Money market meltdown intensifies

Cross-posted from Zero Hedge on some seriously fucked global financial plumbing.

As Bank of America’s rates expert, Mark Cabana – formerly of the NY Fed – writes on Saturday, “the Fed has been on fire” lately, which in light of the Fed’s activities in the past two trading days of the week, may be an understatement: the Fed announced a $5 trillion (assuming max allotment) expansion to its monthly repo operations and executed purchases on Friday of $37BN out of their $80BN/month in UST firepower across the curve. As we explained at the time, the Fed needed to do this to unfreeze an increasingly broken Treasury market and to facilitate a relatively orderly unwind of highly leveraged UST positions that have likely reached loss risk limits with recent market volatility, which sparked an unprecedented VaR shock (as Cabana note, “the dealer community could not facilitate the unwind of such trades since their balance sheets were full of duration + limited ability to expand them under current regulations).

And yet, despite the unprecedented large Fed UST purchases the Fed isn’t done, because as Cabana points out, not all highly leveraged UST trades have been unwound which is reflected by the fact that:

- 30Y USTs vs OIS have only richened marginally over recent days

- 30Y swap spreads have only widened back to levels last seen prior to the Fed’s shift in UST purchase strategy yesterday

- implied funding costs on long-dated futures contracts has not materially eased.

And hinting that more is to come, the Fed said that “the composition of the remaining purchases will be announced on Monday, March 16, 2020, around 9:00 AM.”

However, with FRA/OIS exploding despite all the Fed’s emergency interventions, and even JPM now admitting the world is facing a $12 trillion dollar margin call…

… the Fed will have to do more before funding markets finally stabilize.

The problem is what does the Fed do. On one hand, as per the recommendation of Credit Suisse repo expert, Zoltan Pozsar, the Fed should “open liquidity lines that include a pledge to use the swap lines, an uncapped repo facility and QE if necessary.” With the Fed already restarting QE, that just means a full blast of unlimited swap lines re-opened with the world’s central banks coupled with a standing repo facility to bailout any and all financial intermediaries who are still caught on the wrong side of the Treasury basis trade that has crushed so many last week.

However, if the Fed does pursue this “kitchen sink” approach, and if it fails to boost confidence (especially if the market deems the fiscal response by Congress as insufficient), Powell would be out of ammo, his last bullet being to buy stocks (and oil) in the open market, a precursor to full-blown systemic collapse.

That said, there is one intermediate step the Fed can do.

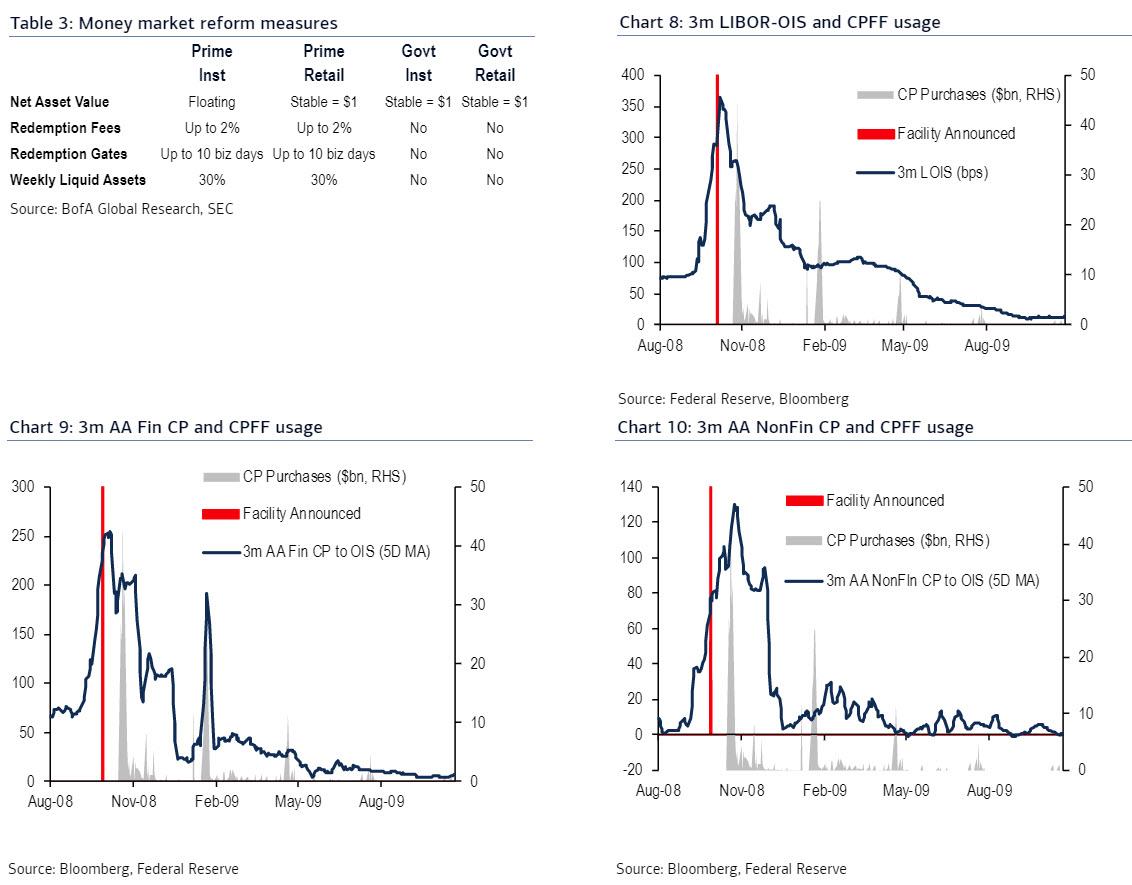

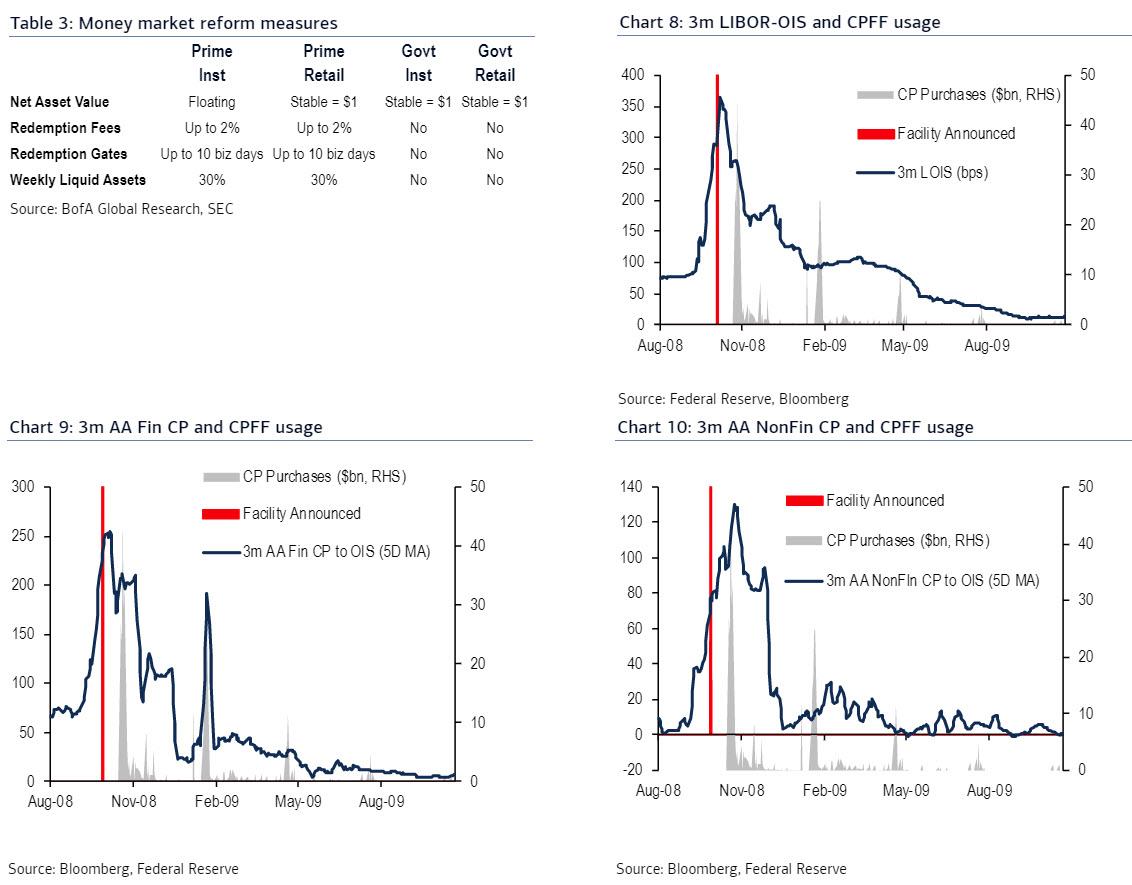

According to BofA’s Cabana, the Federal Reserve may announce measures on Sunday night aimed at bolstering liquidity in the commercial paper market, used by companies for short-term loans, or as Cabana puts it “the commercial paper market will likely be the Fed’s next target to unfreeze.” The last time the Fed issued such an was in 2008 when the Fed bought commercial paper from issuers directly, when it also rolled out a Commercial Paper Dealer Purchase Facility in which the Fed would buy commercial paper from dealers directly.

To justify his point, the BofA rates strategist looks at the explosion in CP rates and 3m LIBOR-OIS spreads to levels last seen in the financial crisis, similar to what is going on in FRA/OIS.

As he further explains, during the last crisis, the CP market froze due to similar dealer balance sheet constraints as the UST market but with a different genesis. Dealer CP balance sheets are clogged because of elevated macro risks caused

- increased or anticipated corporate CP issuance to secure cash

- MMF to sell CP as a means to raise cash in anticipation of large institutional outflows.

Why CP? Corporations rely on the CP market as a reliable source of short-term cash for unanticipated funding needs. COVID-19 has provided a sharp downward shock to revenues and many issuers either sought to increase financing or the market anticipated the need for this. The expected CP supply shock + growing credit concerns then pushed spreads wider and reduced overall investor demand. This then made it harder for non-financial corporates to issue and for dealers to move any new issuance off their balance sheet.

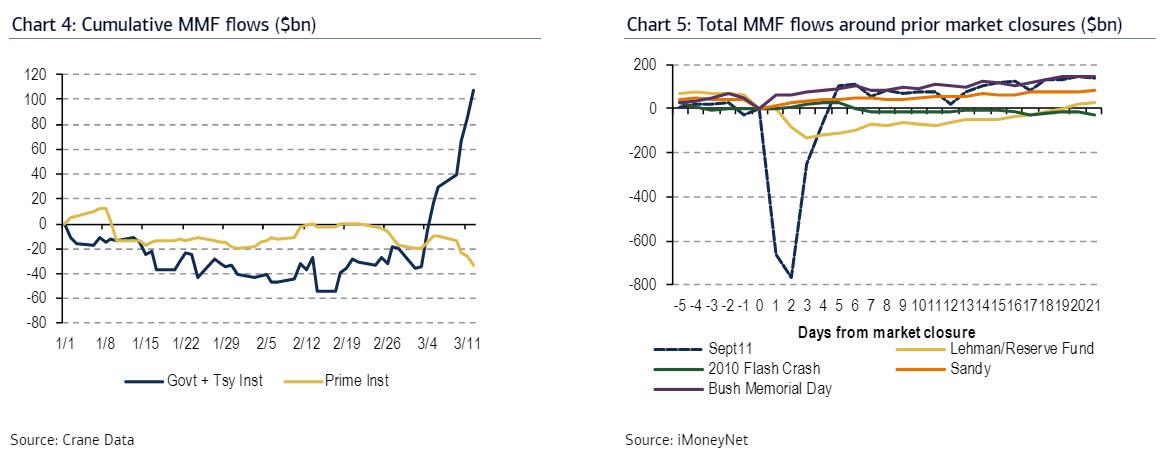

U.S. money market funds took in a record $87.6 billion in the week to Wednesday, data from Lipper showed.

Meanwhile, as Reuters notes, investors are demanding the highest premium since March 2009 to hold riskier commercial paper versus the safer equivalent. The spread between the overnight AA-rated paper of nonfinancial companies versus riskier overnight P2 paper rose to 73 basis points on Thursday, the most recent data available from the Federal Reserve.

Without access to the commercial paper market, companies could turn to banks to draw on their lines of credit, potentially putting even more stress on lenders. At the end of 2019, banks had roughly $1.4 trillion of unused corporate credit commitments according to a recent analysis by Credit Suisse.

Already last week we saw Boeing, Hilton Worldwide and SeaWorld Entertainment draw on or increased the size of their credit lines in recent days, perhaps in anticipation of just such a worst case outcome. All three companies are in sectors directly affected by reduced tourism and discretionary spending due to the coronavirus.

Which is where the Fed steps in: in short, the Fed would effectively backstop the most urgent and short-term form of corporate funds. one which many companies in the past have used to repurchase their own stock, and as such any such corporate bailout will spark a huge political debate as Americans – rightfully – demand to know why the Fed is now in the business of bailing out companies that spent like drunken sailors on buybacks, only to demand a rescue now that they have no cash left.

In any event, at the same time corporates have been seeking to tap CP markets to fund short-term funding gaps, money market mutual funds (MMF) have been trying to raise cash in the secondary CP market. MMF are raising cash to build liquidity buffers ahead of an expected increase in investor outflows. We have already started to see outflows from prime institutional funds and this may spill over into government MMF depending on the severity of quarantines around the county & concerns over access to cash. With a backdrop of extremely volatile markets, MMFs may be concerned that outflows will continue as we have seen around market closures in the past.

And so, in anticipation of outflows, prime MMFs have already started to increase their liquid assets and reduce CP holdings, but this will only become more difficult as dealers struggle to find buyers and move risk off their clogged balance sheets… unless the Fed steps in.

What the above means in English is that in a repeat of the Lehman crisis, the financial system could see a bank run, only not in conventional deposits, but rather in money market funds: as Cabana explains, “the clogged CP market poses risks to higher bank funding costs and could result in an MMF run akin to that in the aftermath of the Reserve Fund breaking the buck in ’08.” To be sure, U.S. money market funds took in a record $87.6 billion in the week to Wednesday, data from Lipper showed. It coulf get much worse, as the market turmoil could spur nervous investors to withdraw from money market funds en masse, creating a run like that seen in 2008 with the Reserve Primary Fund, a $65 billion fund which saw its net asset value “fall below $1 thus resulting in investors receiving an amount of cash lower than what they originally deposited.” More below:

… the clogged CP market also poses increased risks for a MMF run. The source of the MMF run would be fundamentally different than during ’08. Recall, in ’08 the Reserve Fund experienced losses on its CP holdings sufficient to cause its NAV to fall below $1 thus resulting in investors receiving an amount of cash lower than what they originally deposited (i.e. “breaking the buck”). These fears sparked a run on MMF and forced the Fed to intervene in CP markets and the MMF industry.

The source of the current potential MMF run is not around “breaking the buck” but is about investors not being able to access their MMF cash on demand. Concerns around “breaking the buck” have largely been solved through post crisis MMF reforms that allows for institutional prime funds with credit sensitivity to have a floating NAV that can fall below zero. However, all prime funds have a weekly liquid asset minimum of 30% NAV (Table 3). If “weekly liquid assets” falls below 30% of NAV the MMF board can impose a liquidity fee of up to 2% for all redemptions; if the liquid assets fell below 10% the prime fund would be required to impose a liquidity fee of 1%. To ensure that MMF are not required to impose a liquidity fee most MMF maintain liquidity well above the 30% threshold.

The current concern is that if the CP market is frozen, prime MMF could see their weekly liquid assets fall below 30% as they experience outflows. If weekly assets fall below 30% this would need to be reported to the SEC, would be in the public domain, and could result in a liquidity fee. Such a drop in liquidity would like result in a run on the MMF which experienced a drop in their liquidity and could result in a run on the prime MMF industry more broadly. This type of run would then result in more forced liquidations which would worsen CP liquidity, increase front-end credit spreads, and weigh on market sentiment. We strongly suspect the Fed wants to avoid this.

Which is Cabana “expects the Fed to act quickly to avoid both stressed outcomes.”

What, specifically, would the Fed announce?

To address the current frozen CP market BofA expects the Fed to announce two CP facilities, likely on Sunday night. These facilities include:

- a reintroduction of the 2008 “Commercial Paper Funding Facility” or CPFF

- a facility that would specifically target purchases of CP on dealer balance sheets which we will call a “Commercial Paper Dealer Purchase Facility” or CPDPF.

These are discussed in greater detail below:

- CPFF: the CPFF would likely be structured similarly to the facility in the financial crisis. In 2008 3m L-OIS widened to around 350bps amid mounting credit concerns. The Fed announced the CPFF to purchase CP directly from issuers and allow corporates to continue funding themselves despite market stress. After this facility was announced, L-OIS and Fin CP to OIS spreads started to tighten, though NonFin to OIS spreads continued to widen until the purchases were implemented.

CP was purchased at a discount rate of 3m OIS + 100bp plus either an additional 100bp surcharge or a collateral arrangement with the issuer. The Fed would provide 3m loans to a specially created LLC, which would use those funds to purchase CP directly from issuers. This LLC held the CP to maturity and used the proceeds to repay its loan from the Fed. US issuers of CP were eligible to use this facility and they were required to register with the CPFF. In short, Cabana expects that Fed will launch a CPFF similar to the ’08 facility. This CPFF would be targeted at to re-open CP issuance markets and to alleviate the potential bank funding strain from having numerous credit lines drawn over a short period of time.

- CPDPF: a proposed “Commercial Paper Dealer Purchase Facility” would essentially entail creating a special Fed vehicle aimed at purchasing CP directly off of primary dealer balance sheets, similar to the current UST purchases discussed above. The purchase program would likely need to be relatively small and short lived in its existence. The facility would only be used to clear existing inventory off dealer balance sheets and provide an outlet for additional prime MMF sales until they had built sufficient liquidity buffers. There is roughly $9.5bn of CP on dealer balance sheets according to primary dealer data as of March 4. We might imagine prime MMF might only need to sell $20-$40 bn more to build their liquidity buffers by another 5%. Therefore, according to BofA’s calculations, it is likely that the size of the Fed’s CP dealer facility might only need to total $30-$50 bn.

There is a potential hurdle in that both of these facilities – which would seek to explicitly bail out corporations in need of funding and MMFs – likely cannot be unilaterally authorized by the Fed due to law changes since the financial crisis. The existence of these facilities would only occur through the authority of section 13-3 of the Federal Reserve Act. The Federal Reserve used the “unusual and exigent circumstances” clause (i.e. “section 13(3)”) of the Federal Reserve Act to extend credit to financial firms during the Global Financial Crisis in 2008. Using this broad authority, the Fed created and implemented five funding facilities to provide liquidity to primary dealers and act as a backstop to the commercial paper and asset-back securities markets. BofA explains further:

Congressional action has reined in some of the Fed’s emergency lending powers. The new guidelines do not eliminate the Fed’s lending authority but raise the procedural bar. The new law still allows the Fed act as the “lender of last resort” and create broad funding facilities to help market functioning. However, there are more hoops to jump. The Fed is also restricted from providing “tailored” help to individual firms.

To recap, the Dodd Frank Act of 2010 changed the Fed’s 13(3) authority and requires programs established under this authority to have:

- Approval from the US Treasury Secretary

- “Broad based eligibility” is meant to include a program or facility that is not designed for the purpose of aiding any number of failing firms and in which at least five entities would be eligible to participate. It also suggests programs should not be for the purpose of aiding specific companies to avoid bankruptcy or resolution.

- Limited risk of insolvency: the definition of insolvency to cover borrowers who fail to pay undisputed debts as they become due during the 90 days prior to borrowing or who are determined by the Board or lending Reserve Bank to be insolvent.

All three conditions would easily be met in the current market panic.

Which brings us to the question of “when” will the Fed announce these facilities? Here, as above, BofA repeats that “time is of the essence on these facilities and expect the Fed will announce them this coming Sunday night.”

We believe it imperative the Fed roll out these facilities on Sunday night given the looming expected prime MMF outflows and necessity of their ability to sell CP in order to raise cash. If the Fed waits too long the MMF outflow pressure could mount and the risk of a large scale MMF run could increase.

Finally, how will the market respond if the Fed acts? Here is BofA’s conclusion:

We expect that 3m LIBOR-OIS and FRA-OIS spreads would tighten sharply if the Fed rolled out these facilities on Sunday. It is also expected that swap spreads and credit spreads further out the curve would tighten. Finally, we would also expect to see significantly less USD demand in the currently very strained cross currency basis market. Recall, offshore banks and other entities frequently use the cross currency basis market as a source for USD when the commercial paper market is less readily accessible (such as around year-end).

The flipside, of course, is that the Fed does nothing today and tomorrow all hell breaks loose, forcing the Fed to do even more to restore confidence, especially after Friday’s historic 2000 Dow point surge. In any case, the Fed is cornered and whether it wants to or not, it will have to fire an even bigger bazooka in the coming 24 hours or else risk everything it has done in the past 107 years come crashing down.

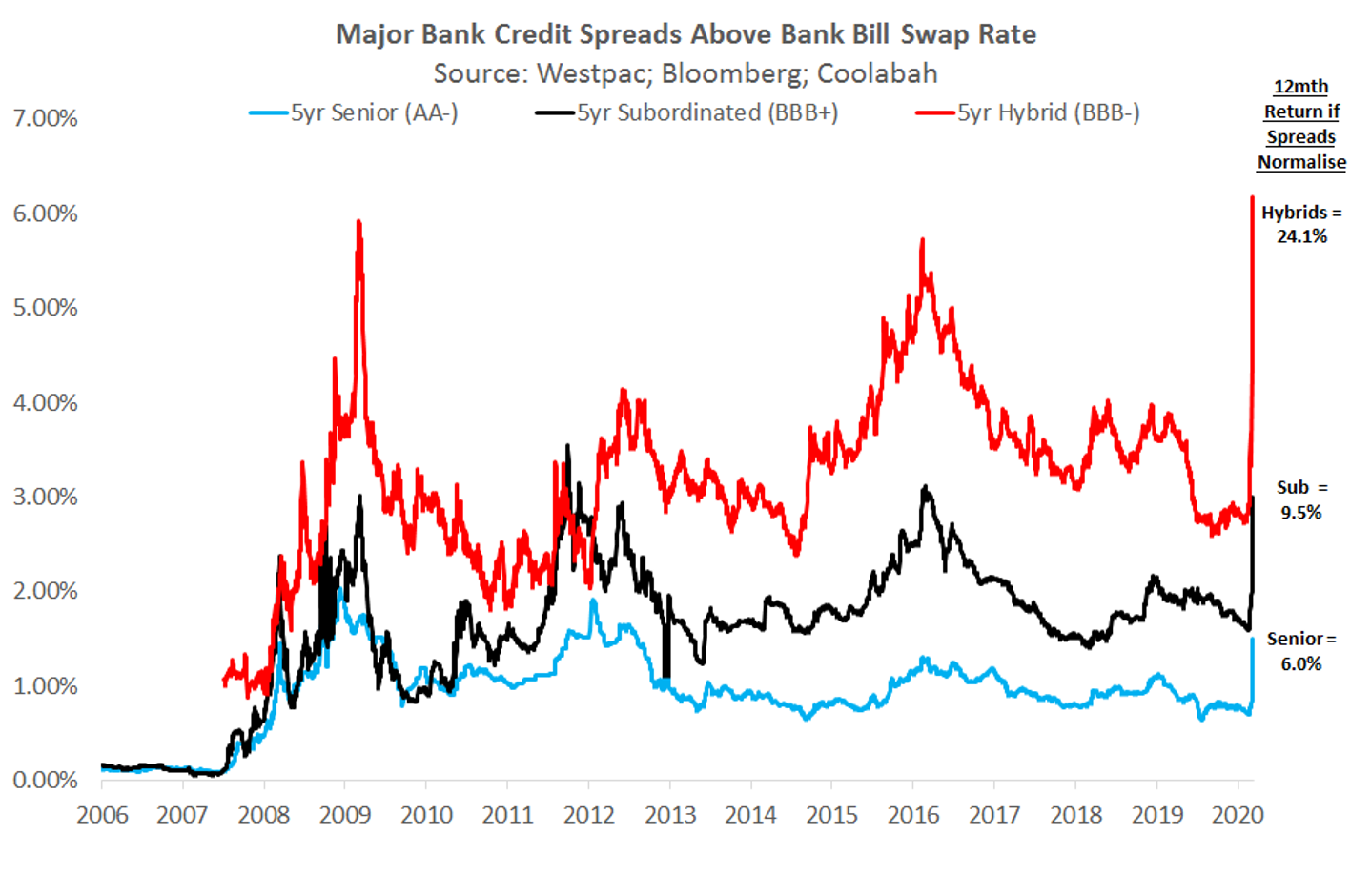

H&H here. Meanwhile, Australian bank funding spreads:

And from the RBA: ZZZZZZZZZzzzzzzzzzzzzzzzzzzzzzz…