The Grattan Institute has released its submission to the federal government’s Retirement Incomes Review, which explicitly argues that Australia’s system of compulsory superannuation is failing lower-income workers. Grattan also argues that instead of lifting the superannuation guarantee, which would cost the Budget an additional $2 billion a year, the government should instead bolster the Age Pension, raise Newstart, lift rent assistance, and make superannuation concessions more progressive:

Super is the wrong tool to ensure low-income Australians have adequate retirement incomes.

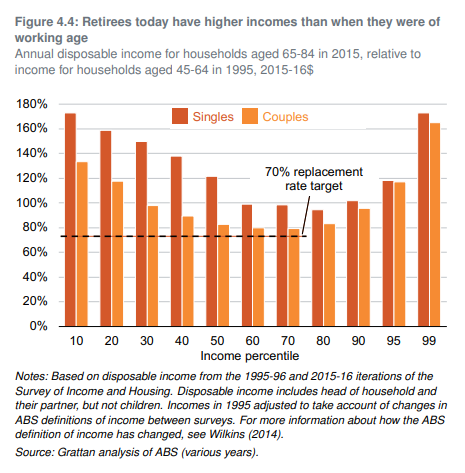

Some commentators – particularly those associated with the superannuation sector – advocate for super to help low-income Australians, especially women, to avoid poverty in retirement. Yet super is poorly placed to boost retirement incomes for low-income Australians at risk of poverty. Super is a contributory system: you only get out what you put in. If you earn low wages, you will have small compulsory super contributions. For people on low and modest incomes, the cost of increasing the Super Guarantee would hurt them during their working lives, when they’re typically under even more financial stress, by reducing their take-home pay. In fact the poorest 30-to-40 per cent of workers can expect a pay rise in retirement, because the Age Pension and the income they get from compulsory retirement savings will be higher than the wage they receive during their working life (see Figure 4.5 on page 56).

Previous attempts to use super to help low-income earners have given money to workers who we predict might end up with poor outcomes in retirement. Targeting those who may have low lifetime incomes on the basis of their incomes in a given year will never be as well targeted as using the Age Pension to target support to people otherwise at risk of poverty in retirement. Grattan Institute’s 2017 paper What’s the best way to close the gender gap in retirement incomes? showed that about a quarter of the government’s support to low-income earners via the Low-Income Superannuation Tax Offset (LISTO) leaks out to support the top half of households…

Instead the income support system, specifically the Age Pension (and Rent Assistance for renting retirees), is the best tool to prevent poverty in retirement. Eligibility for the pension is based on the income and assets of the whole household, including those of a spouse. And by assessing eligibility at retirement, the Age Pension better targets retirement incomes to those who need it most. Measures to boost the value income support payments for retirees, especially for renters, are likely to materially reduce the number of Australians, including existing retirees, suffering poverty in retirement…

Super is taxed very concessionally compared to other savings vehicles… Half the benefits flow to the wealthiest 20 per cent of households, who already have enough resources to fund their own retirement, are unlikely to qualify for an Age Pension, and therefore do not need government support.

Treasury projections in the consultation paper to the Retirement Income Review show that the lifetime value of super tax breaks to high-income earners remains much higher than the value of the Age Pension for low-income earners, even after recent reforms…

Without clear objectives, the super system has provided excessively generous tax breaks that cost the budget $35 billion each year in lost revenue, with half the benefits flowing to the top 20 per cent of income earners who already have enough resources to fund their own retirement. These excessively generous tax breaks should be wound back…

Given the reality that most Australians will have enough money in retirement, there is no need to boost retirement incomes across the board. Increasing the Super Guarantee as planned would effectively compel most people to save for a higher living standard in retirement than they enjoy in their working lives.

Even if governments wanted to boost retirement incomes, the planned increase in compulsory super contributions to 12 per cent is an ineffective way to get there. Raising the Super Guarantee to 12 per cent would reduce wages today and do little to boost the retirement incomes of many low- and middle-income workers tomorrow. It would lead to lower pensions for both current and future retirees by suppressing the value of the wage-benchmarked Age Pension. Pushing for more retirement savings when they are not needed is simply a recipe for larger bequests, leading to widening wealth inequality over time as those unused savings are passed on to future generations.

Scrapping the increase in compulsory super to 12 per cent would also save the Budget $2 billion a year.

Grattan is correct. Lifting the superannuation guarantee to 12% is unambiguously poor policy that would lower workers’ take-home pay, reduce federal budget revenue, and increase inequality.

The only winners from doing so are the superannuation industry players, which would earn fatter fees from having more funds under management.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.