The ABS has released household wealth data for the December quarter of 2019, which revealed a big lift in wealth driven by property:

Household wealth

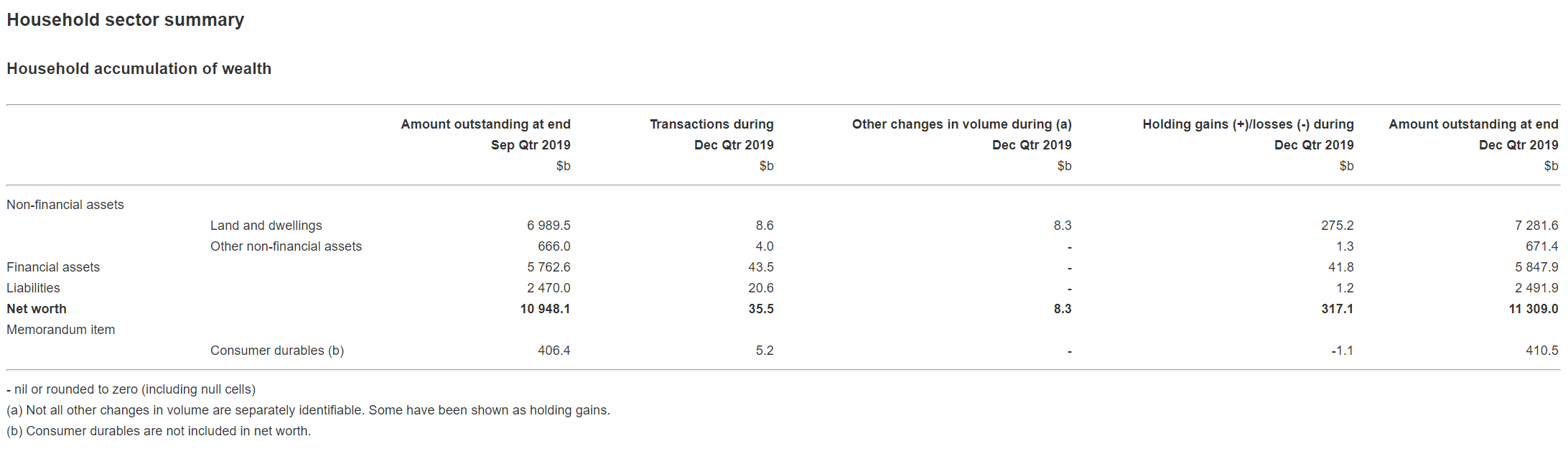

Household net worth (wealth) increased $360.9b (3.3%) in December quarter 2019 driven by a $382.8b increase in total assets. This was partly offset by a $21.8b increase in total liabilities. Household wealth per capita increased $12,809 to $442,705, the largest increase since December quarter 2009. With quarterly growth in household wealth at its highest in ten years, through the year growth in household wealth has recovered from the negative results seen in 2018-19.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.