Ian Henschke, chief advocate for National Seniors Australia, has demanded the Morrison Government show some leadership and cut the deeming rate to those on part pensions:

“If they cut the deeming rate, it would be giving money to people who need it and it would go straight into the economy and give people faith that the government was acting in their interests,” [Henschke] said…

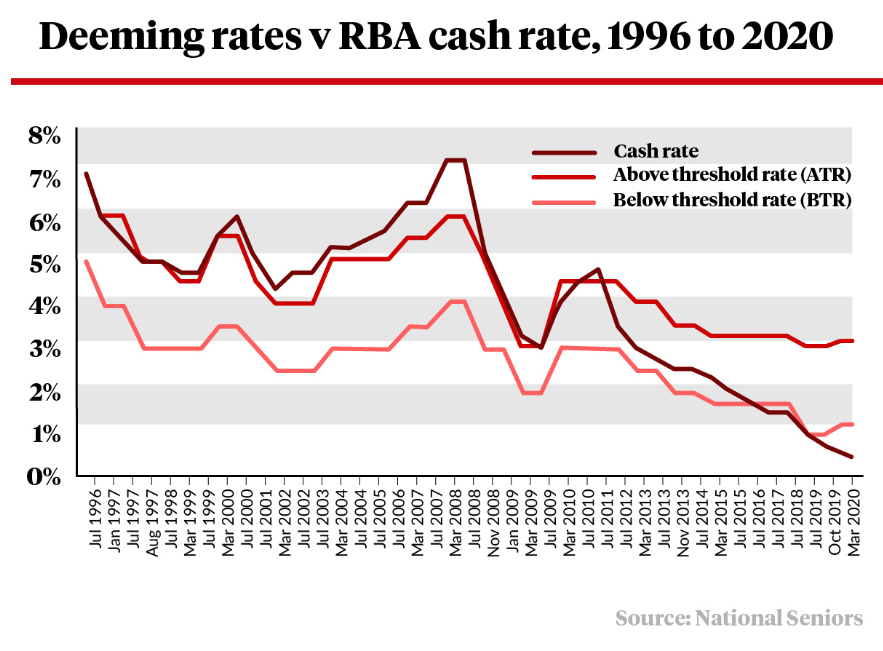

Deeming works like this. For single pensioners who have savings of up to $51,799, or couples with up to $86,200, the government assumes (“deems”) interest earned on their accounts comes in at the rate of 1 per cent for the purposes of the age [or other] pension income tests.

On savings above those amounts, the deeming rate is 3 per cent.

So if you earn less than the government assumes on your savings, you receive less pension than you really should.

The loss in pension income is the difference between the deemed rate of return and what the bank actually pays in interest…

Mr Henschke has called on the government to act.

He wants it to “halve the upper deeming rate to 1.5 per cent and the lower rate to 0.25 per cent, or better still, go back to coupling deeming rates to follow the cash rate”…

Once again, the argument that the deeming rate is unfair does not pass scrutiny. Deeming rates apply to all financial assets, including equities like shares and unit trusts. And equities typically rise as the cash rate falls – a point conveniently ignored by Ian Henschke.

Deeming rates have to provide a simple benchmark that takes account of cash returns, dividends and other equity returns. That’s why there are two deeming rates – a lower one biased to cash (1.00% on the first $51,800 of investment assets for a single), and a higher one biased to equities (3.00% on investment assets over the amount of $51,800 for a single).

Advertisement

If anything, the upper deeming rate is far too generous, since actual earnings on equities (dividends) are typically much higher than 3%.

My argument was explicitly supported by Council on the Ageing Australia CEO, Ian Yates, who recently noted that most pensioners earn significantly more than the deeming rate on their investment earnings:

“Those calling for the full cut in the cash rate to be applied to deeming need to be honest about how many pensioners are affected, and about the fact that if the Government replaced the deeming rate with actual earnings the majority of part pensioners would be worse off”.

Advertisement

Moreover, if economic stimulus is the goal, then the government should instead lift Newstart, which has not risen in real terms since the early-1990s and has fallen 30% below the poverty line.

The unemployed are among Australia’s poorest and every extra dollar they receive in government support would be spent rather than saved.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.