The embattled Peter Switzer had a crack at those that saw it coming on Saturday:

Some irresponsible media players have already pulled out the D-word for clickbait reasons. I hope one day I can bring them to book for over-scaring Australians, when it was the last thing people locked out of jobs, needed to see, read or hear.

And let me make this clear: while a depression is possible, the magnitude of the response from governments, central banks and even banks makes it very possible that this shocking smashing of economies could be short term.

The US Federal Reserve Chairman, Jerome Powell on Thursday suggested that an eventual rebound of the stock market and the US economy could be “vigorous”.

In fact, it already has been – shocking me and my hairline! I’ve seen some stock market gyrations in my lifetime, but this takes the cake!

The most watched stock market index — the Dow Jones Industrial Average — dropped 37% at its worst, as the Coronavirus wreaked havoc on a complacent and pandemic-ignorant share market fraternity. Unfortunately being in that group I have to admit that I was, however, pondering how the market was ignoring it.

My headlines on www.switzer.com.au or Switzer Daily show it:

January 29 — “How do the Yanks gamble against the Coronavirus?”

January 31 — “Could the Coronavirus be a killer black swan?”

February 3 – “Will we dodge a coronavirus and bushfire recession bullet?”

February 4 – “Will the Reserve Bank use the Coronavirus to justify a rate cut today?”

February 11 – “The Coronavirus could seriously hit JB Hi-Fi, Harvey Norman and more.”

February 14 – “Could the Coronavirus cause a mega-market meltdown?”

February 19 – “Well, der, America, the Coronavirus IS a big deal.”

The Dow hit its top on 12 February, but it didn’t go into panic mode until 21 February. And it was a disaster until 23 March, when the Trump team and the Democrats stumped up a US$2 trillion stimulus package. Of course, other governments pulled out their budgetary bazookas with our own Josh Frydenberg finding $17.6 billion and then $66 billion in stimuli packages.

This global government rescue plan was aided and abetted by the Fed and other central banks, and our own Reserve Bank has pumped $90 billion into our banks for small business loans. And the Government found another $15 billion for smaller banks and non-bank lenders to keep the economy going.

The biggest bazooka of all per country came out of Germany where the stimulus package there was, wait for it, 30% of GDP!

This reaction shows that governments and economists have learnt from the Great Depression. The biggest lesson of that prolonged economic quagmire of the 1930s, which lasted for nearly a decade, was that when you get a massive shock to the financial and economic system, you have to throw money at the problem.

The former Fed boss, Ben Bernanke, who navigated the US out of the GFC and who was regarded as a world academic expert on the Great Depression, made the idea of “helicopter money” popular as a solution to a huge economic collapse. Metaphorically sprinkling money out of a chopper to people is seen as a lesson economists have learnt looking at what has worked and failed in previous recessions and depressions.

This week when Bernanke was interviewed on CNBC this was his take on the current economic and stock market drama.

“It is possible there’s going to be a very sharp, short, I hope short, recession in the next quarter because everything is shutting down of course,” he said. And roughly 3.3 million Americans, who lost their jobs in a week, suggest he’s absolutely right.

However, Ben said more.

“If there’s not too much damage done to the workforce, to the businesses during the shutdown period, however long that may be, then we could see a fairly quick rebound.”

“This is a very different animal from the Great Depression” he said. “[It] came from human problems, monetary and financial shocks. This has some of the same feel, some of the feel of panic, some of the feel of volatility that you’re talking about [but this one]… it’s much closer to a major snowstorm or a natural disaster, than a classic 1930′s-style depression.”

So an expert on the Great Depression is putting an upcoming Great Depression on a lower order expectation, while a bunch of ill-qualified, media-chasing headline click-baiters are happy to scare people to near economic death!

Ben could be wrong but if the infection and death rates come off their rising trends in Europe and the USA faster than current predictions, then my money will be on Ben’s economic prognostications rather than another Great Depression.

I’d love the doomsday merchants to be wrong because they seem to be backslapping themselves and their forecasting, forgetting the human tragedy that is driving down asset prices, closing businesses, killing jobs, crushing businesses and consumer confidence, in delivering what they’ve been wrongfully predicting for years.

If these current events had occurred because of economic mistakes or developments, then they’d rightfully be proud of their negative and accurate analysis — but they’ve been helped by a black swan Coronavirus.

They might have got it right but for the wrong reasons. So I hope the best efforts by the governments and citizens of the world can trump this tragedy.

If we fail to beat the virus, a depression is a real possibility, even with the stimulus packages. But from where I’m currently observing, with my less than 2020 virus-affected vision, I’m betting against another Great Depression.

Go the world!

MB is a big fan of Ben Bernanke’s actions to get liquidity into markets after the GFC struck. But given the Chairsatan also expressed in 2003 the Fed had “tamed” the economic cycle, and then in 2007 that the subprime mortgage crisis was “likely to be contained”, we long ago concluded that using him as a forecasting expert is not going to win too many arguments.

Also, just before the above Mr Switzer holds anyone to account for using the word “depression”, here’s hoping that he holds someone else to account. Those in the media who have been actively underplaying the dangers of the virus. Check out this other guy who is also called Peter Switzer:

My media mates are bullshitting the Coronavirus and it’s a disgrace. I really don’t want to write this, but my sense of social obligation and my fear that the infodemic about the alleged pandemic means I have to criticize my mates in the media. But I guess as an experienced player in the space who was schooled by an old-fashioned regime, I have to scream that this Coronavirus bullshit has to stop!

…and being a numbers man, I ran my eye over the infection and death numbers in South Korea in yesterday’s column. I found the infection rate was a very low 0.06% — and of those, 0.01% ended up deceased.

…The pressure for media outlets to get eyeballs and ears means the media, at times, swaps intelligent analysis of current affairs issues for clickbait stupidity, which is not really a threat to life and limb but jobs, economic growth, profits, share prices and our super funds.

I really wish adults were in charge of media outlets who occasionally say “we’re better than that and we won’t run that shit!” By the way, that’s the way Heads of News actually speak when they’re making a point.

And that’s the problem — too many young journalists haven’t been given great leadership — and gee, isn’t it showing?

We have right-wing outlets pushing their agenda and left-wing outlets playing fast and loose with the truth. And it’s honesty, integrity and the brainpower of the media that is the casualty.

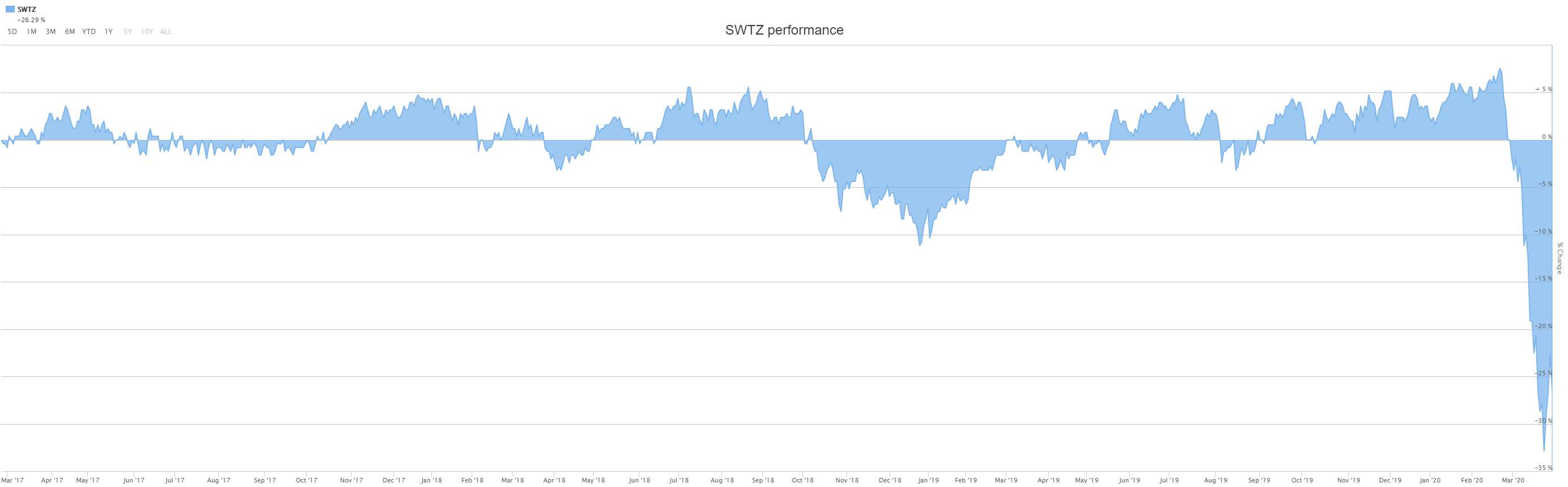

Hopefully no elderly folk acted on that argument and leaped into the public sphere. Otherwise they may have succumbed like Switzer’s flagship Growth ETF:

Down 31.5% from the recent peak. From inception? Minus 26% over three years in raw numbers. Including dividends? From inception, SWTZ down 18% versus the ASX200 down 4%.

Of course, past performance is not an indicator of future returns and you can’t put a price on a reassuring word from the magician.

Even from your ICU bed.