I don’t know, I think it’s pretty bad. Via MarketWatch:

Leland Miller is CEO of the China Beige Book, a research firm that collects data from surveys of thousands of Chinese companies and industry participants to construct a report on the economy that’s more granular — and possibly more candid — than the notoriously opaque Chinese government data.

…“The situation on the ground is materially worse than what has come out in the media,” he said in an interview.

MarketWatch: How bad is the situation in China?

Leland Miller: Since 2012, when we started collecting data, we have never seen our headline index turn negative. This month it did. Our flash data shows nearly every major measurement is in contraction. I do always stress that this is early data.

(Only about half of the roughly 3,500 firms that report in the full-month version contribute to the flash report.)

MarketWatch: Which is the single data point that’s most telling to you?

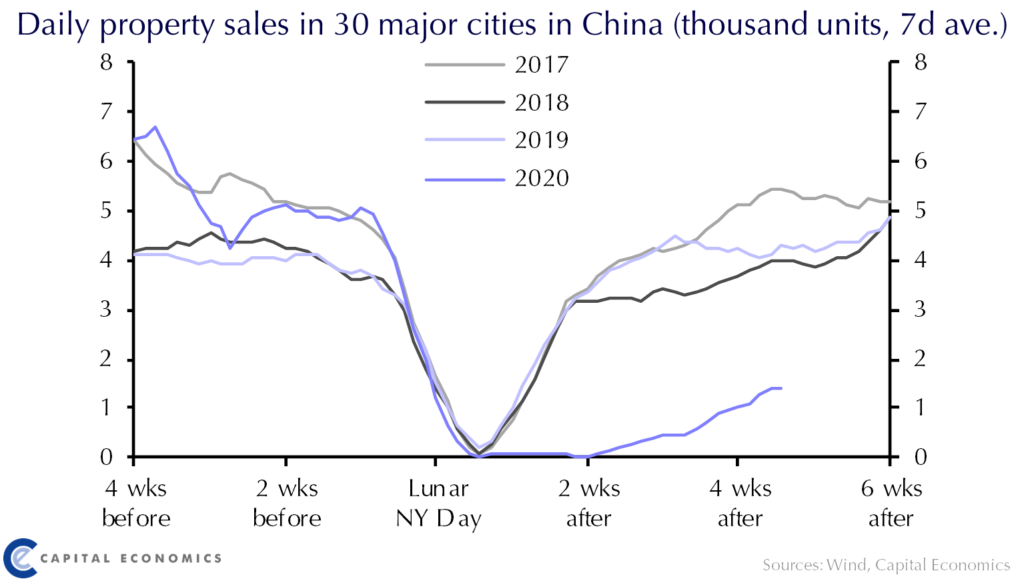

Miller: The numbers in the property sector are remarkable. It confirms this sector is at the bottom of the food chain in China right now, the last priority for Beijing in a long list of priorities. Property is extremely important because it’s the sector in which most Chinese have large portions of their wealth. Chinese people can’t get money out of the country so they’re stuck with only a few opportunities to diversify. The bond market is scary. The stock market is scary. Property has always been the least scary thing and the Chinese government has always known how important it is as a store of household wealth. It shows they’re more afraid of the bankruptcies of small and medium-sized enterprises. At least there may finally be a culling of the herd in terms of (real estate) developers and overleveraged firms allowed to die.

On the positive side, we’re seeing the job growth numbers in slight contraction. It’s remarkable they’re not much worse than that. This is an economy that could be in contraction for a long time, yet firms aren’t firing people. You can’t pay your people, you have no cash flow, no customers, so you’re paying them to stay home right now. (The lack of layoffs) is one reason you’re not seeing big-bang stimulus yet.

MarketWatch: Can you talk more about what kind of stimulus options the Chinese government does have available and how effective they can be?

Miller: The big fear is that there will be millions of firms defaulting because there’s no cash flow. The government doesn’t want that to happen, that would be a disaster. And mass layoffs would be bad for the party. So people are looking to see what China is doing as far as fiscal and monetary policy. But the state controls almost all the counterparties. The banking system is run by the state, it loans to state entities. It can order them to do whatever it needs, like not call in loans. The most important lever they have is simply not allowing banks to call in loans .

MarketWatch: What does China’s economic situation mean for the rest of the world – markets, economic growth, supply chains, and so on?

Miller: I would expect the data to get better if only because in March you’ll see firms back to work and the outbreak will hopefully be less terrible. Conditions — and data — should improve. But the implications of data anywhere near this bad is: China is an important cog in the supply and demand chains of the world. Globalization runs through China. Car factories around the world can’t build their cars because they can’t get their inputs from China. China buys a lot of commodities — oil and so on. Even if the outbreak can be contained, which doesn’t look like it, the economic impact can’t be.

MarketWatch: How should American investors parse upcoming official reports out of China?

Miller: You’ve got to figure that any report that comes out of China, whether economic or medical, is going to be political. “Take it with a grain of salt” may be too charitable. There aren’t easy ways of getting the truth. The truth is usually something between what the Wall Street banks think, which is way too optimistic and financial Twitter chatter which is too alarmist.

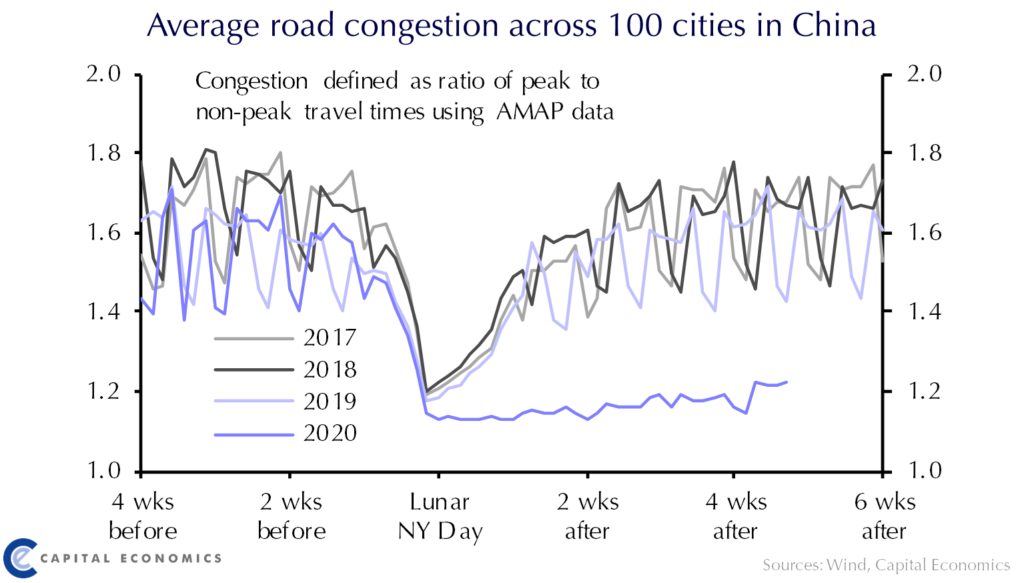

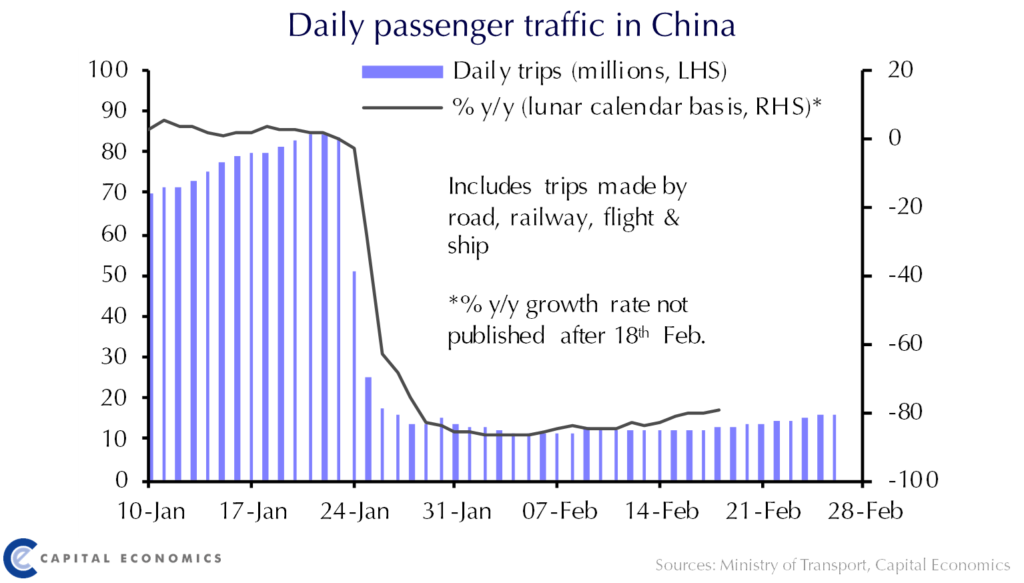

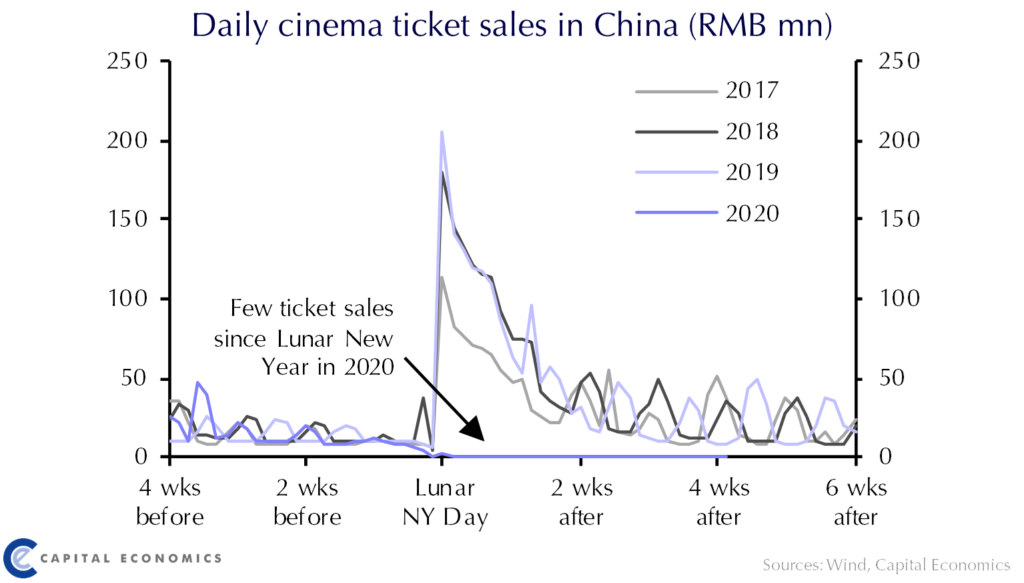

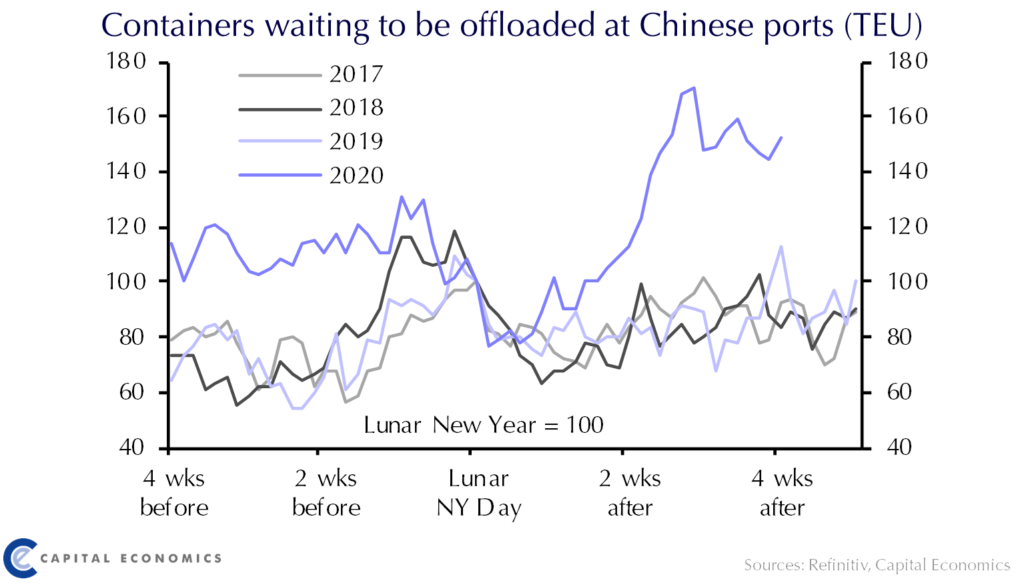

Yep. Here are the latest Capital Economics charts:

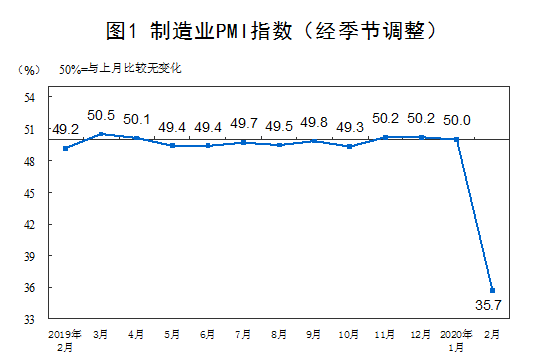

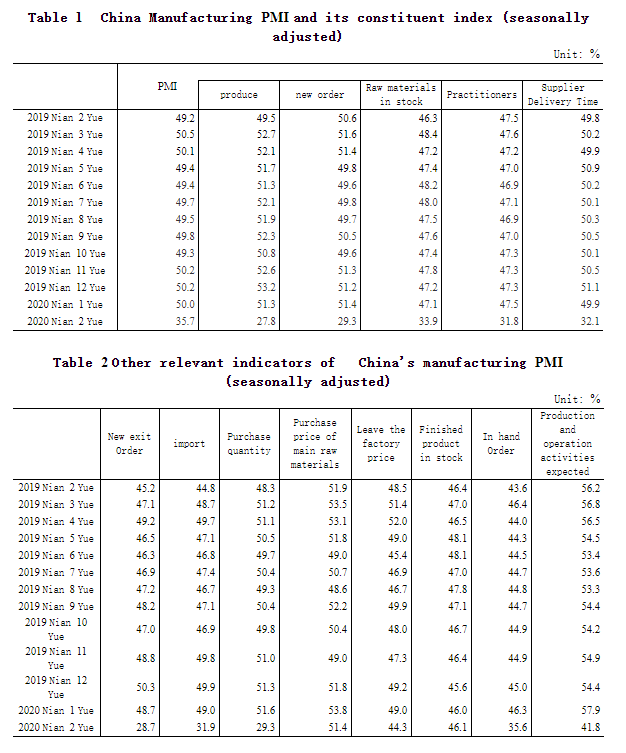

The February PMIs were an absolute write-off. Manufacturing:

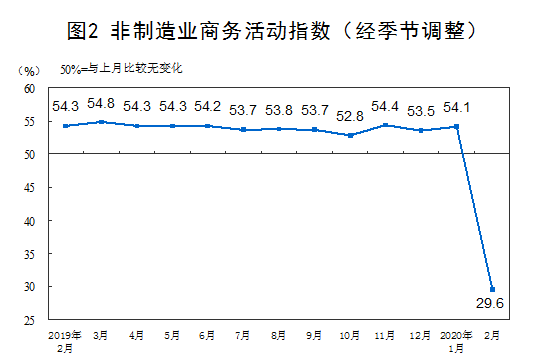

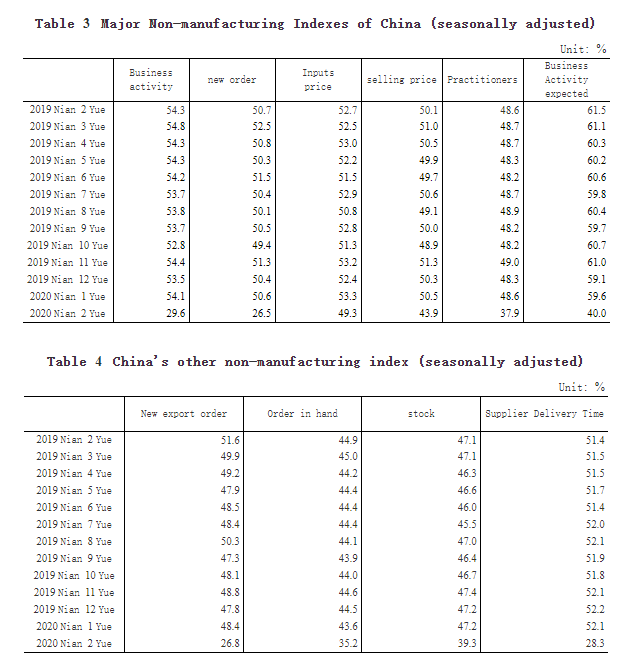

And services:

Export orders were as bad as local:

Most worrying for Australia:

The business activity index of the construction industry was 26.6% , a decrease of 33.1 percentage points from the previous month.

Although this will obviously improve, there’s no v-shaped recovery coming as services business lost is never regained given there is no inventory cycle.

The NBS noted:

Although the new crown pneumonia epidemic has caused a great impact on the production and operation of Chinese enterprises in the short term, under the strong leadership of the Party Central Committee with Comrade Xi Jinping as the core, the epidemic has been initially contained, and the negative impact on production is gradually weakening. Enterprises The rate of resumption of work resumed quickly, and market confidence recovered steadily. Purchasing managers survey shows that medium-sized enterprises 3 Yuedi return to work rate will rise to 90.8% , with manufacturing to 94.7% , respectively, than the current rise 11.9 and 9.1 percentage points. Recently, a series of policies and measures such as tax and fee reduction, financial services, rent reduction and employment subsidy for the epidemic, especially support for small and medium-sized enterprises to pass the crisis, have been gradually implemented, which will effectively alleviate the difficulties brought by the epidemic to the production and operation of enterprises. To further boost corporate confidence and accelerate the pace of resuming production and production, it is expected that China’s purchasing manager index will improve in March .

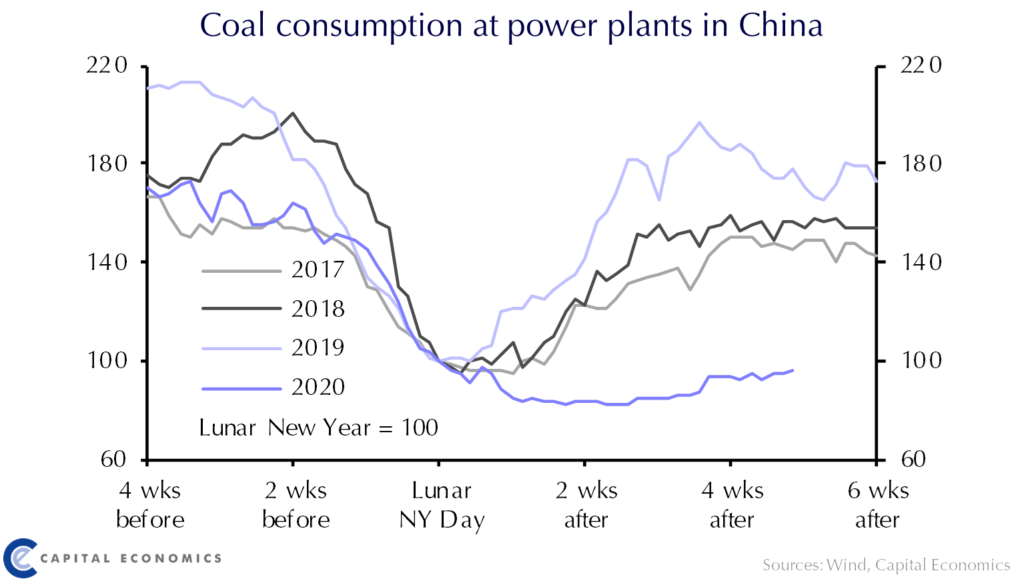

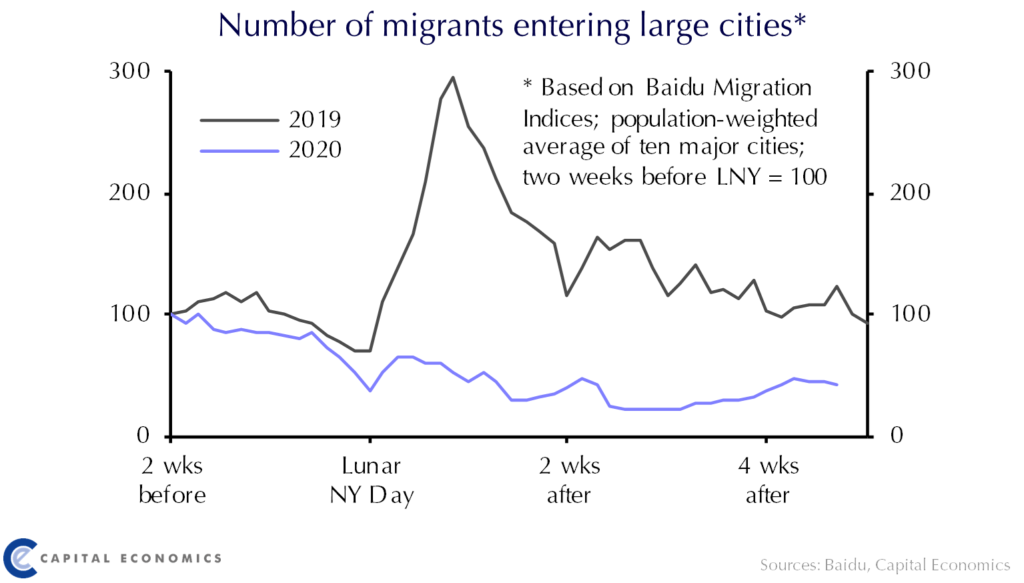

Beleive that if you want. They don’t even have workers:

It will be months before China returns to full capacity, even if we ignore a rapidly deteriorating external environment.