But the OPEC+ deal also aided America’s shale industry and Russia was increasingly angry with the Trump administration’s willingness to employ energy as a political and economic tool. It was especially irked by the U.S.’s use of sanctions to prevent the completion of a pipeline linking Siberia’s gas fields with Germany, known as Nord Stream 2. The White House has also targeted the Venezuelan business of Russia’s state-oil producer Rosneft.“The Kremlin has decided to sacrifice OPEC+ to stop U.S. shale producers and punish the U.S. for messing with Nord Stream 2,” said Alexander Dynkin, president of the Institute of World Economy and International Relations in Moscow, a state-run think tank. “Of course, to upset Saudi Arabia could be a risky thing, but this is Russia’s strategy at the moment – flexible geometry of interests.”

…the decision to take on shale could backfire. While many drillers in Texas and other shale regions look vulnerable, as they’re overly indebted and already battered by rock-bottom natural gas prices, significant declines in U.S. production may take time. The largest American oil companies, Exxon Mobil Corp. and Chevron Corp., now control many shale wells and have the balance sheets to withstand lower prices. Some smaller drillers may go out of business, but many will have bought financial hedges against the drop in crude.In the short run, Russia is in a good position to withstand an oil price slump. The budget breaks even at a price of $42 a barrel and the finance ministry has squirreled away billions in a rainy-day fund. Nonetheless, the coronavirus’s impact on the global economy is still unclear and with millions more barrels poised to flood the market, Wall Street analysts are warning oil could test recent lows of $26 a barrel.

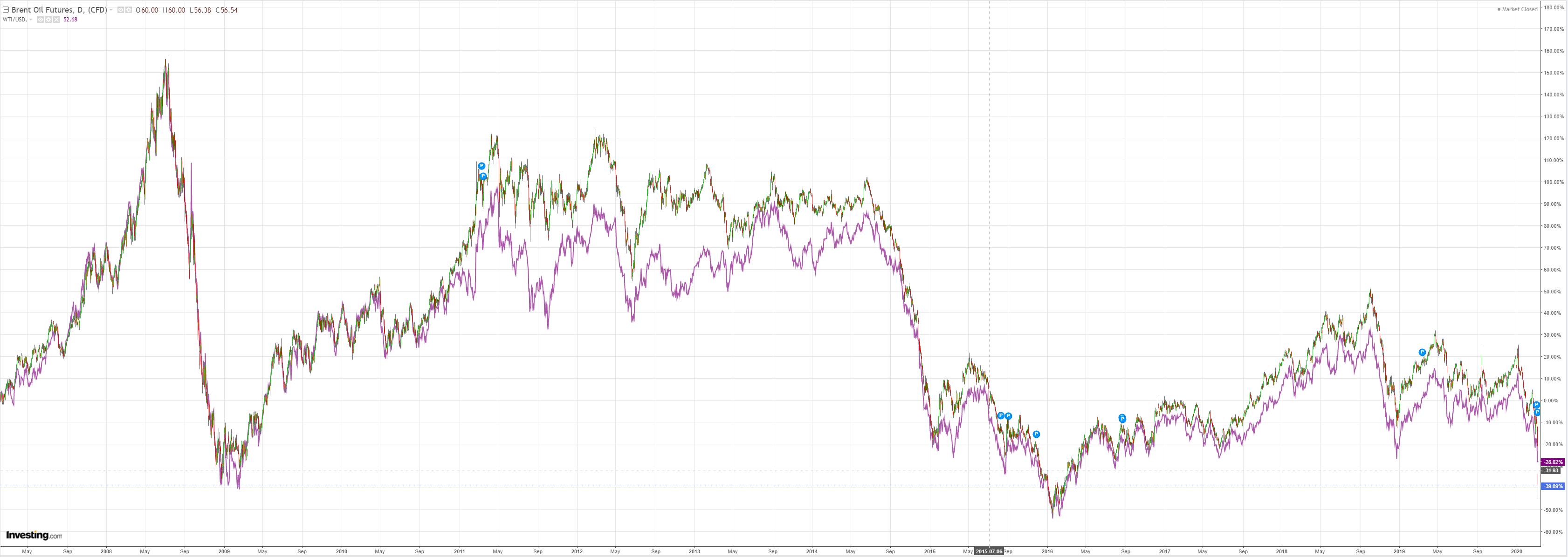

Saudi has dropped prices and lifted output above 10mb/d. There are reports it could go as high as 12m/bd.

Advertisement

It doesn’t really matter. The world is already swimming in oil as the COVID-19 demand shock deepens. I already saw oil in the twenties. Now it’s going into the teens.

First, this would normally aid consumers. But this time that isn’t going to happen. Within a month they’ll all be huddled at home.

Second, the impact on suppliers will be severe. There will casualties across the US oil patch, in particular. In turn, this will add pressure to the US junk bond market. During the 2016 oil bust this dynamic spread quickly into the broader high yield bond market. Happening at this juncture, it will make the extant freeze in US corporate bond markets much worse, very quickly.

Advertisement

Third, when oil falls, wider commodity markets generally do too. Oil is the major input cost for mining and logistics. A deflationary tsunami is being unleashed and sovereign bonds are going to be bid even more wildly.

Fourth, Australia will see its LNG sector pulverised. This is good to the extent that on the east coast it adds almost nothing to economic activity or taxes. But the west coast sector does so that will hurt. There will be upside in falling gas prices if they get passed through but it won’t happen quickly.

The most important impact will be on the trade balance which will be smashed as the price of contract LNG craters with oil. This will be offset in the capital account as profit outflows also collapse. But for markets, the return to trade deficit, indeed twin deficits as the budget slides, will not be welcomed and add further pressure to the Australian dollar.

Advertisement

It is testament to Australia’s disastrous energy policy that we’ll probably be better off, in and of ourselves, with lower oil and gas prices. However the exacerbation of the global credit shock means that, overall, the oil crash is another falling domino in an accelerating line of them headed into recession.

Here’s Goldman with more good news:

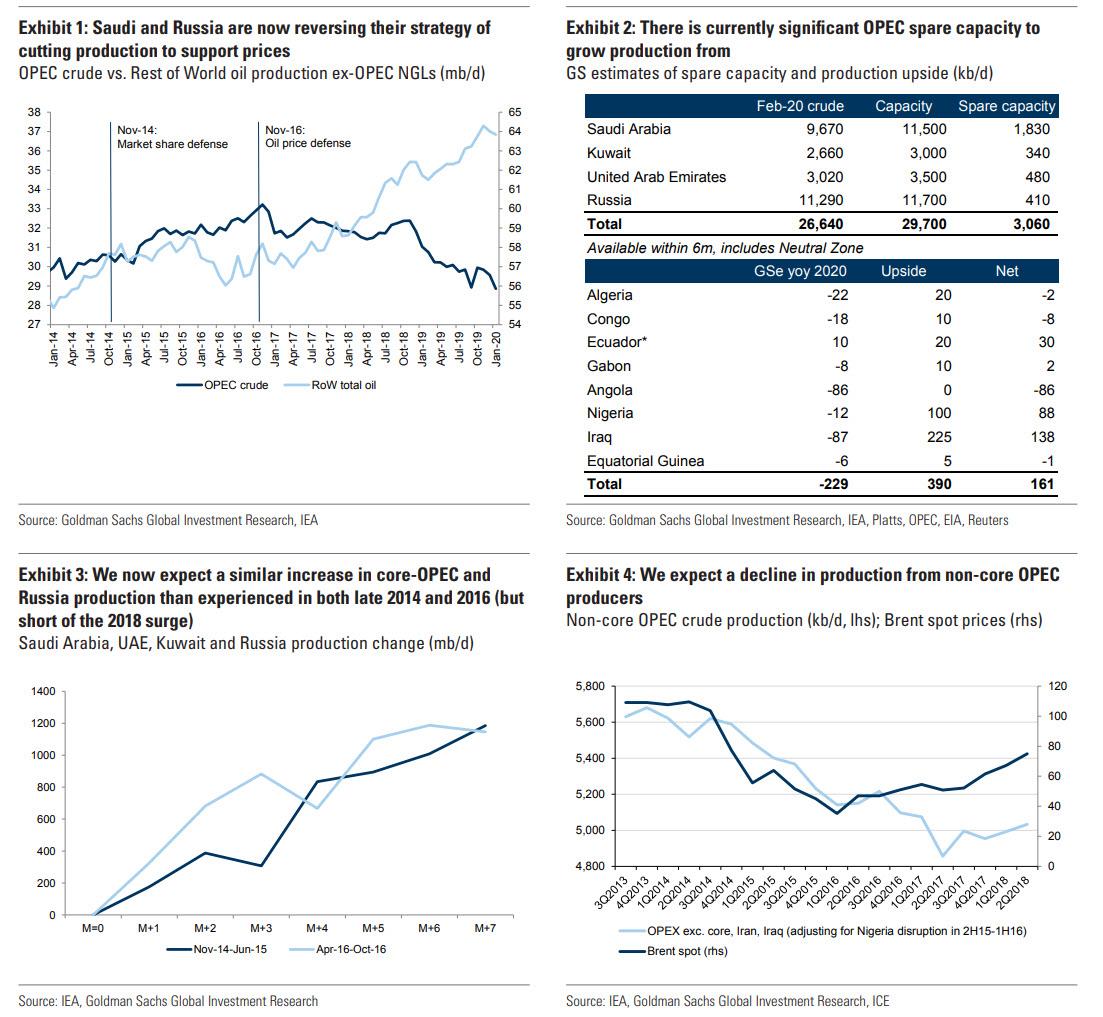

1. At its core, the decision from Russia to unwind the artificial price support that OPEC+ had created since 2016 is rational. As we argued previously, these cuts to defend prices instead of market share defied the economic incentive of large low-cost producers without pricing power, with Russia’s economy able to cope with lower oil prices. Since November 2016, OPEC and Russia production was cut by 4.4 mb/d while the rest of the world increased output by 5.7 mb/d. Media reports over the weekend relayed that Russia’s decision was indeed squarely targeted at the shale sector given its current financial distress but also at the US administration in response to recent US sanctions on its Nord Stream 2 gas pipeline and Rosneft.

2. Such a sanction motivation, Russia’s comment on Friday to continue cooperation within the OPEC+ charter, Saudi’s aggressive OSP retaliation and the stress that low oil prices would create on its economy (itself already on weaker footing than in 2014) all suggest that a reversal in coming months could be possible, bringing us back to our post-coronavirus price forecast. While we can’t rule out such an outcome, we also believe that the OPEC+ agreement was inherently imbalanced and its production cuts economically unfounded. The aggressive cut to Saudi’s OSPs and Russia’s reluctance to be pushed into a deal on Friday both also point to a low probability of an immediate agreement. As such, we base case that no such deal occurs in coming quarters, with any response only likely at sharply lower prices anyways.

3. The oil market is now faced with two highly uncertain bearish shocks with the clear outcome of a sharp price sell-off. While there is so much that we still don’t know about oil fundamentals in coming months, we also know very well from 2015-16 how such a rebalancing will take place. Our initial attempt to frame this supply vs. demand divergence points to a 2Q20 record large surplus of c. 2.9 mb/d. This reflects the “price war” scenario we laid out on Friday, with an 1.0 mb/d aggressive ramp-up in core-OPEC and Russia output through 2Q, similar to what occurred in both 2014 and 2016 (and consistent with news reports that Saudi Arabia is already looking to lift April production well above 10 mb/d). On our quantitative pricing model, this would point to Brent prices averaging $30/bbl in the quarter with clear risks that prices at times overshoot to the downside.

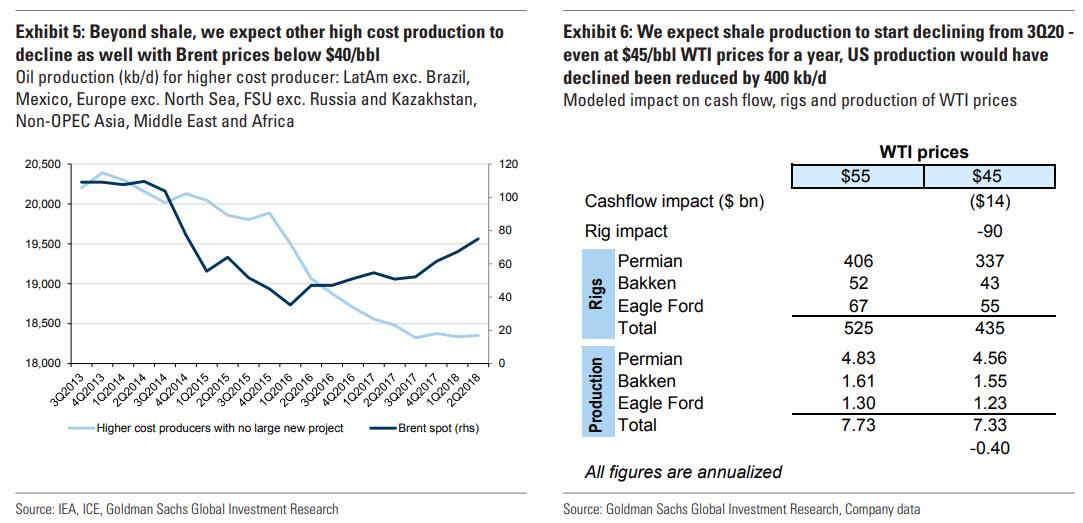

4. Such price levels will start creating acute financial stress and declining production from shale as well as other high cost producers. Specifically, we assume legacy production decline rates outside of core-OPEC, Russia and shale increase by 3% to 5% to return to their 2016 highs. In the case of shale, we assume a negligible response in 2Q but with production falling sequentially in 3Q by 75 kb/d and with declines increasing to 250 kb/d qoq in 4Q20. This will not, however, prevent a 3Q20 surplus of 1.2 mb/d and inventories peaking above their 2016 highs and Brent spot prices staying at $30/bbl on average. In fact the negative feedback loop of lower oil prices on energy exporting economies could exacerbate the decline in oil demand. At that point, the fundamental rebalancing could require oil prices falling to operational stress levels for high cost producers with well-head cash costs near $20/bbl.

5. Assuming no change in production policy, we would expect a market deficit to start in 4Q20 and that would run down excess inventories through 2021, with the outlook for draws helping prices rebound that quarter to $40/bbl like they did in the spring of 2Q16. Our 2021 quarterly Brent price forecasts are now $45/bbl, $50/bbl, $55/bbl and $60/bbl with a long-dated price of $45/bbl Brent. This lower equilibrium reflects a lower marginal cost of production in coming years due to steady growth in core-OPEC and Russia production (from their spare capacity initially and new drilling subsequently). The significant level of spare and disrupted capacity (each more than 3 mb/d) as well as resilient non-OPEC growth above $60/bbl Brent were ultimately the reasons why we didn’t expect upstream under-investment to become bullish for oil prices for another few years. This Revenge of the New Oil Order, while bearish initially, will finally start the clock on such a binding under-investment, with a clearer line of sight on higher equilibrium prices in 2 to 4 years.

6. Reusing our template from 2015-16, we expect this fundamental rebalancing to occur in three phases: 1) the survival phase, with the capitulation of large producers in dropping investment; 2) the inflection phase where inventories peak and the least fit producers engage in significant capital restructuring, including shuttering of assets; and 3) eventually the regeneration phase of a new industry with stranded assets ultimately shuttered or optimized.

7. While phases 1 and 2 played out over more than a year last time around (Nov-14 to Apr-16) and phase 3 never happened, we expect a much faster rebalancing this time around as shale and high-cost oil producers were already facing sharply higher costs of capital over the past year due to persistently poor shareholder returns. For example, as of last Thursday before the collapse of the OPEC+ agreement, US HY Energy credit spreads were already above 1000 bps, a level they had last traded at in March 2016 when WTI prices were trading at $35/bbl. This faster rebalancing – which may in fact be even quicker than our first path given the ongoing coronavirus-led contraction – may itself be the catalyst for Russia to hold off on any output agreement until it is completed and may help explain why this market share battle is happening now. In particular, there is no longer a wave of long-cycle projects coming online, with the last of these projects starting in 2020. Illustrating this point, our new global 4Q20 supply forecast ends up being lower without a OPEC+ cut than our prior expectations which featured a 1 mb/d cut from 2Q20.

8. From a market perspective, we expect the price decline to play out in two steps. First, already started large inventory builds will lead to a sharp steepening of the forward curve into contango to cover the quickly rising costs of storing all these barrels. We therefore recommend closing the long Dec-20 vs. Dec-21 Brent timespread trade that we initiated on 3-Feb-20 but keeping the accompanying long Jun-19 $49/bbl Brent put position added on 14-Feb-10, with the portfolio so far performing positively. Second, reflecting the structural nature of this repricing, long-dated prices will also fall to the market’s new clearing marginal cost of production likely initially near $40/bbl for Brent. During the inflection phase when inventories are at their peak, we could see a flattening of the forward curve near the trough in prices, the typical sign of producer capitulation and distressed hedging. This inflection phase is also a period where we would expect price volatility to surge to potentially new highs. From there, the path to a rebalanced market will eventually lead to sustained backwardation.

9. From a crude differential perspective, we expect the initial sell-off to come alongside a sharp compression of the WTI-Brent differential to potentially near parity like experienced in Jan-16, reflecting the cheaper cost of storing crude in the US and the lack of buying of uncontracted US crude by foreign refiners facing both weak demand and cheap seaborne Middle East crudes. From a product market perspective, we expect highly volatile cracks given the diverging forces of collapsing demand and surging excess crude supply. After a likely rebound on the first days of the crude price collapse, cracks should retrace given the ongoing demand shock (especially since refiners respond to % margin incentives against a backdrop of lower crude prices). Once refiners cut run, we would then expect the crude surplus to prevail and help margins recover even if the demand recovery remains shallow.

10. The impact of this structural shift will of course be felt well beyond the oil market, with likely significant distress for energy exposed sovereigns and sectors. In particular, we don’t expect the gas market to be spared. If Russia is indeed responding to both the competition from shale and the US sanctions on its new EU gas pipeline, we would expect its gas exports to Europe to rise as well. Such risks of higher Russian flows just make an already unsustainable balance potentially worse. As a result, we now base-case that the oversupply in the EU gas market will require a shut-in of the US LNG exports, and ultimately a shut-in of Appalachia gas production. Admittedly, this is a less surprising outcome than for oil since the global gas market has been heading that way following the collapse in Chinese demand due to the coronavirus, a notable surge in US LNG exports in February and the impact of a very warm winter on heating-related gas demand.

11. With a collapse in shale oil drilling, we are however increasingly comfortable forecasting a tightening US gas market and rising Henry Hub prices in both 2021 and 2022, with new Appalachia and Haynesville drilling required to balance the US market. That is because even if Russia raised export levels in Europe, we would expect the global LNG market to still sequentially tighten from its 2019-20 oversupply (assuming normal winters ahead) and allow for steadily rising US LNG exports. Based on these views, we are cutting our 2Q and 3Q20 Henry Hub forecast to $1.50 and $1.75 but raising our 4Q20-1Q21 forecast to $3.00/mmBtu with our 2021 summer forecast now up to $2.75/mmBtu. Our 2Q-3Q20 TTF price forecast is now $2.10 and $2.40 with winter staying at $4.70/mmBtu. Our 2Q-3Q20 JKM price forecast is now $2.40 and $2.70 with winter staying at $5.80/mmBtu.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.