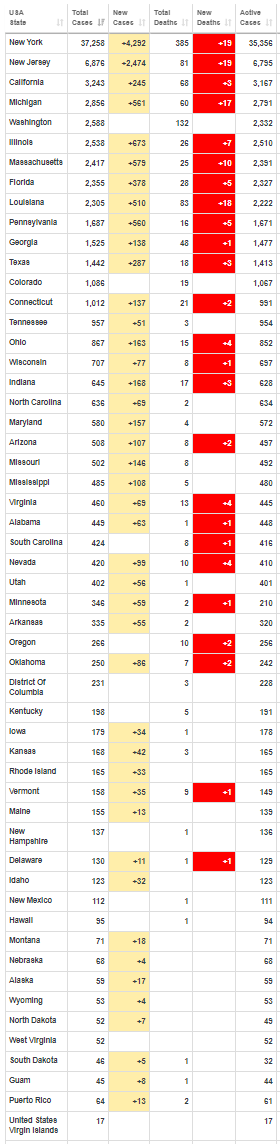

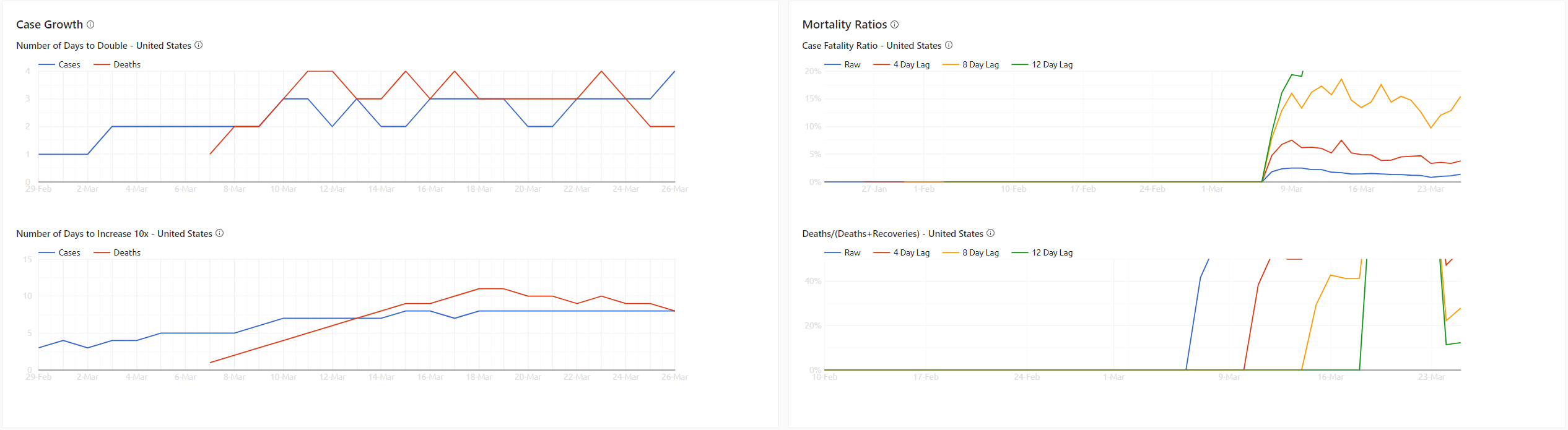

Coronavirus update: Latest WHO data, via the Situation Reports, indicates 40,700 new cases on 25 March, slightly higher than the previous day. Unofficial source Worldometer indicates 39.678 new cases on 26 March.

The U.S. Senate approved a historic $2 trillion rescue plan to respond to the economic and health crisis caused by the coronavirus pandemic, in a 96-0 vote. The House is scheduled to vote on the bill on Friday, through a remote voice vote so members need not travel to Washington.

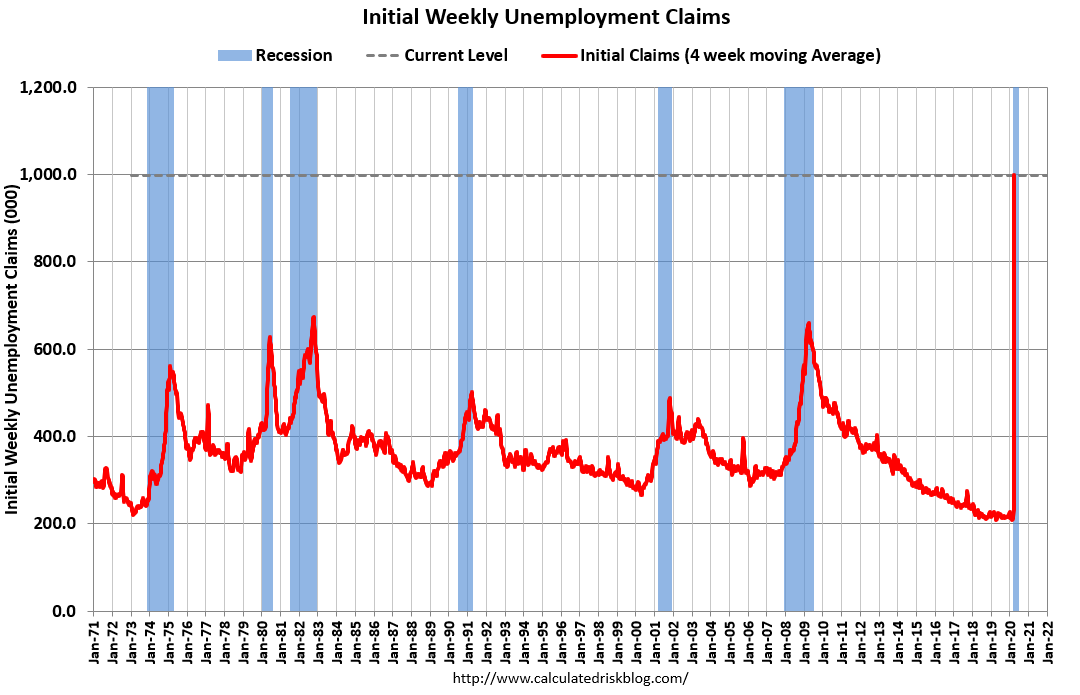

US initial jobless claims surged 3.001m to 3.283m in the week ending 21 March, setting new records for the increase and level, following the 71k climb to 282k in the prior week. For historical context, claims data starts in 1967, and the previous record increase was in July 1992 (+172k), with the all-time high level in 1982 at 695k.

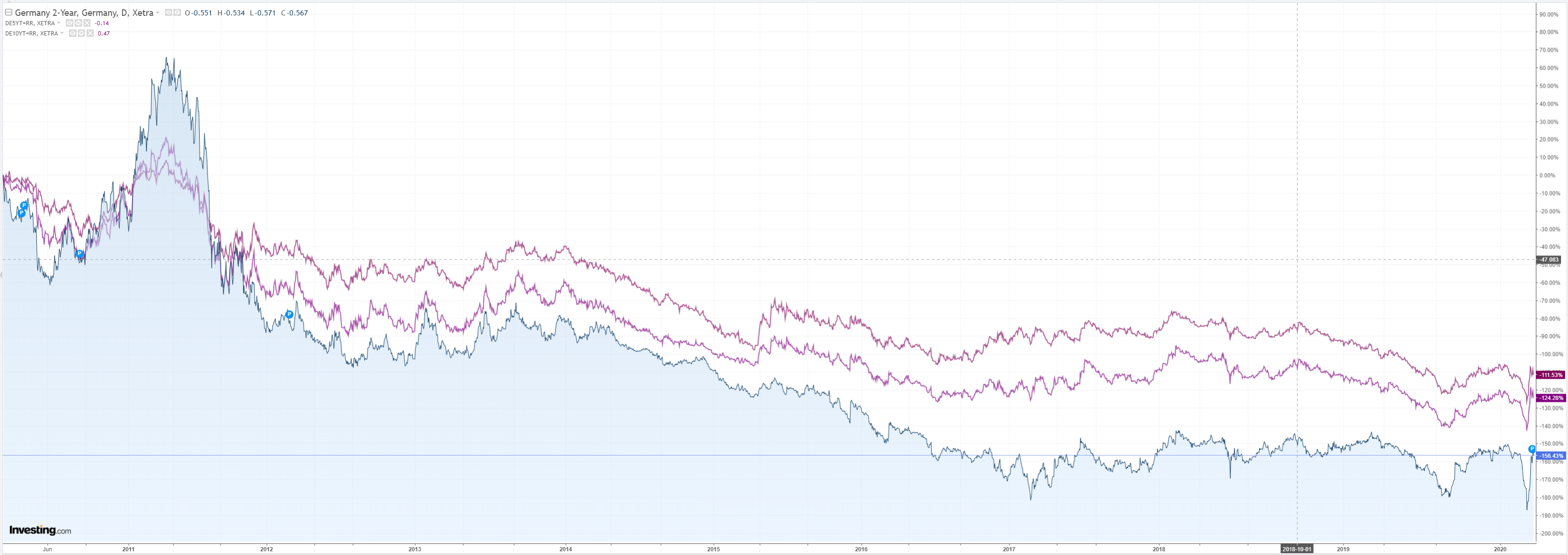

Media reports indicated the ECB favours activating its OMT program – a powerful bond-purchase tool created in 2012 to support the euro, but has never been used. It allows the ECB to buy unlimited amounts of a country’s sovereign debt.

BoE left its benchmark policy rate unchanged at 0.10%, as expected, in a unanimous vote. The asset purchase program was also left unchanged. The BoE had already moved in an emergency meeting last week, to cut rates and add additional asset purchases, but the central bank stressed that it can still expand purchases as needed.

Event Outlook

In New Zealand we have the March ANZ consumer confidence survey, expected to fall sharply in response to COVID-19 concerns.

In China, February industrial profits are due. Profits had already stabilised at a weak base before the advent of the contagion, so another soft print can be expected. The final read for the Q4 current account balance is also scheduled for release, including the full detail on trade and financial flows.

US February personal income is expected to have grown by 0.4% ahead of the impact of COVID-19. Likewise, personal spending will be subdued going forward, but is expected to have risen by 0.2% in the February read. Finally, the February corePCE deflator is expected to print at 1.7%, still below the Federal Reserve’s inflation target. The finalised Michigan Univ. consumer confidence survey should be lower.

Not that any of that matters much. We’re far beyond data now. Still here’s the DOL:

In the week ending March 21, the advance figure for seasonally adjusted initial claims was 3,283,000, an increase of 3,001,000 from the previous week’s revised level. This marks the highest level of seasonally adjusted initial claims in the history of the seasonally adjusted series. The previous high was 695,000 in October of 1982. The previous week’s level was revised up by 1,000 from 281,000 to 282,000. The 4-week moving average was 998,250, an increase of 765,750 from the previous week’s revised average. The previous week’s average was revised up by 250 from 232,250 to 232,500.

Advertisement

This is a classic bear market rally. Way overbid following being way oversold. It’ll run until it’s over. My best bet is not very long given the US is headed directly into virus disaster:

At terrifying speed:

Advertisement

While the bear market rally runs the Australian dollar runs with it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.