DXY took a breather last night as markets were hit by the Fed bazooka:

The Australian dollar plunged on anyway:

Gold is liquidating but so far the damage is minimal:

Oil is going to $10:

Base metals joined the rout:

Miners fell but not as much as many:

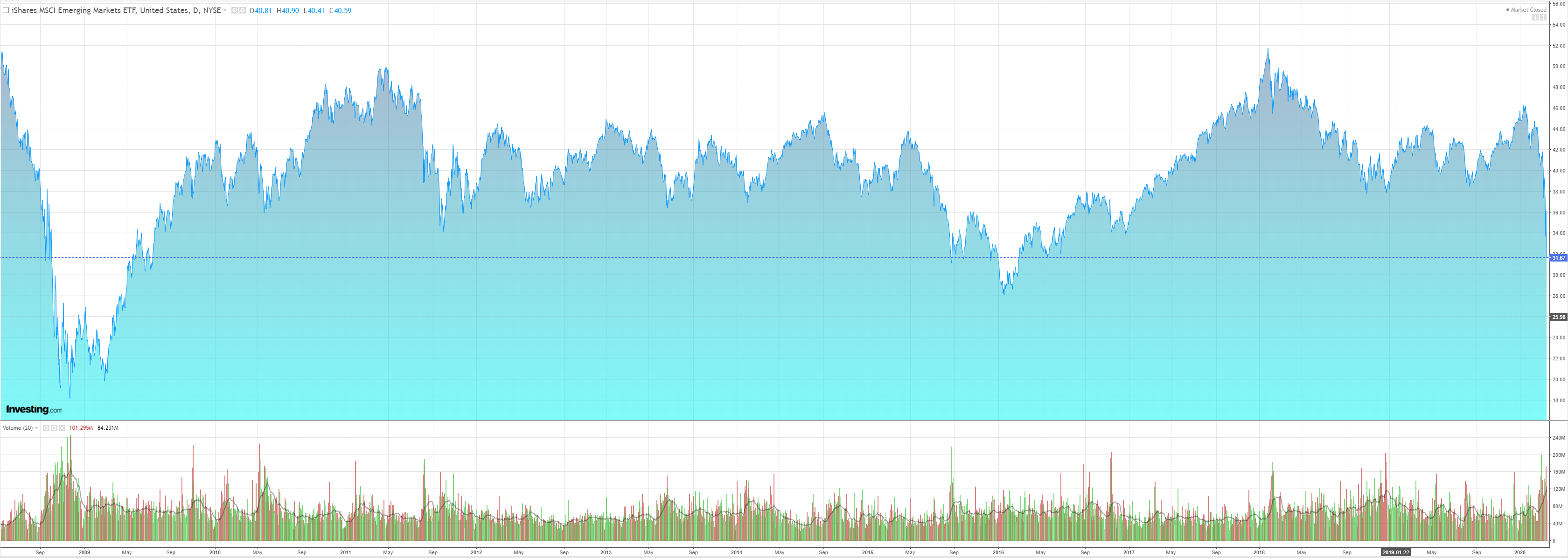

EM stocks broke:

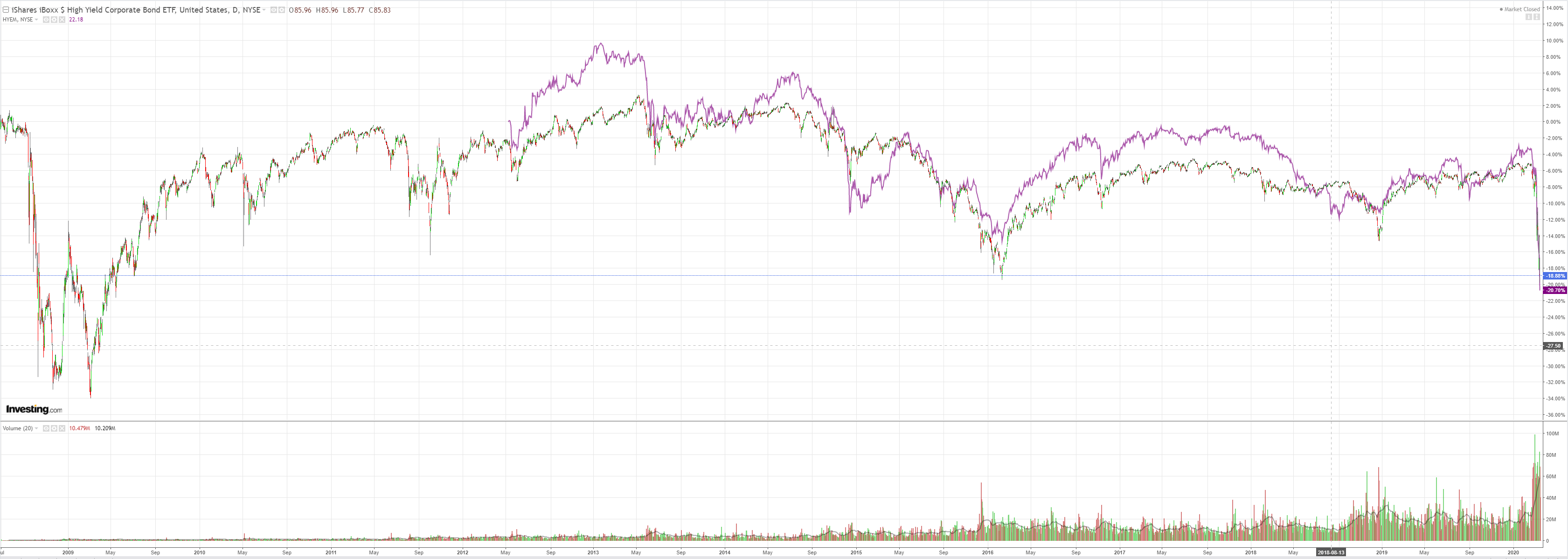

Along with junk:

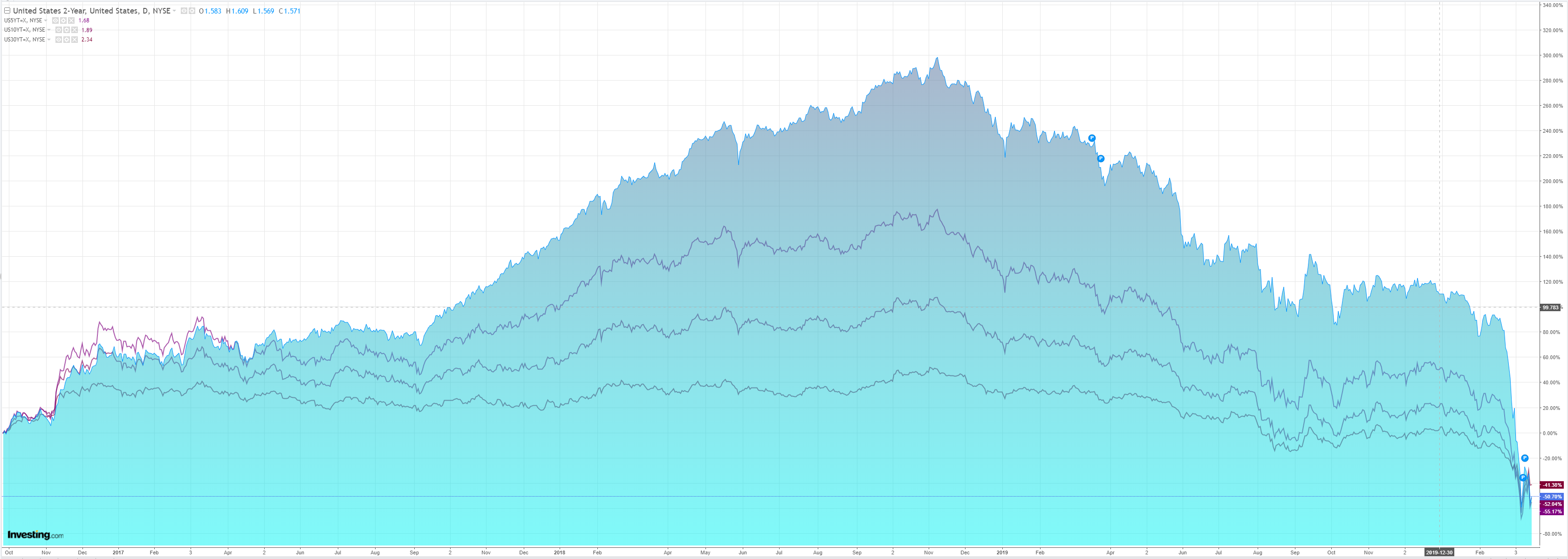

Treasuries held on the Fed bazooka:

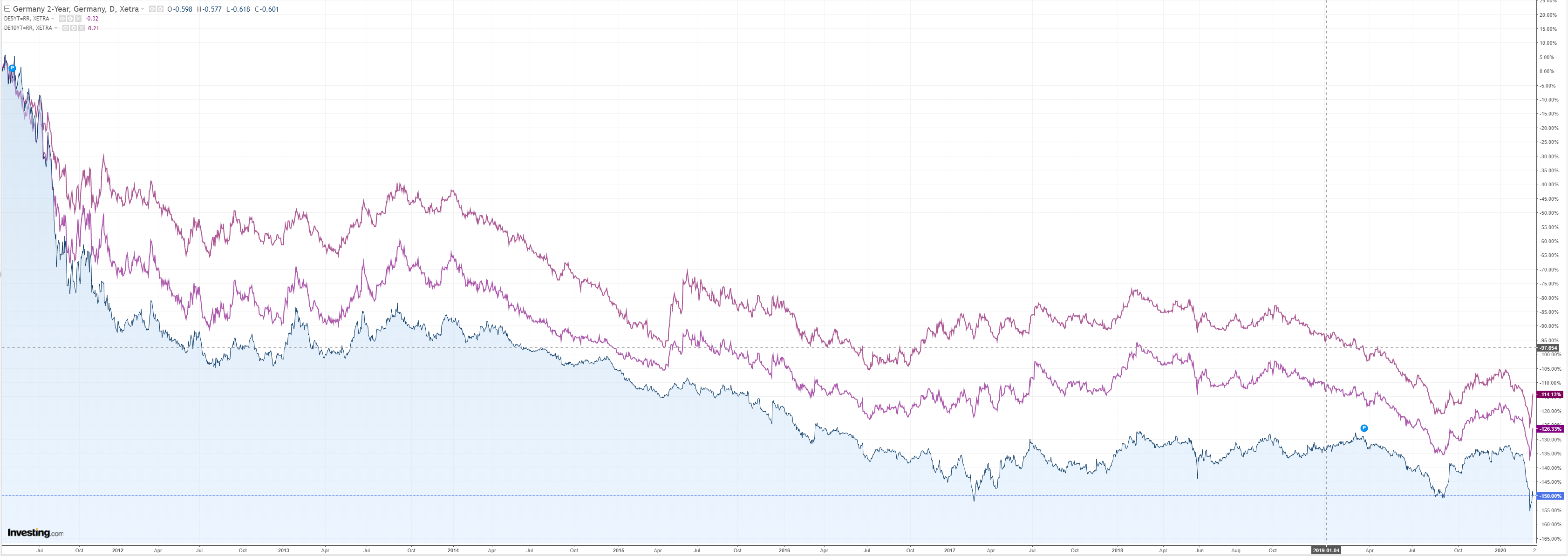

But bunds sold:

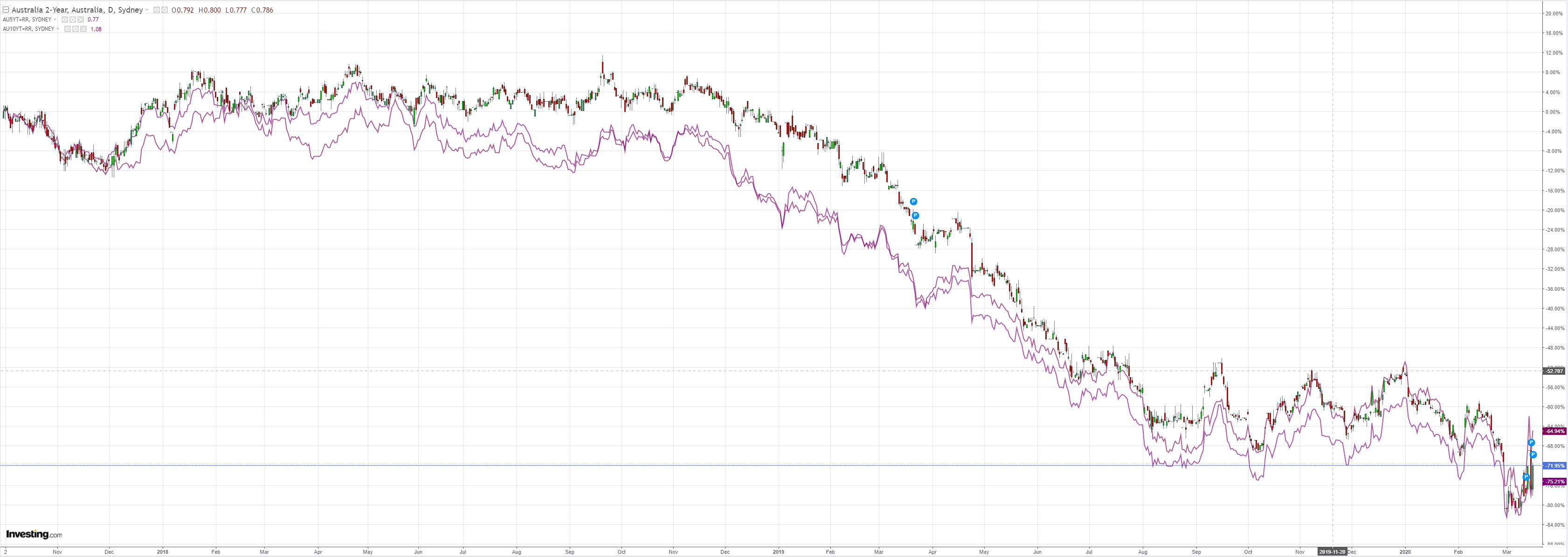

And the market is going to test the RBA version, as expected:

Stocks OMG, daily moves of 10% plus now:

Westpac has the wrap:

Event Wrap

Coronavirus update: Latest WHO data, via the Situation Reports, shows 153,517 cases confirmed as at 15 March, with 27 new cases in China and 10955 new cases outside China. The latter continues to accelerate, the largest increase in cases coming from Italy, Iran, Spain, France and Germany. Unofficial sources such as Worldometer show cases confirmed to date total 179,700 as at 16 March.

G-7 released a joint statement on their “whatever is necessary” measures to support global trade, investment and jobs whilst coordinating health research to combat coronavirus.

IMF declared a USD1trn funding/loan facility was available to assist in fighting COVID-19. They also underscored the need for synchronised fiscal stimulus is growing “by the hour”.In the first US survey since COVID-19 started to accelerate, the Empire NY Fed Survey for March fell a record 34.4 points to -21.5 (prior +12.9). New orders fell to -9.3 from +22.1 and employees fell to -1.5 from +6.6.

Event Outlook

In Australia, the Q1 AusChamber-Westpac business survey is due. This will provide a timely update on conditions in the manufacturing sector amidst a disruptive start to the new year and a continuing downturn in the homebuilding sector. Following this, the RBA minutes for the March meeting will be published, providing additional colour around COVID-19 risks and how policy can respond.

Singapore’s February non-oil domestic exports are expected to print at a weak -7.1%yr as shutdowns across the region weigh on trade.

Turning to Europe, the market will be watching the March ZEW survey of expectations to gauge the shock from the virus.

In the UK, the Jan ILO unemployment rate is expected to hold steady at 3.8%. The labour market has remained strong in the UK despite growing uncertainties. This read predates the spread of COVID-19 in Europe.

Several releases are due in the US. The first will be February retail sales, which Westpac expects will increase by 0.3% – COVID-19 disruption in the latter part of the month should be offset by earlier precautionary spending. February industrial production will follow; the market expects this will grow by 0.4% ahead of COVID-19’s spread. January JOLTS job openings also predate the spread of the virus, and should be broadly flat in the month. Finally, the March NAHB housing market index is also expected to hold at 74 – whilst homebuilding has strong economic support, the virus presents a considerable risk.

The Australian dollar did OK last night considering the broader liquidation. The market looks ready to test the RBA’s QE commitment with Aussie spread remaing wider than elsewhere. “Show me the money” it might be called. So until then the AUD might hold up.

I hope the RBA will adopt yield curve control given it implies unlimited bond purchases. That would hit the AUD hardest and also pressure spreads the most. Which probably means they won’t do it! Jokes aside, it is the method they have mooted.

So, more downside ahead for the Australian dollar.