The Australia Institute (TAI) released startling research on the growing cost of Australia’s compulsory superannuation system, which is costing the federal budget much more than it saves in Aged Pension costs:

Superannuation tax concessions are almost as big as the cost of the age pension. They’re also growing at twice the rate of the age pension. While the age pension is means tested to make sure that most of the benefit goes to those who need help with their retirement incomes, most of the superannuation tax concessions go to those that need the least help with their retirement incomes.

Superannuation tax concessions were supposed to help Australians become less reliant on the age pension, but with the rapid increase in the concession they will soon to be more expensive than the age pension. The cure has becoming worse than the disease…

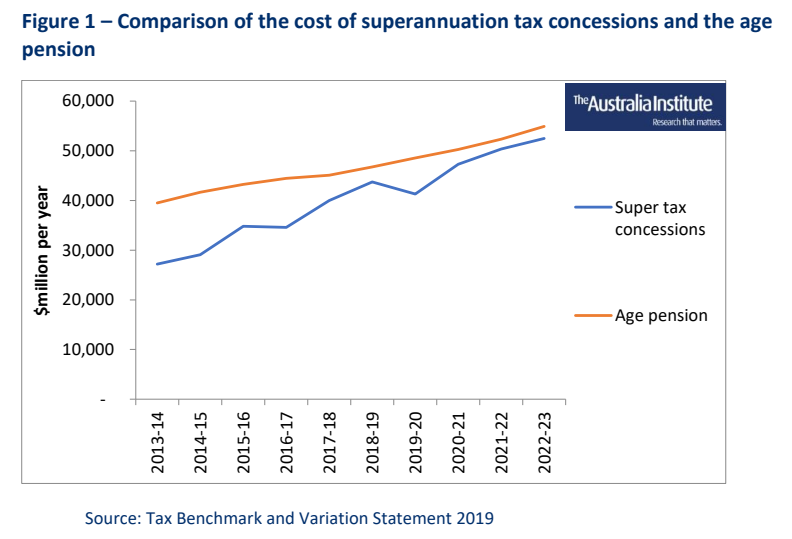

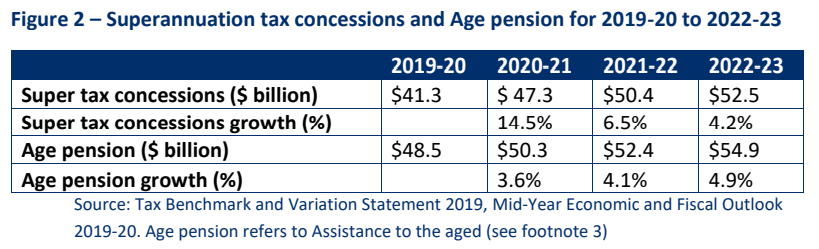

Superannuation tax concessions are set to rival the age pension in costs within a few years. According to Treasury’s release in February of the Tax Benchmark and Variations Statement 2019, superannuation tax concessions are expected to be $41.3 billion in 2019-20 and grow over the next three years to $52.5 billion in 2022-23. This compares to commonwealth funding for assistance to the aged, which is made up almost entirely by the age pension, which will be $48.5 billion in 2019-20 rising to $54.9 billion in 2022-23…

Superannuation tax concessions are not just large but are growing rapidly. Over the next three years they’re expected to grow by 25.2%. This is twice the growth rate of the age pension which is expected to grow by 12.6% over the next three years… If we look at the average annual growth rate of the age pension over the nine years from 2014-15 to 2022-23, it has grown at 3.7% per year. Superannuation tax concessions have grown at more than twice that rate over the same period at 7.8% per year…

Compulsory superannuation and the concessional way Australia taxes it was introduced in part to take pressure off the budget. This represents a failure of policy because superannuation tax concessions which were designed to reduce the budget cost of the age pension have themselves grown rapidly and are likely to soon cost the budget more than the age pension…

There is also the issue of equity. While the age pension is means tested and mainly helps low income households, superannuation tax concessions mainly go to high income households. 60 per cent of superannuation tax concessions go to the top 20 per cent of households with just 11 per cent going to half of all Australian households…

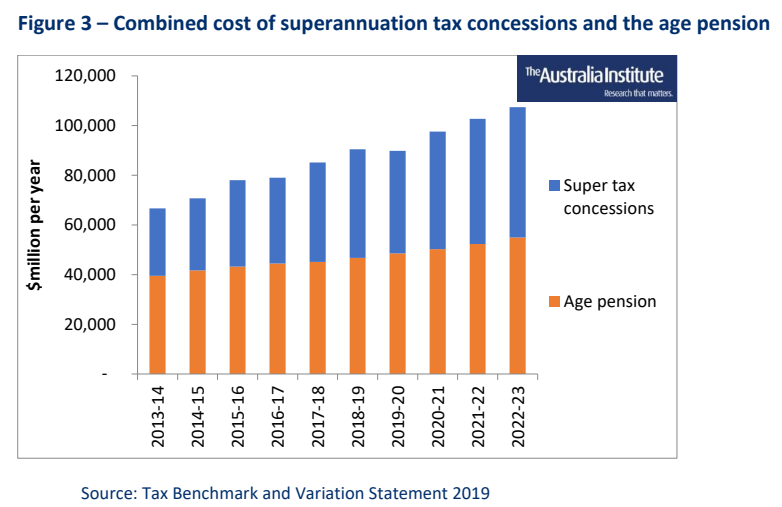

Superannuation tax concessions and the age pension represent the main way the government funds retirement incomes. The two combined are worth $90 billion in 2019-20 rising to $107 billion in 2022-23. This is shown in Figure 3…

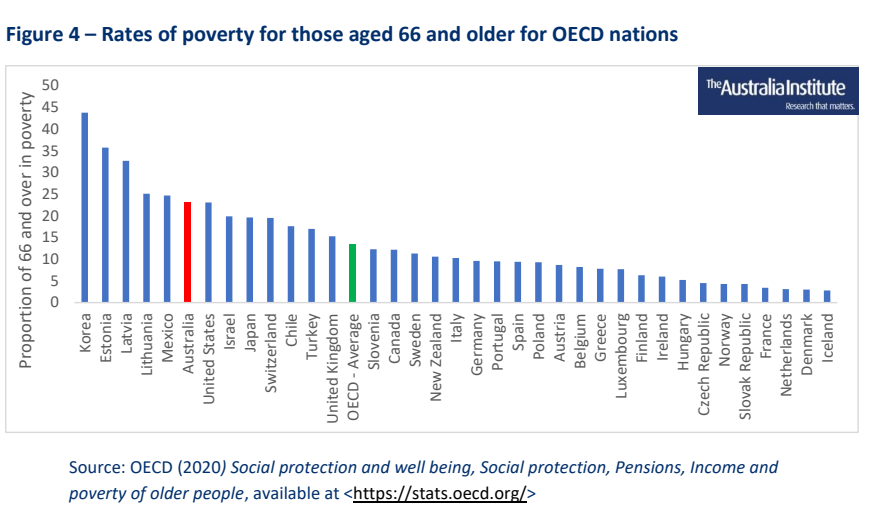

Despite the large amount of money Australia still has very high rates of poverty in retirement. Of the 36 developed countries (OECD nations) Australia has the sixth highest rate of poverty for retirees. This is shown in Figure 4.

Such high rates of poverty in retirement is in part because so much of the funding for retirement incomes goes to high income households in the form of superannuation tax concessions. The rapid growth in these tax concessions will only make this worse.

TAI’s findings are backed by the Grattan Institute, which also found that superannuation concessions cost the federal budget far more than it saves in aged pension costs:

Advertisement

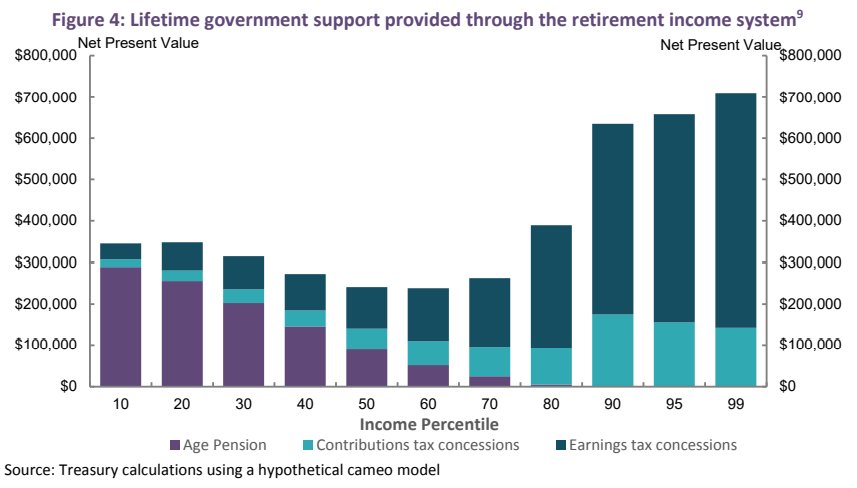

Part of this is because superannuation concessions are skewed so heavily towards high income earners, as shown spectacularly by the below chart from the Australian Treasury:

Given the above evidence, the federal government would be economically negligent to proceed with the legislated increase in the superannuation guarantee to 12%. All this would do is increase inequality, blow an even bigger hole in the federal budget, and rob ordinary workers of much-needed disposable income at a time of zero real income growth.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.