DXY softed a little last night:

The Australian dollar firmed:

Gold jumped:

Oil too:

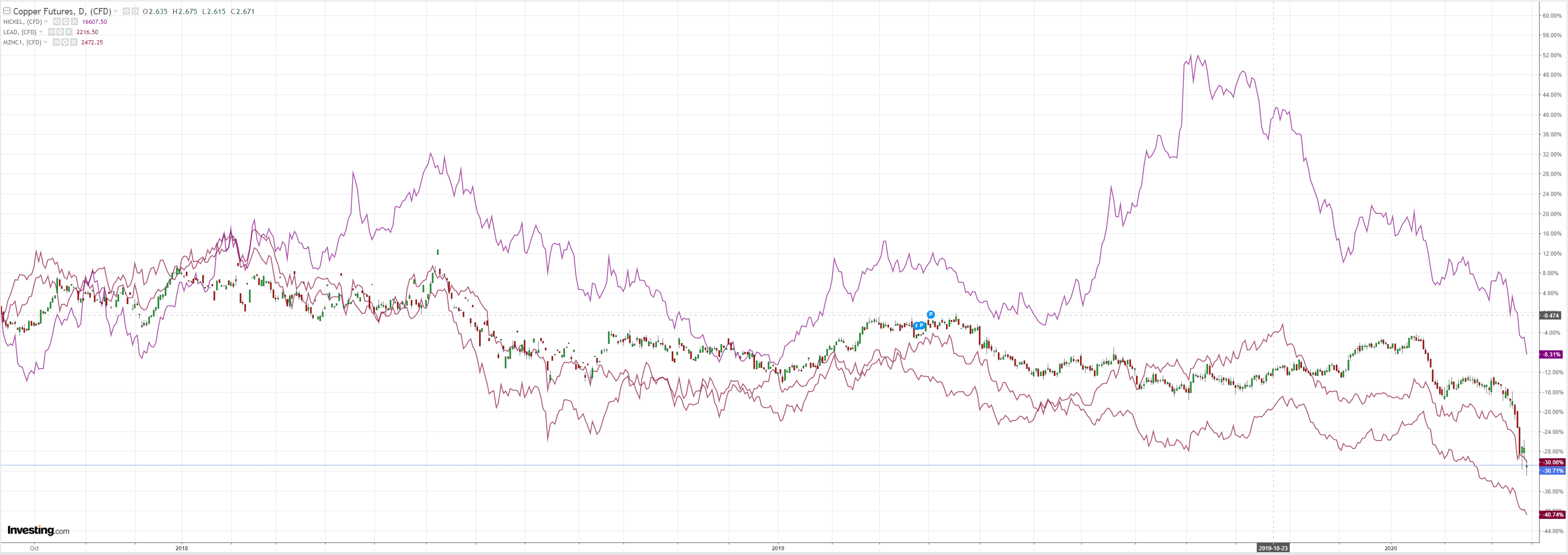

Not metals:

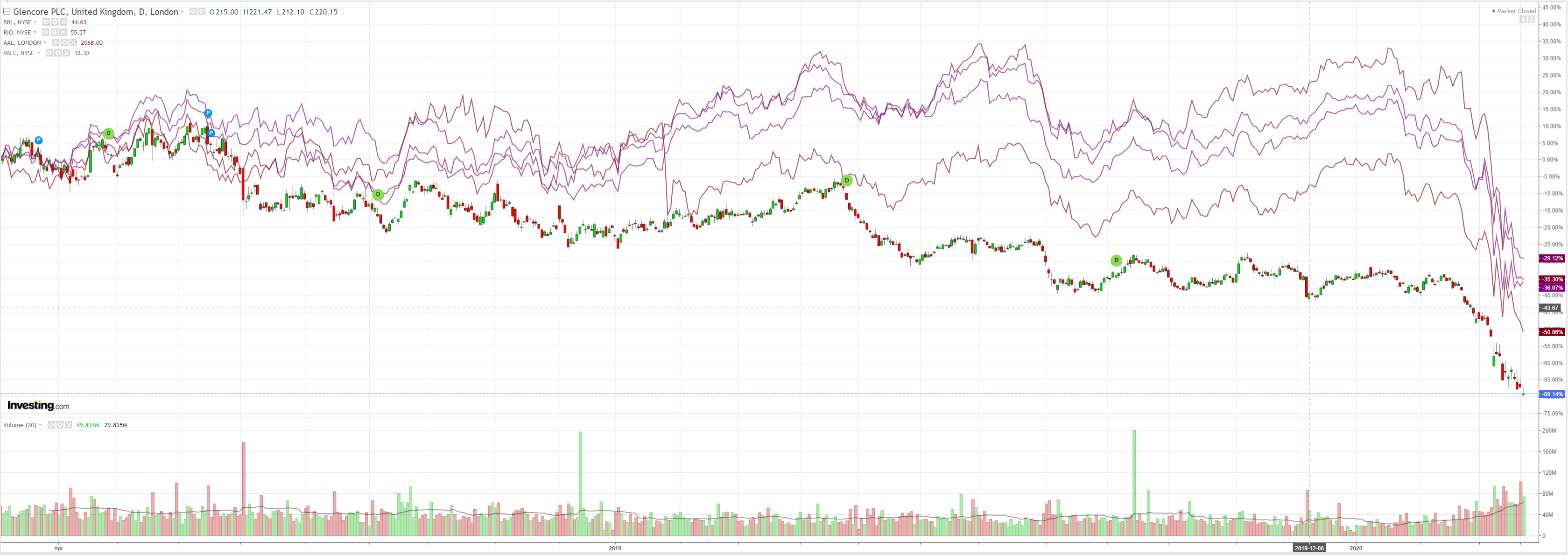

Nor miners:

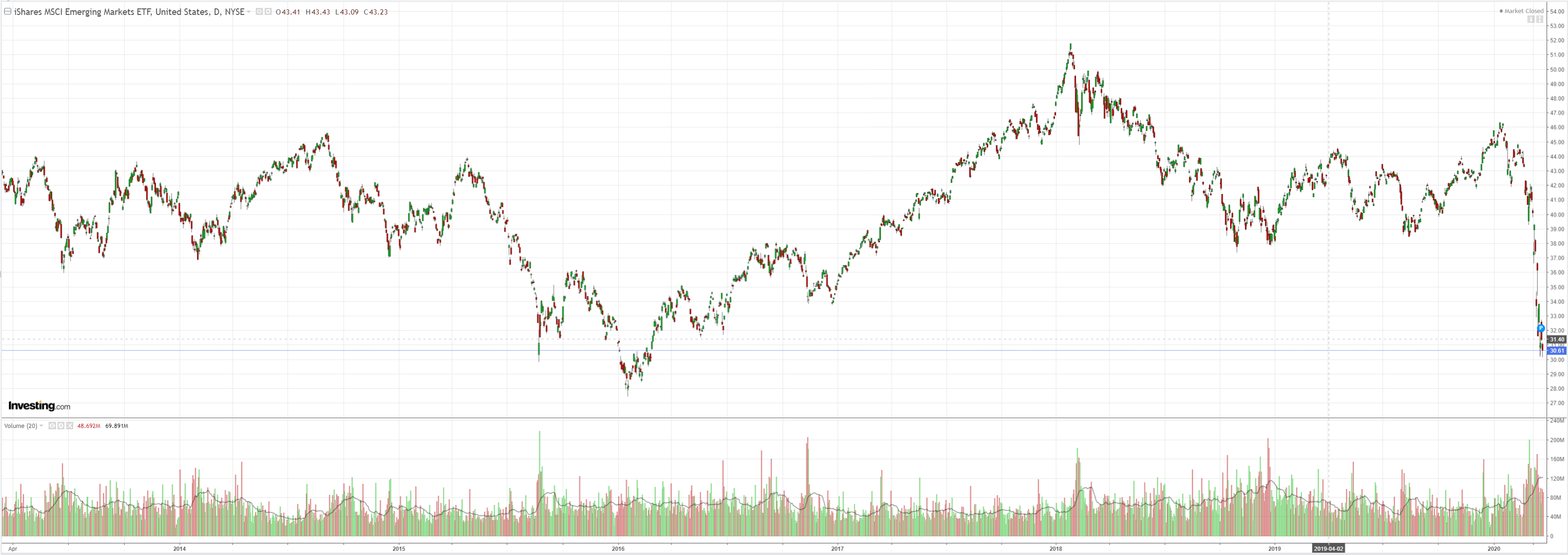

Or EM stocks:

Junk lifted a little:

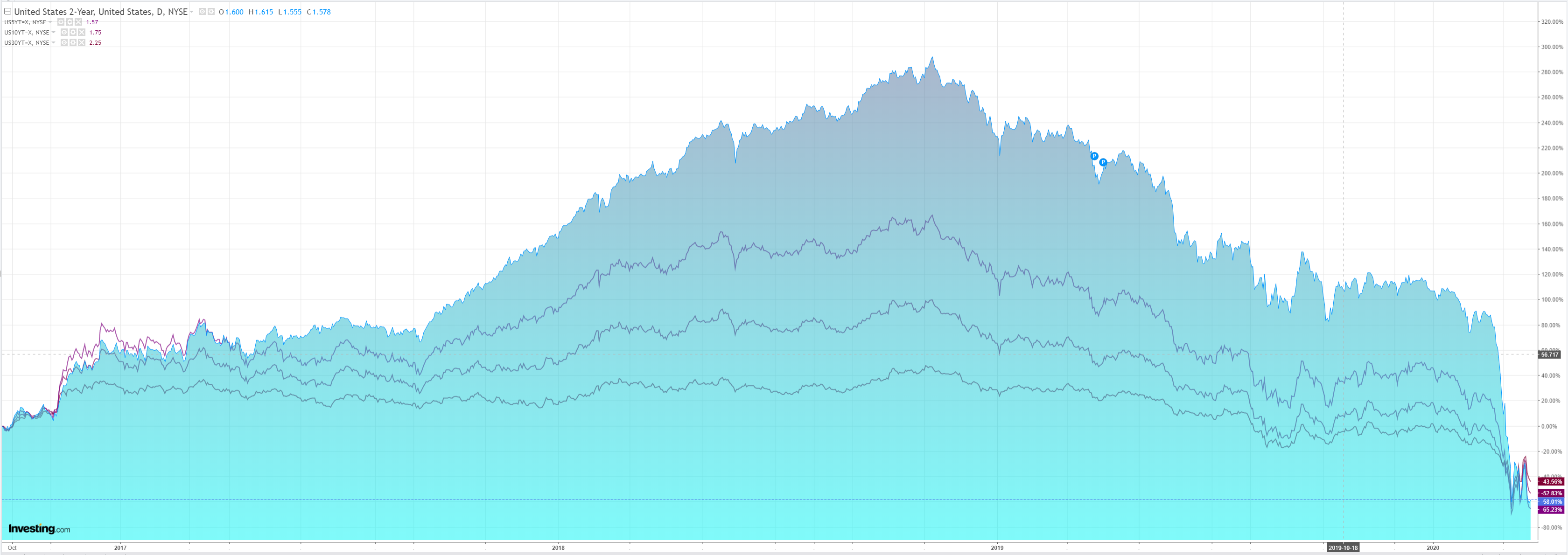

As did bonds:

Stocks fell anyway:

Westpac has the wrap:

Event Wrap

Coronavirus update: Latest WHO data, via the Situation Reports, shows 292,142 cases confirmed as at 22 March, with 26,069 new cases. The daily increase in cases continues to rise, the largest increases coming from Iran, Italy, Spain, France, Germany, Switzerland, USA and UK. Unofficial sources such as Worldometer show cases confirmed to date total 372,253 as at 23 March, with 34,823 new cases.

The US Federal Reserve announced an unprecedented set of initiatives designed at supporting the interest rate markets and businesses, including open-ended purchases of treasury, agency and mortgage backed securities, a new USD300bn fund to provide consumer and business credit flow , two facilities for large employers, support for the corporate bond market, Term Asset-Backed Security Loans to support consumer and business credit, and business lending programmes to support SMEs.

Regarding US Government rescue initiatives, disputes between Democrats and Republicans persist, the parties presenting opposing bills.

Event Outlook

Several preliminary readings of the March Markit PMIs are due over the day. This includes the manufacturing and services PMIs for Japan, the Euro Area, Germany, the UK and the US. The market will watch these indices closely as a barometer for conditions amidst the pandemic; sharp contractions are anticipated across the board.

US February new home sales are now dated, but expected to print at 750k. This is ahead of a likely pullback in demand as COVID-19 accelerates. March Richmond Fed index is expected to fall to -10 as US industry comes under significant pressure from the contagion.

The Fed finally reached to place the world needs it to be:

Federal Reserve announces extensive new measures to support the economy

The Federal Reserve is committed to using its full range of tools to support households, businesses, and the U.S. economy overall in this challenging time. The coronavirus pandemic is causing tremendous hardship across the United States and around the world. Our nation’s first priority is to care for those afflicted and to limit the further spread of the virus. While great uncertainty remains, it has become clear that our economy will face severe disruptions. Aggressive efforts must be taken across the public and private sectors to limit the losses to jobs and incomes and to promote a swift recovery once the disruptions abate.

The Federal Reserve’s role is guided by its mandate from Congress to promote maximum employment and stable prices, along with its responsibilities to promote the stability of the financial system. In support of these goals, the Federal Reserve is using its full range of authorities to provide powerful support for the flow of credit to American families and businesses. These actions include:

- Support for critical market functioning. The Federal Open Market Committee (FOMC) will purchase Treasury securities and agency mortgage-backed securities in the amounts needed to support smooth market functioning and effective transmission of monetary policy to broader financial conditions and the economy.

- The FOMC had previously announced it would purchase at least $500 billion of Treasury securities and at least $200 billion of mortgage-backed securities. In addition, the FOMC will include purchases of agency commercial mortgage-backed securities in its agency mortgage-backed security purchases.

- Supporting the flow of credit to employers, consumers, and businesses by establishing new programs that, taken together, will provide up to $300 billion in new financing. The Department of the Treasury, using the Exchange Stabilization Fund (ESF), will provide $30 billion in equity to these facilities.

- Establishment of two facilities to support credit to large employers – the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.

- Establishment of a third facility, the Term Asset-Backed Securities Loan Facility (TALF), to support the flow of credit to consumers and businesses. The TALF will enable the issuance of asset-backed securities (ABS) backed by student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration (SBA), and certain other assets.

- Facilitating the flow of credit to municipalities by expanding the Money Market Mutual Fund Liquidity Facility (MMLF) to include a wider range of securities, including municipal variable rate demand notes (VRDNs) and bank certificates of deposit.

- Facilitating the flow of credit to municipalities by expanding the Commercial Paper Funding Facility (CPFF) to include high-quality, tax-exempt commercial paper as eligible securities. In addition, the pricing of the facility has been reduced.

In addition to the steps above, the Federal Reserve expects to announce soon the establishment of a Main Street Business Lending Program to support lending to eligible small-and-medium sized businesses, complementing efforts by the SBA.

The PMCCF will allow companies access to credit so that they are better able to maintain business operations and capacity during the period of dislocations related to the pandemic. This facility is open to investment grade companies and will provide bridge financing of four years. Borrowers may elect to defer interest and principal payments during the first six months of the loan, extendable at the Federal Reserve’s discretion, in order to have additional cash on hand that can be used to pay employees and suppliers. The Federal Reserve will finance a special purpose vehicle (SPV) to make loans from the PMCCF to companies. The Treasury, using the ESF, will make an equity investment in the SPV.

The SMCCF will purchase in the secondary market corporate bonds issued by investment grade U.S. companies and U.S.-listed exchange-traded funds whose investment objective is to provide broad exposure to the market for U.S. investment grade corporate bonds. Treasury, using the ESF, will make an equity investment in the SPV established by the Federal Reserve for this facility.

Under the TALF, the Federal Reserve will lend on a non-recourse basis to holders of certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. The Federal Reserve will lend an amount equal to the market value of the ABS less a haircut and will be secured at all times by the ABS. Treasury, using the ESF, will also make an equity investment in the SPV established by the Federal Reserve for this facility. The TALF, PMCCF and SMCCF are established by the Federal Reserve under the authority of Section 13(3) of the Federal Reserve Act, with approval of the Treasury Secretary.

These actions augment the measures taken by the Federal Reserve over the past week to support the flow of credit to households and businesses. These include:

- The establishment of the CPFF, the MMLF, and the Primary Dealer Credit Facility;

- The expansion of central bank liquidity swap lines;

- Steps to enhance the availability and ease terms for borrowing at the discount window;

- The elimination of reserve requirements;

- Guidance encouraging banks to be flexible with customers experiencing financial challenges related to the coronavirus and to utilize their liquidity and capital buffers in doing so;

- Statements encouraging the use of daylight credit at the Federal Reserve.

Taken together, these actions will provide support to a wide range of markets and institutions, thereby supporting the flow of credit in the economy.

The Federal Reserve will continue to use it full range of tools to support the flow of credit to households and businesses and thereby promote its maximum employment and price stability goals.

It is now lender and buyer of last resort to ALL credit.

This is not the end of the crisis. Ahead lies the decimation of the US by the virus. A more severe shutdown there and in Europe. Mass corporate and personal bankruptices. And, finally, mass bank nationalisations.

But it is the end of the beginning. Now the Fed can backstop it all.

Normally we would expect risk assets and the Australian dollar to get a good run from this but the crisis is moving so fast, and the economic damage is so severe and steep, that I do not think that it will get far before heading lower.