Last week, investment bank Macquarie warned that the share market losses from the coronavirus bear market would be even worse than the Global Financial Crisis (GFC):

Macquarie warned the Australian bourse could fall another 27 per cent if the pandemic triggered a long-lasting global recession.

The ASX 200 had fallen about 30 per cent when Macquarie issued the research note, implying a peak-to-trough fall of about 57 per cent if the bank’s worst case scenario eventuated…

“Once we see the peak in daily growth in US cases it will be a positive sign that we may be past the worst and this should allow equity markets to form a bottom,” Macquarie analyst Matthew Brooks said.

This forecast should send shivers down the spines of superannuation holders that are heavily invested in shares and closing in on retirement.

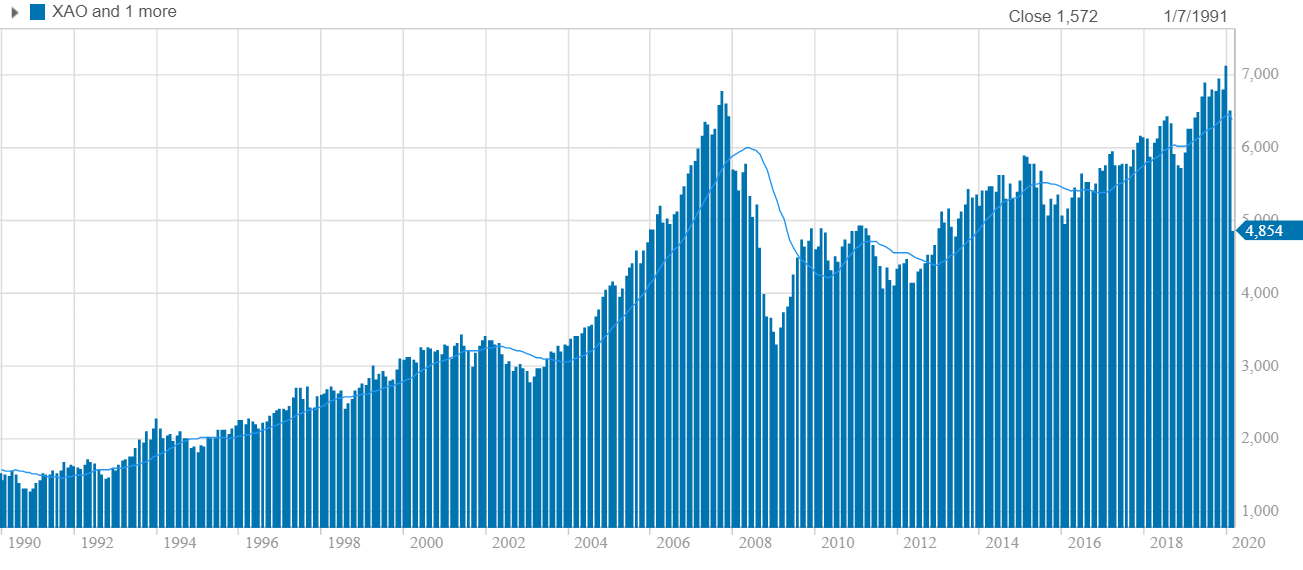

As shown in the next chart, Australia’s All Ordinaries Index, which tracks the 500 largest companies trading on the ASX, fell by around 55% peak-to-trough during the GFC:

Macquarie is tipping that the Australian share market could fall 57% peak-to-trough in the event that the world enters a prolonged global recession – an all but certain outcome in our opinion.

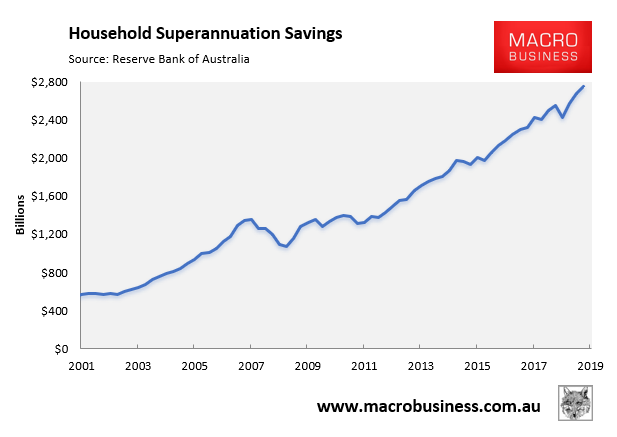

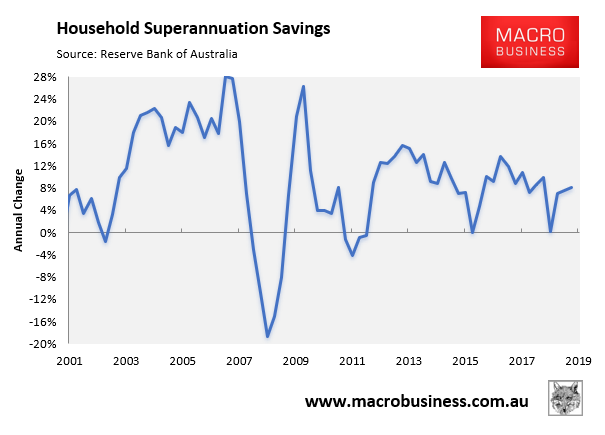

Following the GFC, Australia’s superannuation savings pool suffered a peak-to-trough decline of 21% and wiped off $270 billion in market value:

If those kinds of losses were repeated today, let alone Macquarie’s dire forecast, then $570 billion would be wiped off Australia’s household superannuation savings pool, which was $2.8 billion as at September 2019.

Of course, the outcome for the average superannuation holder would be even worse, given compulsory superannuation ensures a continuous inflow of funds, in turn propelling the savings pool forever higher.

Thus, many baby boomer’s retirement plans are likely to be decimated following the fallout from the coronavirus.

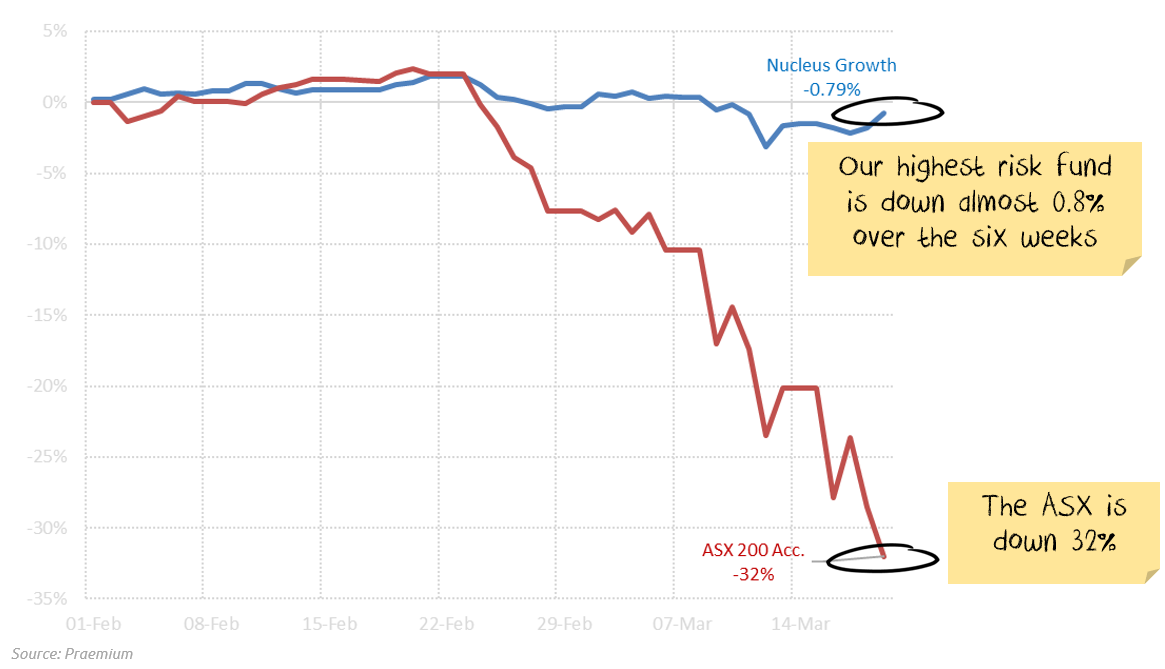

One group that will be sleeping easier are members of the MB Fund, which has massively out performed the market and protected its members’ nest eggs:

As noted by Damien Klassen, Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth:

Just to be clear, all of our funds are invested in liquid, traded blue-chip stocks, federal government bonds or cash. There is no shorting, no derivatives, no leverage. Just high-quality assets. These assets are held by our investors in their own accounts, with only their own tax issues. There is no co-mingling of assets and tax liabilities as you see in a traditional superannuation fund.

Many superannuation funds also hold significant levels of unlisted assets which they value themselves, most likely inflating returns.

————————————————-

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.