DXY was up overnight:

The Australian dollar was roughly stable as the rocket flamed out:

But surged against EMs:

Gold yawn:

Oil is worthless:

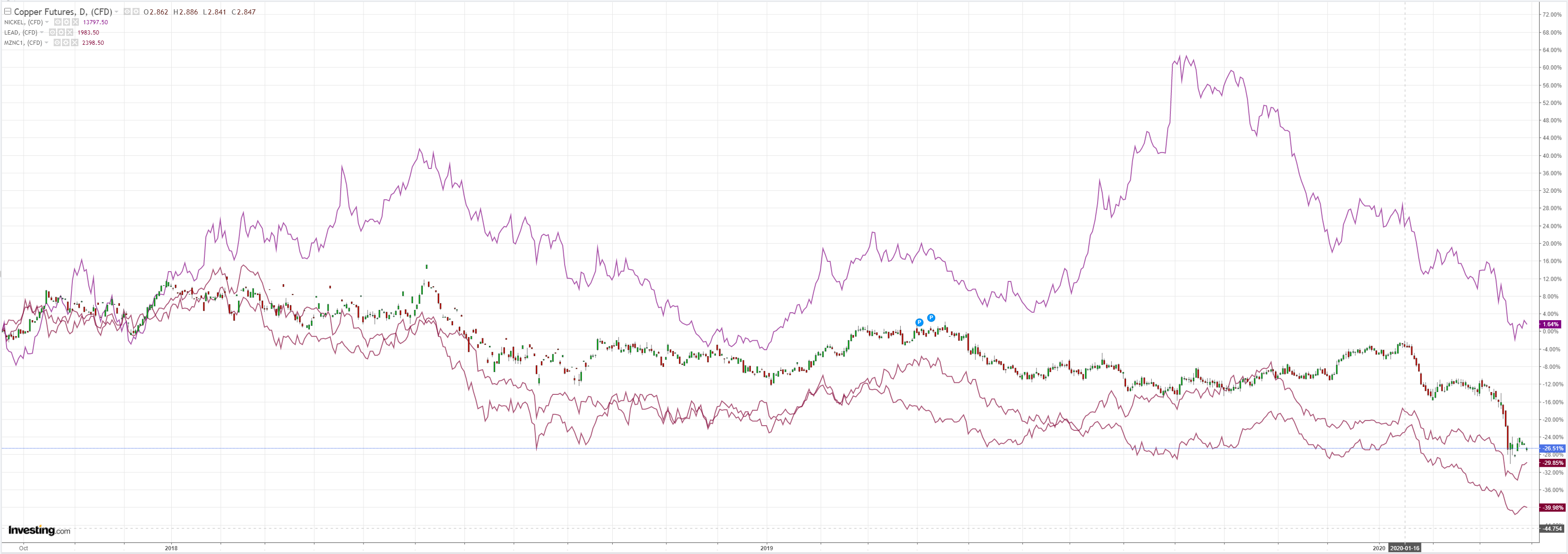

Which does not bode well for dirt:

Miners were OK:

EM stocks too:

US junk rallied. Not EM:

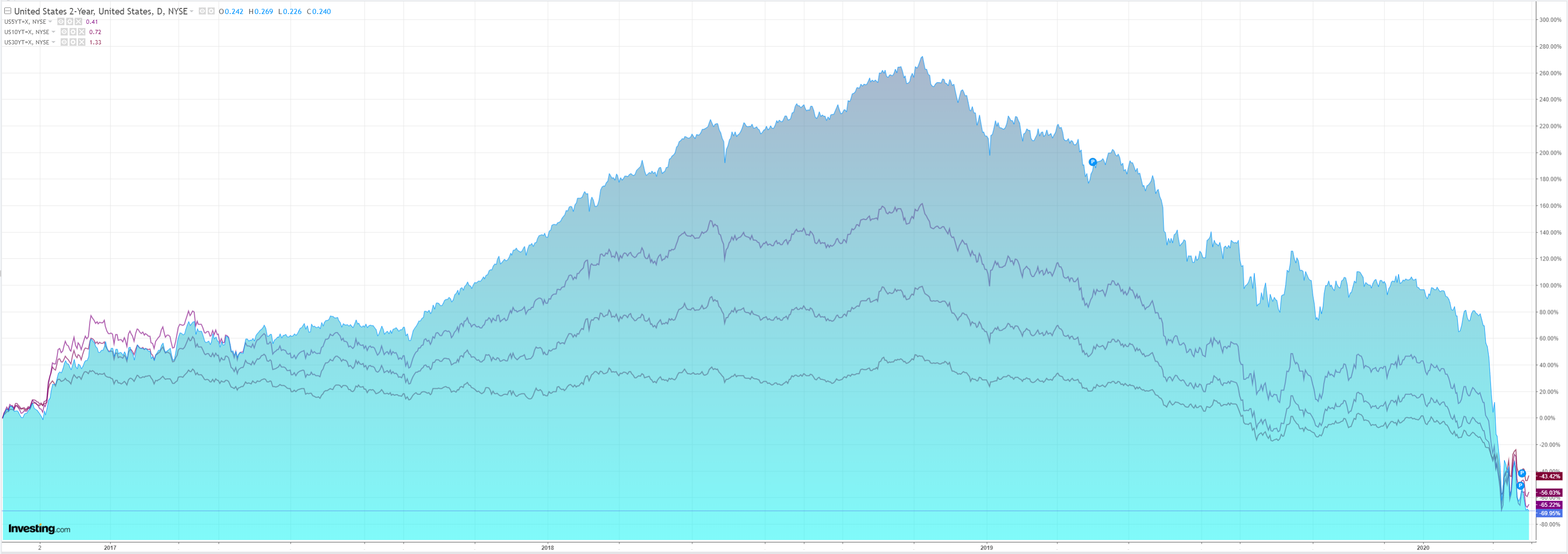

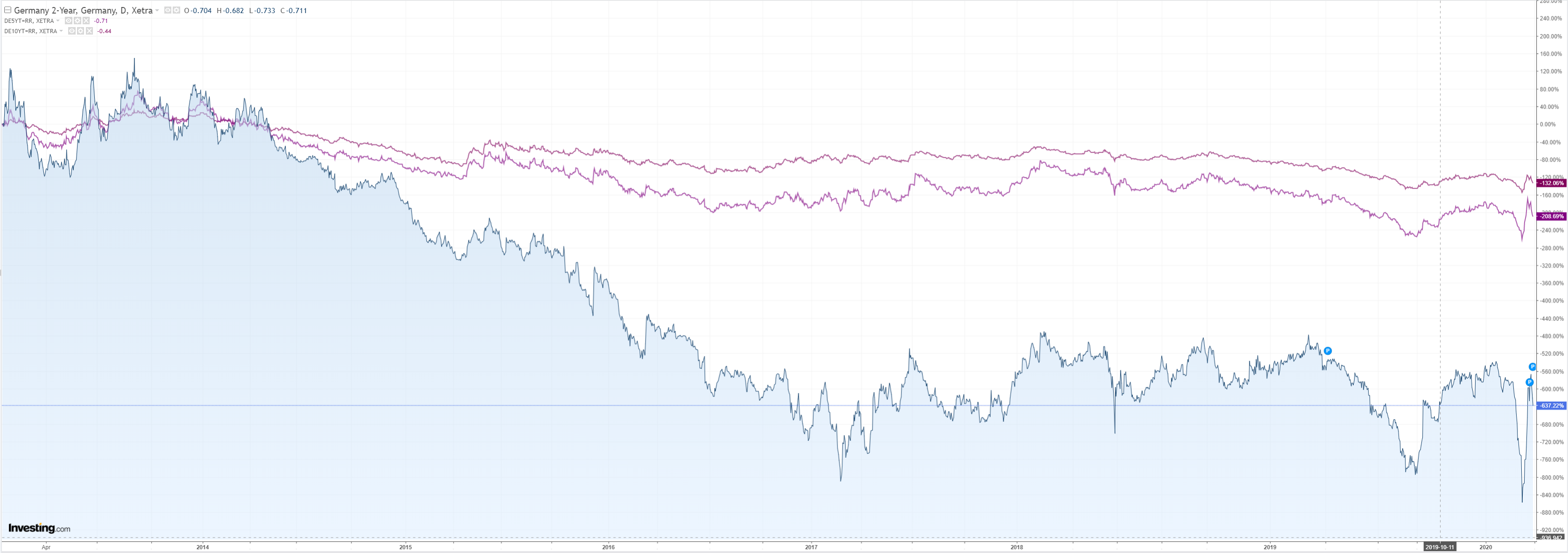

Bonds were mixed:

Stocks tacked on gains:

Westpac has the wrap:

Event Wrap

Coronavirus update: Latest data from John Hopkins University indicates 59,400 new confirmed cases on 29 March, vs 67,400 the previous day.

The Bank of England announced enhanced liquidity provisions, extending its Contingent Term Repo Facility through.

Eurozone business and economic confidence for March fell sharply, but less than estimated. Economic confidence slipped to 94.5 (est. 94.5) from 103.4. Although consistent with contraction, the full scale of the COVID-19 shock is still to hit the surveys.

In the US, Dallas Fed March manufacturing survey plunged to a -70 record low (the GFC low was -59.9) as activity sharply contracted and outlooks worsened. The estimate was -10, prior +1.2.

Event Outlook

In Australia, Westpac expects February private sector credit to grow by 0.3%. A housing upswing and business credit volatility has provided support in the new year, but the underlying trend remains weak.

Turning to New Zealand, Westpac expects that building permits increased by a modest 4.0% in February. Strength is broad based, and this should see annual issuance running near record levels. However, the release predates the coronavirus lockdown, and there is considerable uncertainty going forward. The March ANZ business confidence survey will follow, and preliminary estimates have indicated that a sharp fall is likely.

In China, the market will closely watch the March manufacturing and non-manufacturing PMIs. Both are expected to rebound substantially as conditions gradually revert to their normal trend.

Euro Area March CPI is due, and expected to print at a soft 0.8%yr. However, inflation is a secondary consideration in the face of a looming recession and considerable economic instability.

In the UK, the GfK consumer sentiment index is expected to pull back to -13 in March as the impact of the virus and lockdown measures weigh on the consumer.

Finally, in the US, the January S&P/CS home price index is expected to appreciate by 0.40%; however, as unemployment rises, prices are likely to decline. The March Chicago PMI will follow, and the market expects a material decline to 44.0. To round out the day, the March consumer confidence index is expected to echo previous survey data and deteriorate to 115.0.

So, a decent bear market rally is underway. How far it gets is anybody’s guess. It will have to push through a dramatically increasing US death rate which will be difficult.

It is still most likely only a bear market rally. We’re through the initial market shock and the major policy response. Next up comes the economic hit, demolition of earnings, mass bankruptcies and banking crisis. All on remarkable fast forward.

The market is still hopeful of a v-shaped revovery. Yet in the global test case, China, no such thing is happening. And it owns its banks so has no problems on that front.

Enjoy the rally while it lasts. Including for the Australian dollar.