The DXY flame out continued Friday night. CNY is still looking dubious:

The Australian dollar tore the roof off:

Gold is useless:

Advertisement

Oil is going down, down:

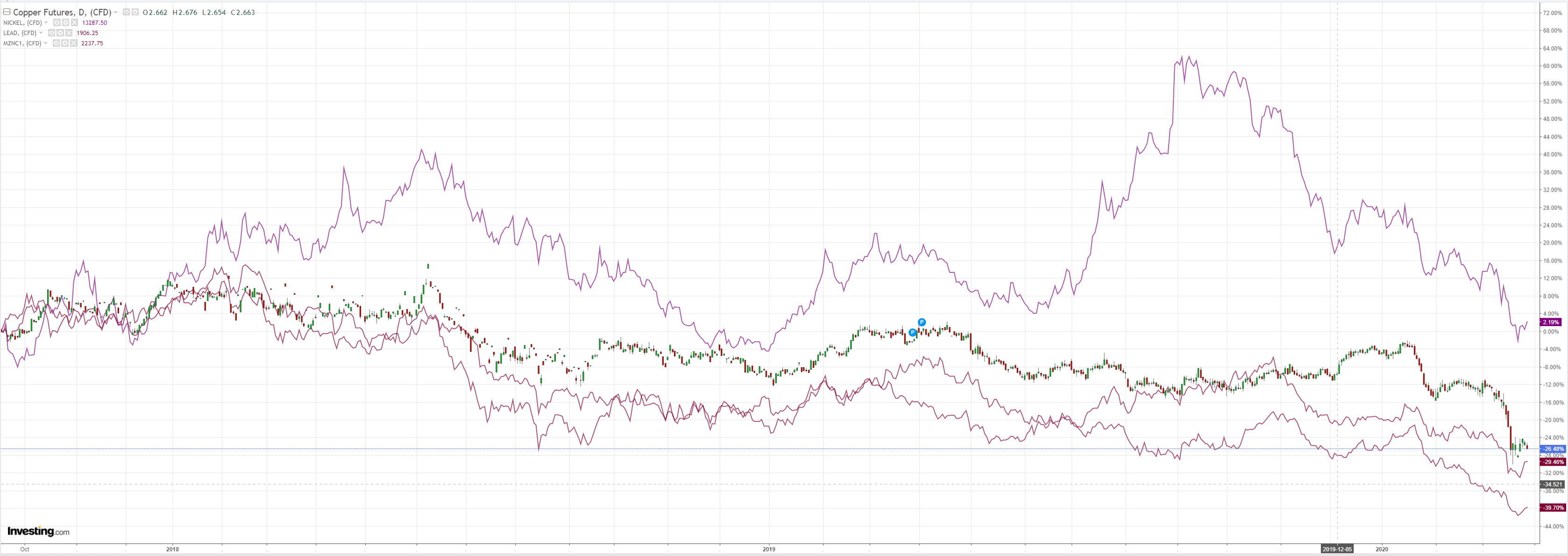

Dirt did better:

Miners did not:

Advertisement

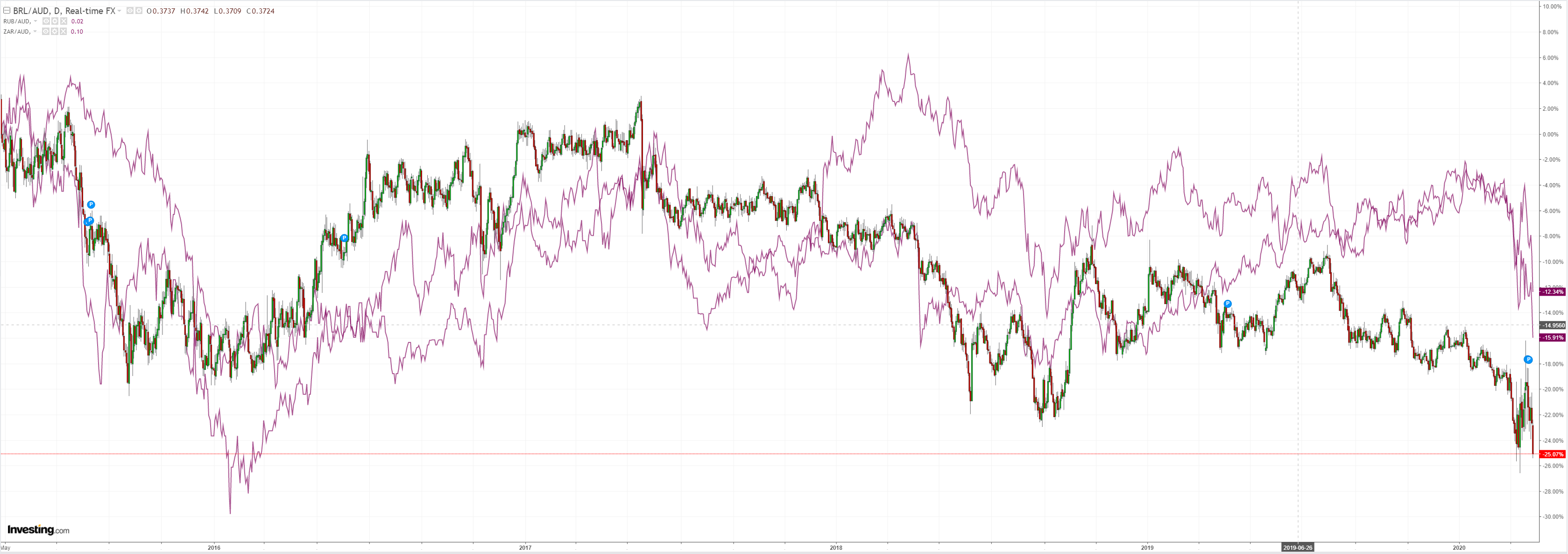

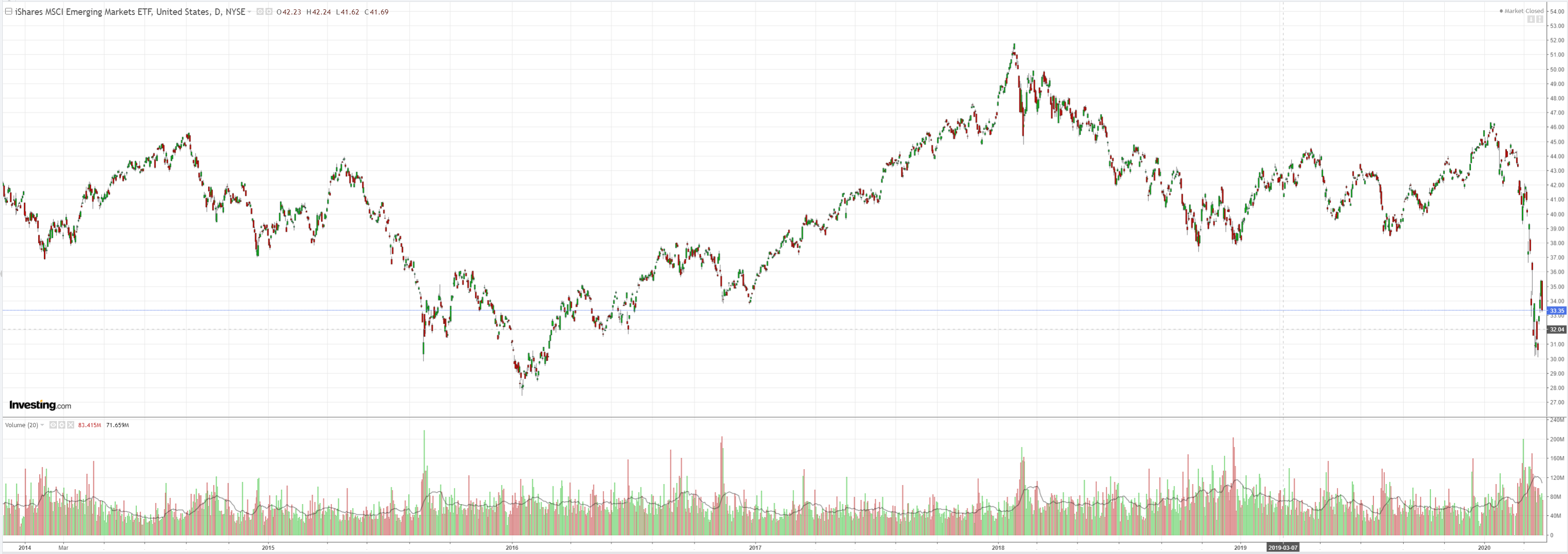

Nor EM stocks:

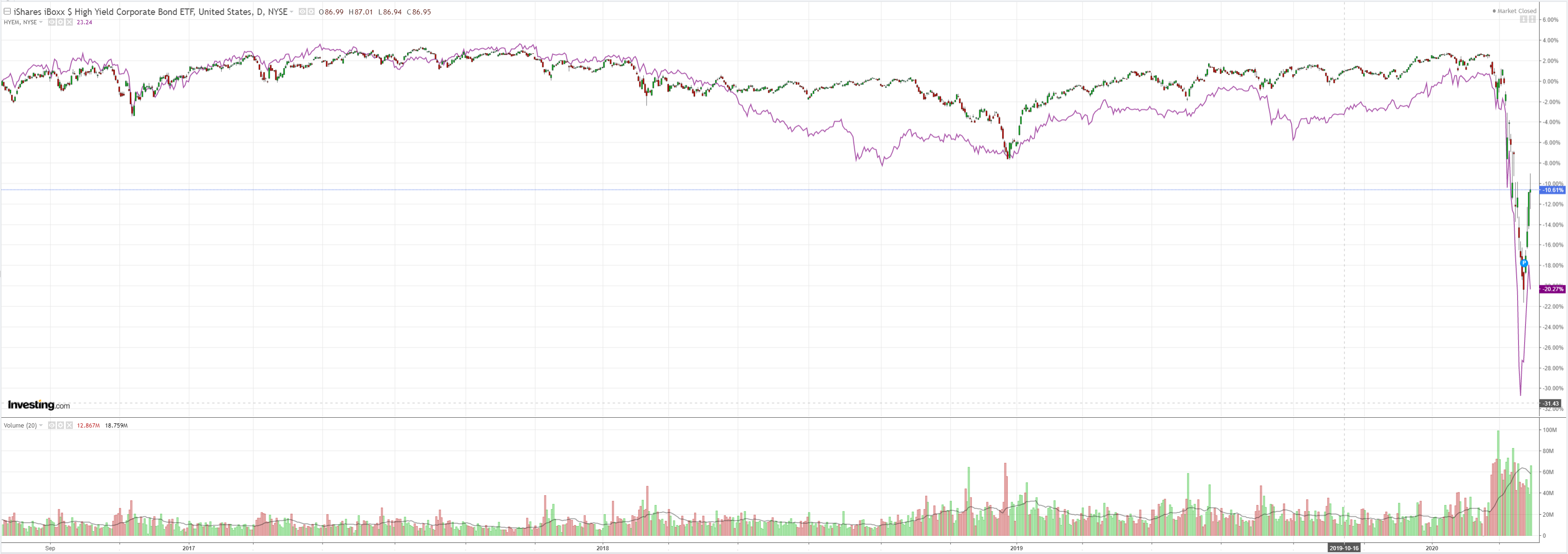

US junk flew, EM fell:

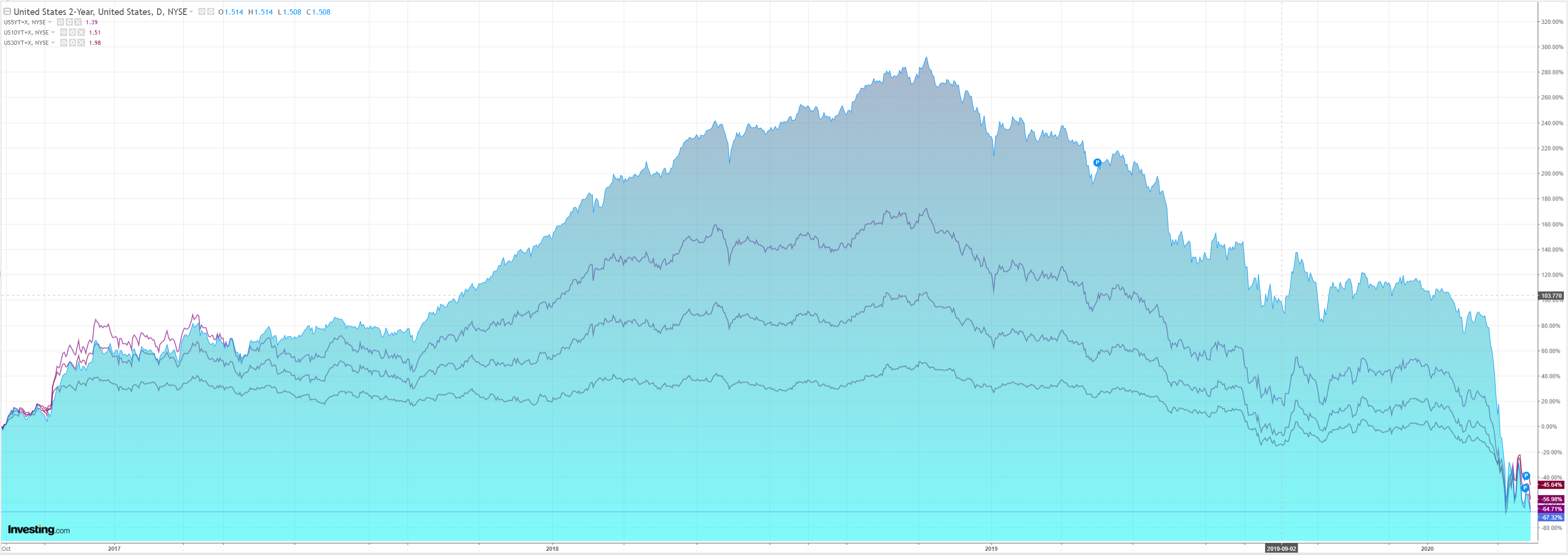

Bonds were uber-bid:

Advertisement

But stocks also flamed out:

The virus is still out of control in the US. I suspect that that is about to become the only story that matters for markets. DXY should turn higher as safe haven with that disastrous backdrop developing. Doubly so given large swathes of Europe are descending into death zones. We shall see.

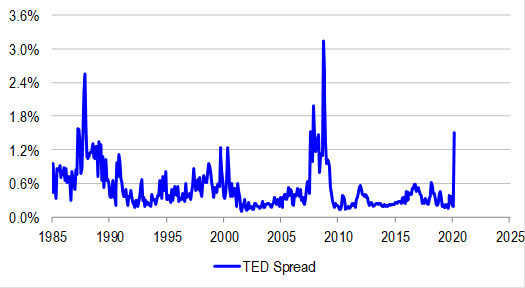

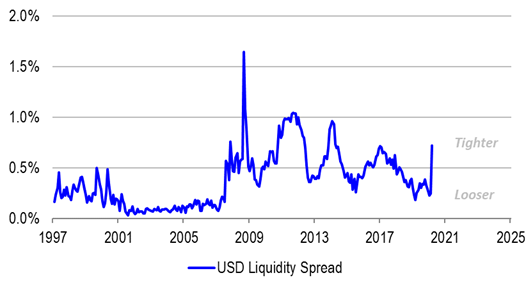

If not, markets are now also ringing the bell for the next phase of the crisis that, again, should be DXY bullish. Our old GFC friends – the TED spread and LIBOR-OIS – are back. As banks brace for the approaching tsunami of bad loans they are losing faith in one another and counter-party risk is booming. Via Damian Boey at Credit Suisse:

Advertisement

Our proprietary USD shortage indicator takes into account trade and credit indicators. There is a shortage in offshore markets when:

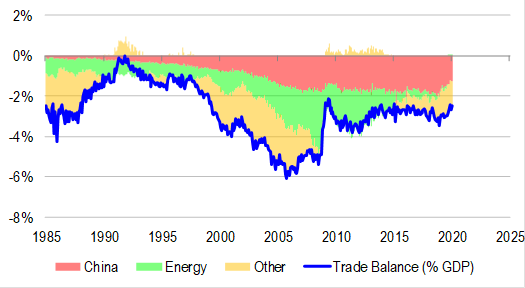

The US trade deficit is expected to get smaller, based on mean reversion to fundamentals such as US domestic saving, and the (inverted) trade-weighted USD exchange rate.

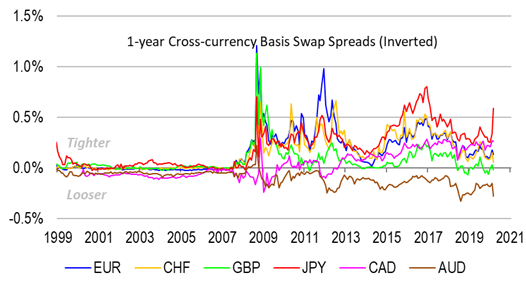

Cross currency basis swap spreads are very wide (or negative).

Interbank credit or liquidity spreads are very wide.

Mathematically, our USD shortage indicator is the sum of the expected change in US trade balance (as a share of GDP), and our aggregate measure of USD liquidity spreads.

Recently the indicator has moved into shortage territory, because spreads have widened. But interestingly, it has not hit crisis levels, in part because the US trade deficit has started to run below levels dictated by fundamentals.

Things could always change of course. A rise in US household saving rates could easily correspond with de-leveraging pressure in the US economy, meaning that it is hard for everyone to get USDs, because the US economy is not creating enough credit. However, there are offsets. For one, the US government is running larger deficits to create money where the private sector cannot. Secondly, a stronger USD actually makes imports more competitive, causing the US trade deficit to widen. The USD works as an automatic stabilizer in this regard.

If the USD shortage in aggregate is not terribly large, then where exactly is the stress that everyone is talking about?

We note that ever since the Fed has re-opened foreign exchange (FX) swap lines and extended them to non-G5 central banks, cross-currency basis swap spreads have narrowed in most jurisdictions. But they have remained quite wide in Japan. And FX swap lines have not been opened to everyone. So in China we have not been able to get a read on the cost of USD funding, while in smaller Asian economies, spreads have remained at very wide levels.

Secondly, even if stress is not apparent in FX swap markets, it is apparent in interbank markets. Eurodollar, and LIBOR-OIS spreads have lifted to the 150bps mark, a very wide level in history. It seems that banks do not seem to trust each other enough to want to clear transactions, despite the raft of Fed measures that have been put in place! Such has been the extent of the shock and uncertainty for the financial sector from shutdowns.

How far the AUD wild thing can rip in this environment is anybody’s guess but I still think we are going a lot lower in due course.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.