hosed them off:

Stocks are as mad as a meat axe:

Let’s recall the analysis of Zoltan Poszer of Credit Suisse on the USD squeeze a little over a week ago:

Asymptomatic ≠ Not Contagious

Liquidity kills you quick…

…but the countries at the eye of a potential storm learned that lesson during the Asian financial crisis, and the banks that form the backbone of the global financial system learned that lesson during the GFC. Safety nets have been enhanced and expanded, with the Fed’s dollar swap lines with the ECB, the SNB, the BoE, the BoC and the BoJ being the most important. These regions are therefore well insured for funding stresses, and Japan has a lot of liquidity on deposit at the Fed before it would tap the swap lines.

We are more worried about other jurisdictions.

In the coming weeks, there will likely be dozens of research notes in which DSGE-types will show that most emerging market countries have multiples of their import bills in FX reserves, arguing that you should not worry about liquidity problems. That is precisely our point: most FX reserves are invested in the FX swap market or are in U.S. Treasuries and MBS, not on deposit at the foreign RRP facility, and when foreign central banks begin to monetize their FX reserves, GC repo rates and the €/$ and $/¥ currency bases will feel it.

Central banks are lenders of last resort, not lenders of first resort and the time it takes for them to go from one mode to another can take a long time and it can take a short time.

In August 2007 it took a long time – subprime was “contained”.

In September 2019 it took a day – with a 15 minute delay.

That said, the Fed’s response time last September was sped up by the fact that the markets exhibiting stresses were the o/n repo and federal funds markets, which are the core of U.S. money markets. The stresses we are imagining here would first strike: (1) peripheral cross-currency bases (e.g., KRW/USD) as missed payments grow; (2) €/S and $/¥ bases as reserve managers stop lending in the FX swap market, to help banks and banking systems deal with dollar outflows in their jurisdictions; (3) U.S. dollar Libor-OIS spreads as banks start fixing their LCRs that are being damaged by outflows of operating deposits and corporate credit lines; and lastly, (4) o/n GC repo markets as FX reserve managers and large banks are scrambling to turn collateral into cash to fund banks’ and corporate customers’ liquidity needs.

Stresses would strike in that specific order, which means that peripheral funding markets would show signs of stress first and core funding markets would show signs of stress last.

That risks a slow balance sheet response from the Fed…

If the outbreak worsens, funding market pressures can easily escalate. Rate cuts will help, but rate cuts, if they re-steepen the curve materially, can exacerbate funding pressures.

Our recommendation for the Fed would be to combine rate cuts with open liquidity lines that include a pledge to use the swap lines, an uncapped repo facility and QE if necessary.

It is very necessary now as the world fights for US dollars to liquify their finanical systems. The pressure is so great that DXY might rise for months ahead, even thoughthe Fed is able to contain yields and the curve steepening.

After all, the last point doesn’t prevent any kind of growth accident. Nothing can stop that now as the world’s two largest economies – EZ and US – go into shutdowns. Nor will it prevent immense defaults and losses.

But QE will underpin the global credit system so that it can absorb those losses in some kind of orderly fashion and, as that transpires, the world will continue to demand US dollars to keep their systems liquid, driving up DXY.

This is the moment. The end of cycle dynamics often referred to at MB since the GFC, when the dollar monetary system can send the AUD to undreamt depths, along with other currencies like gold.

In my view, risk assets are nowhere near the bottom, including the AUD, which may rupture our long held 50 cents target before this over.