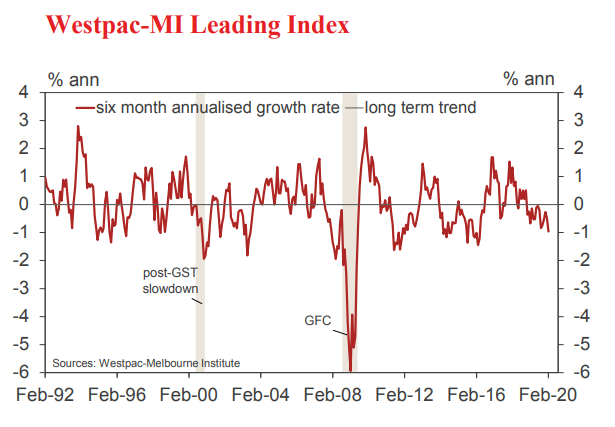

• The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, fell from –0.49% in January to –0.96% in February.

The Index growth rate has been running consistently below trend for 15 months. That signal is indicative that the Australian economy is entering this extremely difficult Coronavirus period with insipid momentum and is therefore more vulnerable to the shock.

On March 9 Westpac forecast that the Australian economy would experience a recession in 2020.Crucially that forecast was based on the negative effects of the virus peaking near the end of the June quarter.

We reconfirmed that view following the announcement of the Government’s $17.6 billion Stimulus Package. Today, following even more adverse growth developments over the last week we have revised down our growth forecasts to anticipate an even deeper recession with the unemployment rate peaking at 7% in the second half of 2020.

The Leading Index growth rate has deteriorated over the last six months from -0.84% in September to the current –0.96%. Much of this reflects initial developments around the Coronavirus outbreak that are set to intensify dramatically in coming monthly reads. The main drivers of the 0.12ppt shift over the six months to February have been a sharp sell-off in the sharemarket (–0.32ppts);

a further decline in commodity prices (–0.13ppts); and a rise in consumers’ job loss fears (–0.12ppts). These negatives are set to intensify sharply in the coming month – February’s 8.2% fall in the ASX has been followed by a 20% slump in the March month to date and Australia’s key commodity prices have also recorded sizeable declines (iron ore a notable exception).

The current weak signal from the Index is broadly based with seven of the eight index components contributing negatively to the Index growth rate. The sole positive contributor – a widening yield spread – is keying off expectations that RBA rate cuts will lower short terms interest rates cuts. But even here, the dramatic decline in long term bond rates is dampening the positive signal.

The Reserve Bank Board cut the cash rate 25bps at its March meeting, responding to a rapidly deteriorating Coronavirus situation. The following Monday, the RBA announced a series of liquidity measures aimed at stabilising financial markets with additional policy initiatives to be outlined on March 19. We expect these to include a further 25bp reduction in the cash rate to 0.25% – almost certain to be the effective lower bound target for cash rate; a quantitative easing programme that is likely to target the risk free yield curve; and, crucially, some initiatives to provide banks with long term funding at around the overnight cash rate that would be tied to loans to businesses and households.

So, vulnerable, in fact, that recession is here, from Bill Evans:

On Monday, March 9, we forecast that the Australian economy would experience a recession in 2020 with the economy contracting by 0.6% in the first half although we expected growth in the second half of 2.2% as the economy recovered from the disruption associated with COVID-19.

Our central assumption was that the COVID-19 threat would peak in the June quarter and by quarter’s end confidence and activity would begin to recover.

We described 2020 as a severe disruption or technical recession to differentiate from the last two recessions in Australia when the unemployment rate spiralled from 6% to 11%.

Our figuring last week set the forecast peak in the unemployment rate at around 5.8%- 6%, up from the current level of 5.3%. The relatively modest increase in the unemployment rate was particularly reflective of the expectation that the disruption would be relatively short when compared to earlier recessions and viewed as such by business that there would be a degree of labour hoarding.

Later in the week we analysed the Government’s $17.6 billion Stimulus Package and concluded that the Package would not be sufficiently stimulative to avert a recession in 2020.

Our key assumptions around the Package focussed on the likely impact on spending from the $4.76 billion payments to pensioners and social security recipients and the instant asset write off provisions.

We assessed that pensioners would save around 75% of payments and social security recipients would save around 60%.

Pensioners are likely to be cautious given the collapse in bank deposit rates and health concerns. In that regard the 13.8% collapse in confidence amongst the over 65 year olds in the latest Westpac MI Consumer Sentiment Survey signals caution. Social security recipients will be unnerved by the COVID -19 threats and discouraged by the “one off” nature of the income boost.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.