Some of Australia’s superannuation funds are facing a liquidity crunch due to holding illiquid unlisted assets at the same time as the Morrison Government is permitting members to make early redemptions:

Jeremy Cooper, Chairman of Retirement Income at Challenger Limited and formerly the Chair of the government’s Super System Review in 2010… warns that there could be a larger exposure to claims than the 15% of the full-time workforce (1.35 million people) the government is expecting to claim. He is concerned that funds have uncapped exposures, only limited by the $20,000 per member withdrawal.

…funds face challenges not just due to the balances of their members, but due to the asset allocation of their default investment options. One popular Industry Fund holds no cash or fixed interest in their flagship default option according to their website. The option is 33% invested in Private Equity, Infrastructure, and Property, which cannot be easily liquidated.

“Super funds currently don’t have formal access to emergency liquidity from the RBA. Access by super funds to the RBA ‘discount window’ would require an amendment to the SIS legislation prohibiting funds from borrowing and other administrative steps”, Cooper said…

[Graham Hand, founder of Cuffelinks] also noted the potential issues caused by the mismatch in liquidity. He referenced a conversation with the CIO of a large industry super fund who said, “we are going to get smashed.”

Labor’s shadow assistant treasurer, Stephen Jones, has demanded the Reserve Bank of Australia (RBA) step in to provide superannuation funds with liquidity support:

“We have genuine liquidity concerns, particularly if this takes off or the pattern of claims is not consistent with the way the government has modelled the numbers,” Mr Jones told The Australian Financial Review.

“The government may well have to step in, given they have created this mess, there will be a big expectation that they have to step in and secure liquidity for any fund that finds itself in trouble.”

Advertisement

Meanwhile, the Grattan Institute has thrown its support behind giving Australians early access to their superannuation:

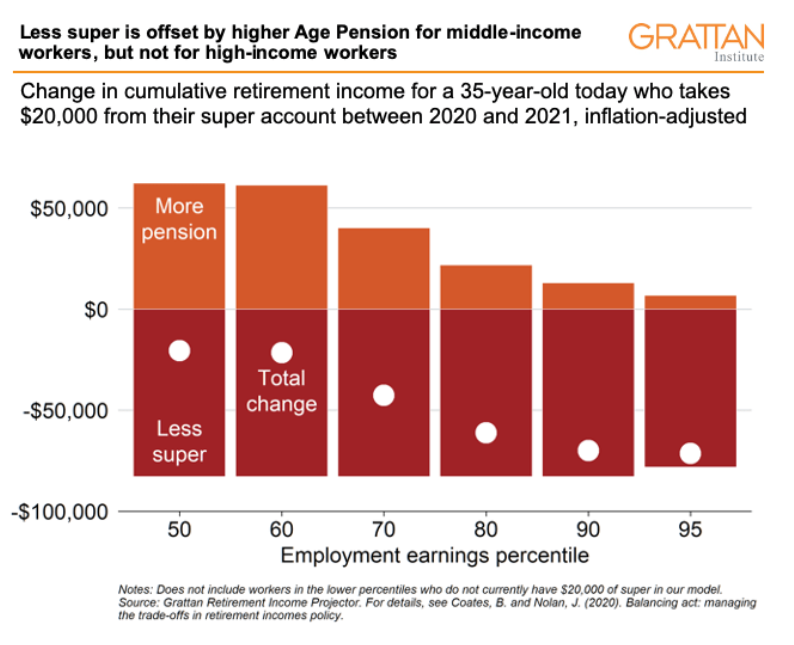

Our modelling suggests that a 35-year-old earning the median wage of about $60,000 who takes the full $20,000 allowed from their super can expect their super income through retirement to fall by around $80,000 in today’s dollars. But their total retirement income would fall by only $20,000 in today’s dollars, or around $800 each year.2 The Age Pension is means tested – the higher your super balance, the less pension you get. So workers who take money from their super will lower their super balance at retirement, but they will receive more Age Pension – helping to soften the blow…

Diverting superannuation money from retirement into Australians’ wallets today is not without cost. But it will put money into the hands of people when they most need it. And they need it now.

One small positive to come from the coronavirus is that it will likely kill calls to raise the superannuation guarantee to 12%. There is simply no way that the federal government will begin slashing take-home pay by 2.5%, just as Australia emerges from its biggest recession in the modern era.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.