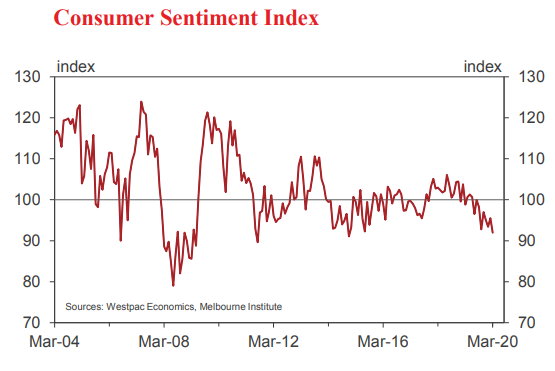

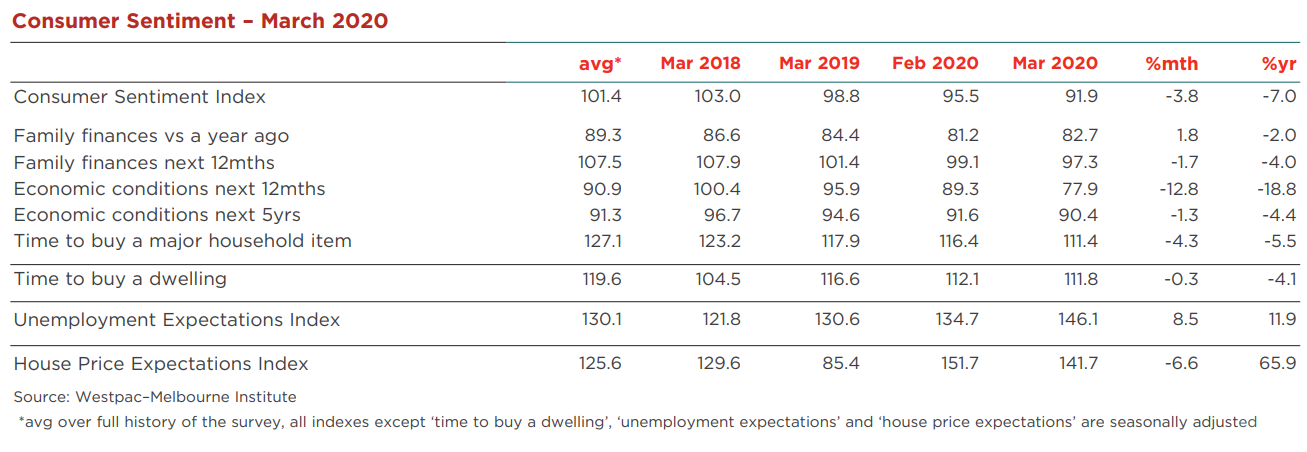

• The Westpac-Melbourne Institute Index of Consumer Sentiment fell 3.8% to 91.9 in March from 95.5 in February.

The worsening coronavirus outbreak and associated rout in financial markets have had a major impact on sentiment this month. The Index has hit a five year low. In fact it is the second lowest level of the Index since the Global Financial Crisis when the Index bottomed out at 79, (with an average read of 86.8 over the period).

Therefore, while clearly very concerned, consumers are, for now, taking a more balanced approach to the situation than we saw during the GFC.

Other evidence of this can be found by comparing the ‘family finances’ and ‘time to buy a major household item’ components of the Index which registered 63.7 and 88.2 respectively at the low point of the GFC compared to the current reads of 82.7 and 111.4 respectively.

The survey detail shows consumers are rightly concerned about the near term outlook for the economy but are less perturbed about their finances or the longer term outlook for the economy. That is consistent with the notion that virus-related disruptions will be large but temporary.

At the time of last month’s survey, there were just over thirty thousand confirmed cases of COVID-19 with over 99% in China. A month later there are well over one hundred thousand cases globally with a quarter of these recorded outside of China, with infections rising rapidly in many countries.

Financial markets have also reacted sharply. After showing little change in February, the ASX dropped 11.5% between the February and March surveys (and by a further 4.5% since the latest survey closed). These falls have been despite a 25bp rate cut from the RBA and an emergency 50bp rate cut from the US FOMC.

Responses to additional questions on news recall show by far the highest recall was for news on the economy – 45% of consumers recalling news on this topic with over 85% saying that news as unfavourable. News on ‘international conditions’ also had a relatively high recall rate (25%) and was also assessed by around 85% of respondents as unfavourable.

About 20% of consumers recalled news on ‘interest rates’.

The RBA cut rates by 0.25% at its March meeting. However, we again saw consumers assess this news more negatively than usual. As we have noted previously, the favourable/ unfavourable mix on ‘interest rate’ news following rate cuts over the five years to 2016 was around 50/50 but has been closer to 30/70 for cuts in 2019 and 2020. That lukewarm

response is despite the major banks passing on the rate cut in full to mortgage interest rates.

Across the five component sub-indexes, the biggest fall was around expectations for the economy, particularly over the near term. The ‘economy, next 12 months’ sub-index recorded a spectacular 12.8% drop taking it to 77.9, a five year low but still comfortably above the GFC low of 62.9.

In contrast, the ‘economy, next 5 years’ sub-index only fell 1.3%, to 90.4. Clearly consumers expect very challenging conditions near term but are less concerned about medium term prospects.

Assessments of family finances were relatively stable. The ‘finances vs a year ago’ sub-index rose 1.8% although at 82.7 it remains 6.6% below the historical average. Despite the recent carnage in equity markets respondents were balanced about the 12 month outlook for their finances with ‘finances, next 12 months’ sub-index down by only 1.7%.

Notably, despite the RBA’s 25bp rate cut and that move by major banks to reduce mortgage rates by the full 25bps, sentiment amongst consumers with a mortgage declined 2.8% in the month.

At the same time, sentiment amongst older age groups fell more sharply, particularly those aged over 65 (–13.8%). This likely reflects several factors including the impact of lower deposit rates on incomes, the hit to superannuation from the sharemarket sell off and perhaps also a higher degree of concern about health risks from the coronavirus, which has a markedly higher fatality rate amongst those in older age groups.

A more positive aspect of the finer survey detail is a sharp 20% rebound in sentiment in regional NSW – an area hit hard by summer’s bushfires and severe drought.

The reading suggests bushfire aid and consistent rain are providing a welcome lift in confidence.

There are concerning signs for retailers that consumers are less inclined to spend. In particular, the ‘time to buy a major household item’ sub-index showed a material 4.3% fall to 111.4, a five year low. That may reflect both increased uncertainty about the economy and concerns about the health risks associated with public places.

A sharp rise in job loss fears also suggests consumers may look to delay or cut back on big ticket expenditure items. The Westpac-Melbourne Institute Unemployment Expectations Index jumped sharply, rising 8.5% to 146.1 in March, a four year high (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). Consumers now look to be bracing for a significant deterioration in labour market conditions in 2020.

Sentiment around housing also softened. The ‘time to buy a dwelling’ index dipped slightly in March, a 0.3% decline taking the index to 111.8. While that looks resilient compared to other aspects of the survey, it is unusual for the index to fall following an interest rate cut. With residential property the most interest rate sensitive sector of the Australian economy, homebuyer sentiment typically shows an even more positive response to rate cuts than consumer sentiment overall. The survey detail continues to suggest deteriorating affordability is becoming more of an issue for some segments, with buyer sentiment amongst age groups that drive first home buyer activity showing more of a pull back.

Consumer expectations for house prices fell sharply.

The Westpac-Melbourne Institute Index of House Price Expectations Index fell 6.6% in March, the largest monthly decline since February last year. That said, at 141.7, the Index is still well above the long run average of 125 and up 66% on a year ago. Most consumers still expect prices to rise over the next year but the result is consistent with some slowing in momentum.

Responses to additional questions on the ‘wisest place for savings’ show a slight easing in risk aversion, but coming from a very high starting point. Consumers still heavily favour ‘safe options’, 63% nominating deposits, superannuation or ‘pay down debt’ as the best place for savings, compared to 64% in December. The proportion favouring real estate rose slightly to 13% from 10% in December and a record 40 year low of 9% this time last year. This may indicate some increased interest from investors, a group that has been less prominent in this current upswing in the housing market than in previous cycles although the wider shock to sentiment is likely to see investors remain cautious.

The Reserve Bank Board next meets on April 7. Given the clear risks being faced by the Australian economy over the next few months the Board is likely to lower the cash rate by a further 0.25%.

That will take the cash rate target to 0.25%, the lower bound for the RBA’s policy rate, as indicated by the Governor in a speech on November 26 last year. The next policy approach is likely to involve a form of unconventional monetary policy where indications are that the Board favours the approach of setting a rate target further out the yield curve and signalling the commitment to defend that target.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.