In a speech delivered today, RBNZ Governor Adrian Orr has ruled out using unconventional monetary policy for the time being, but is open to the idea in the future should conditions warrant it:

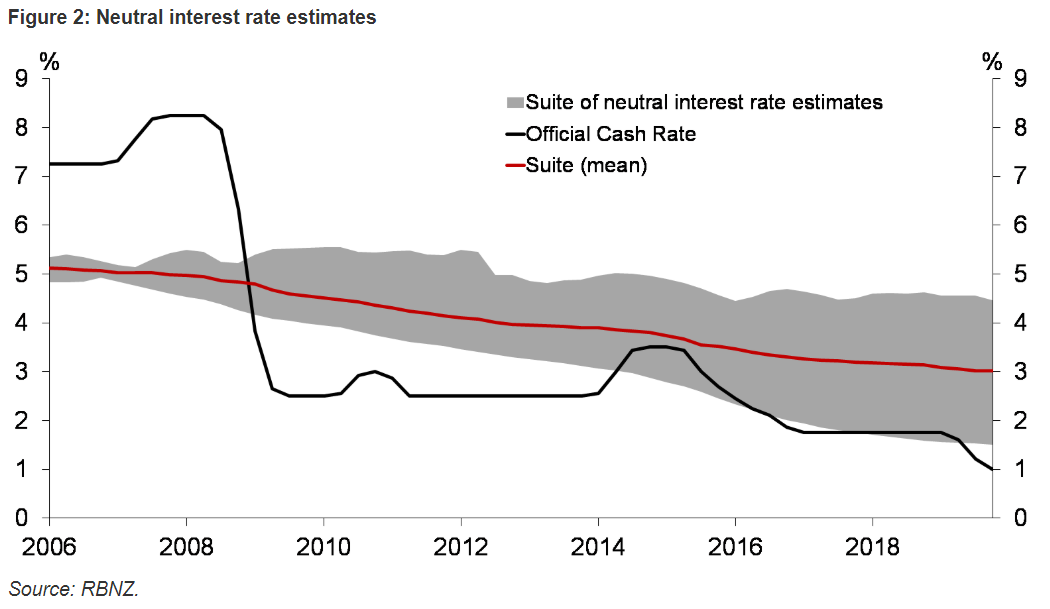

Largely since post the ‘Great Financial Crisis (GFC)’ of 2008, global inflation and interest rates have been remarkably low. New Zealand’s neutral interest rate (i.e., the rate that, on average over time, would be consistent with no over- or under-utilisation of resources and stable inflation) has declined considerably (Figure 2), and we have had downward pressure on domestic inflation.

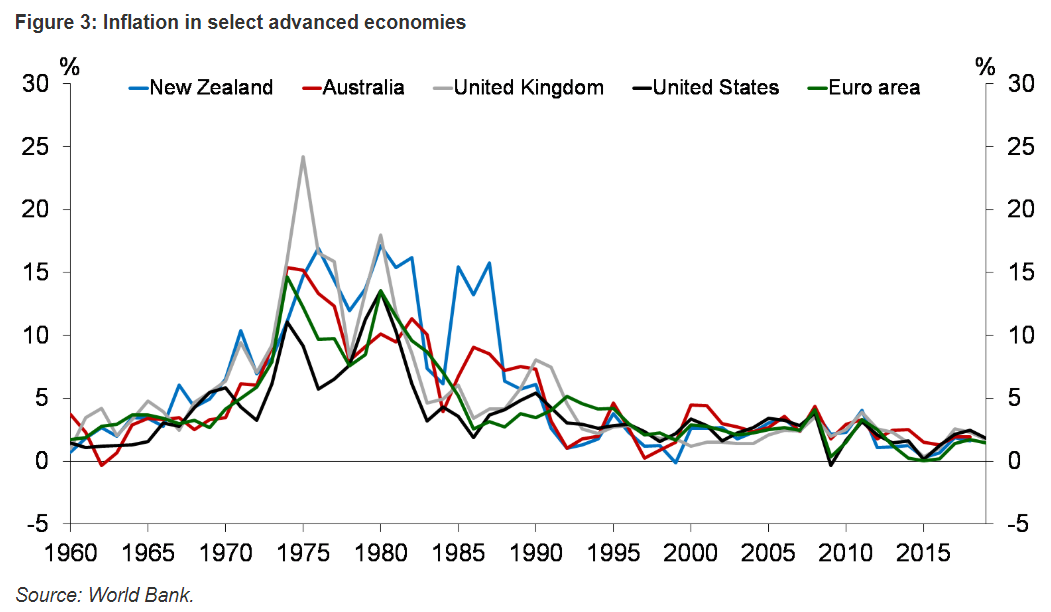

Global inflation has been declining for a variety of reasons over recent decades…

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.