This site has gone to great lengths to expose the critical flaws in Australia’s system of compulsory superannuation and to explain why superannuation is not a genuine retirement pillar.

These problems can be broken down into five key areas.

First, superannuation is voluntary for those that are self-employed, casually employed, or homemakers. Therefore, it misses at least 2 million people, meaning it is not a genuine retirement pillar.

Second, superannuation can be spent many years before the official retirement age of 66 (rising to 67). Indeed, at age 60, superannuants can remove all their superannuation balance and spend it on consumption goods immediately. Therefore, how can anybody genuinely call superannuation a retirement pillar when it legally allows one to withdraw all of their savings tax-free, and spend it as they see fit?

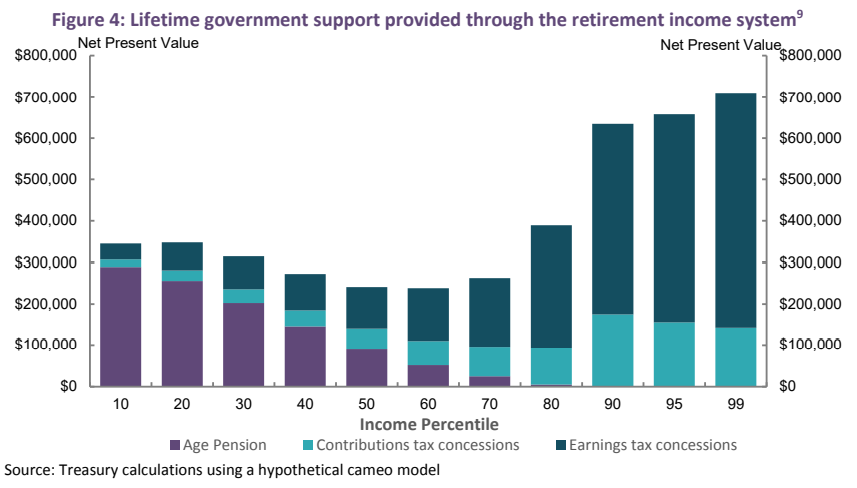

Third, the bulk of superannuation concessions go to where they are not needed (i.e. high income earners), costing the federal budget far more than it saves in Aged Pension costs. How much superannuation is accumulated also depends on both how long and how much one earns.

This absurd situation can be shown most clearly in the below Australian Treasury chart, which shows that the top 1% of income earners will receive over $700,000 in taxpayer contributions to their personal superannuation accounts over their working lives, which far exceeds the $50,000 received by the bottom 10% of income earners.

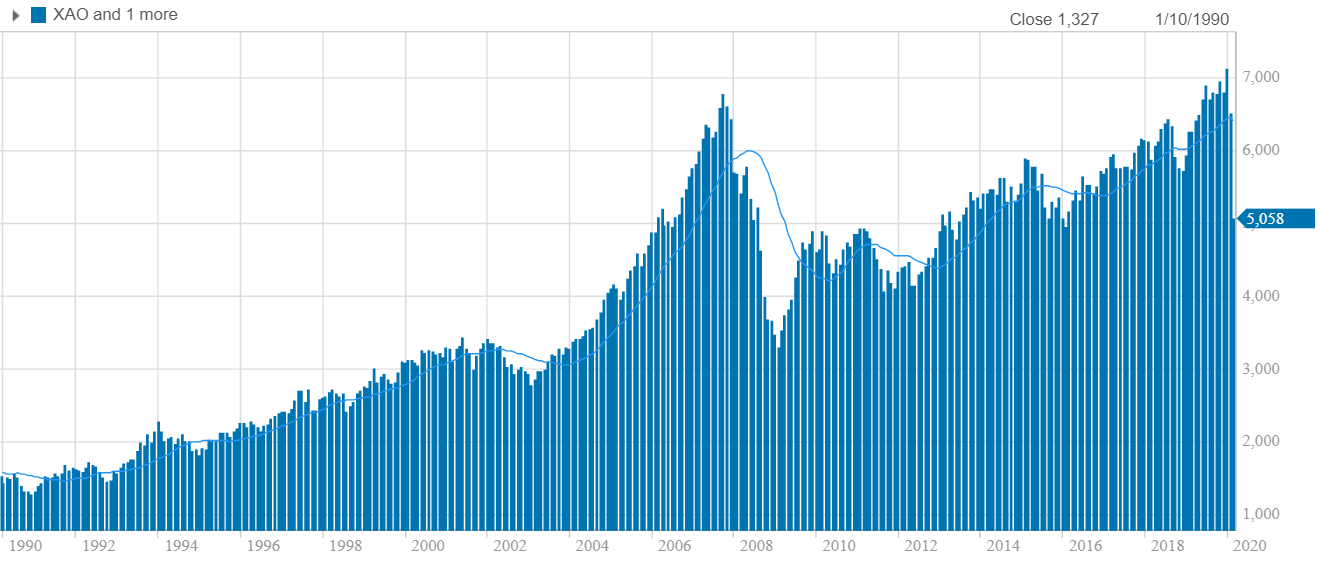

Finally, and perhaps most importantly given the current investment climate, people’s superannuation nest eggs are exposed to market risks, meaning that member balances can be wiped-out by adverse market movements as we are experiencing currently and experience during the Global Financial Crisis (GFC).

As shown in the next chart, which tracks the All Ordinaries Index (i.e. the biggest 500 companies on the Australian Stock Exchange), the Australian share market lost around 55% of its value during the GFC and has lost around 30% of its value currently:

Thus, for superannuation holders invested heavily in Australian shares (the majority), they saw a large proportion of their superannuation nest egg value wiped out.

The Aged Pension, by contrast, suffers from none of the above pitfalls. It is available to everybody that is not already wealthy once they reach retirement age. Because it is means tested, it is targeted towards those that need it most. It is not based on how much one works or earns before retirement. And it is not subject to market risk.

The Aged Pension, therefore, represents Australia’s true retirement pillar. And given these facts, sound policy dictates that taxpayer resources move away from supporting superannuation towards boosting the Aged Pension.