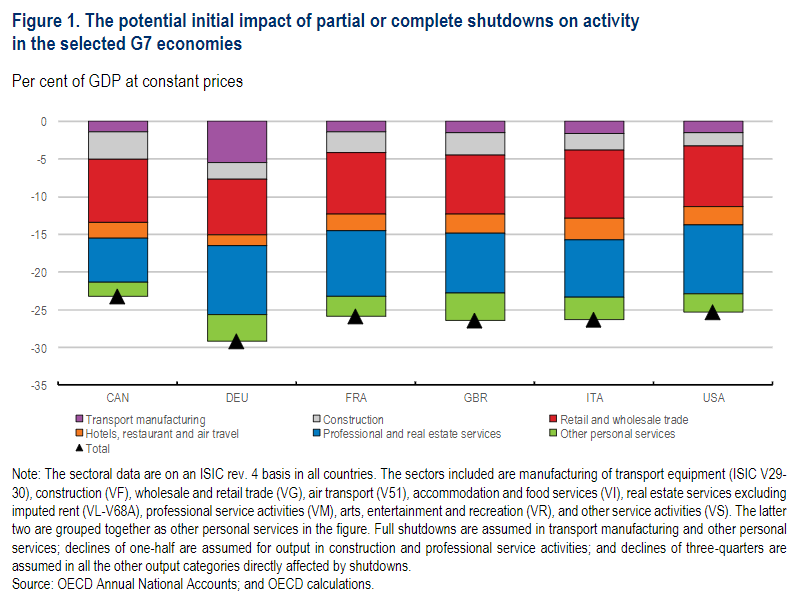

The increasing spread of the coronavirus across countries has prompted many governments to introduce unprecedented measures to contain the epidemic. These are priority measures that are imposed by a sanitary situation, which leave little room for other options as health should remain the primary concern. These measures have led to many businesses being shut down temporarily, widespread restrictions on travel and mobility, financial market turmoil, an erosion of confidence and heighted uncertainty.

In a rapidly changing environment, it is extremely difficult to quantify the exact magnitude of the impact of these measures on GDP growth, but is clear that they imply sharp contractions in the level of output, household spending, corporate investment and international trade. This note provides illustrative estimates of the initial direct impact of shutdowns, based on an analysis of sectoral output and consumption patternsacross countriesand an assumption of common effects within each sector and spending category in all countries.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.