DXY is off and running as the great liquidation mushrooms:

The Australian dollar was destroyed to seventeen year lows:

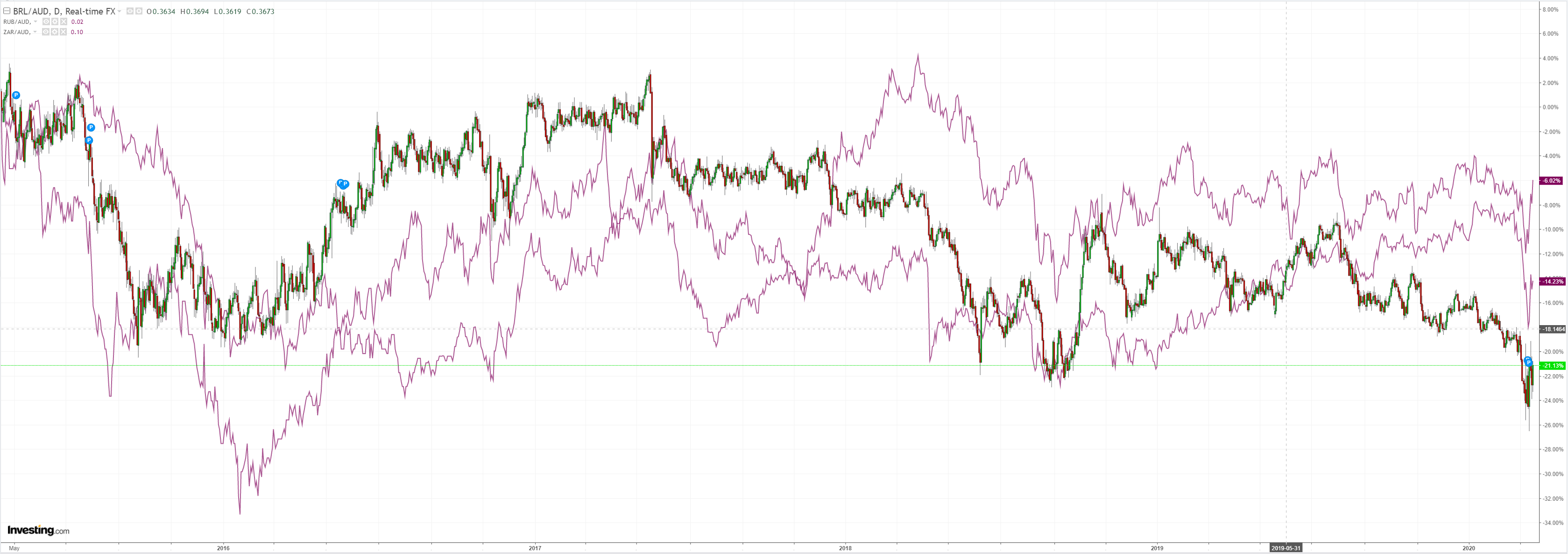

It could not even get a bid versus EMs:

Gold got a bid:

Oil is going to zero:

Base metals not far behind:

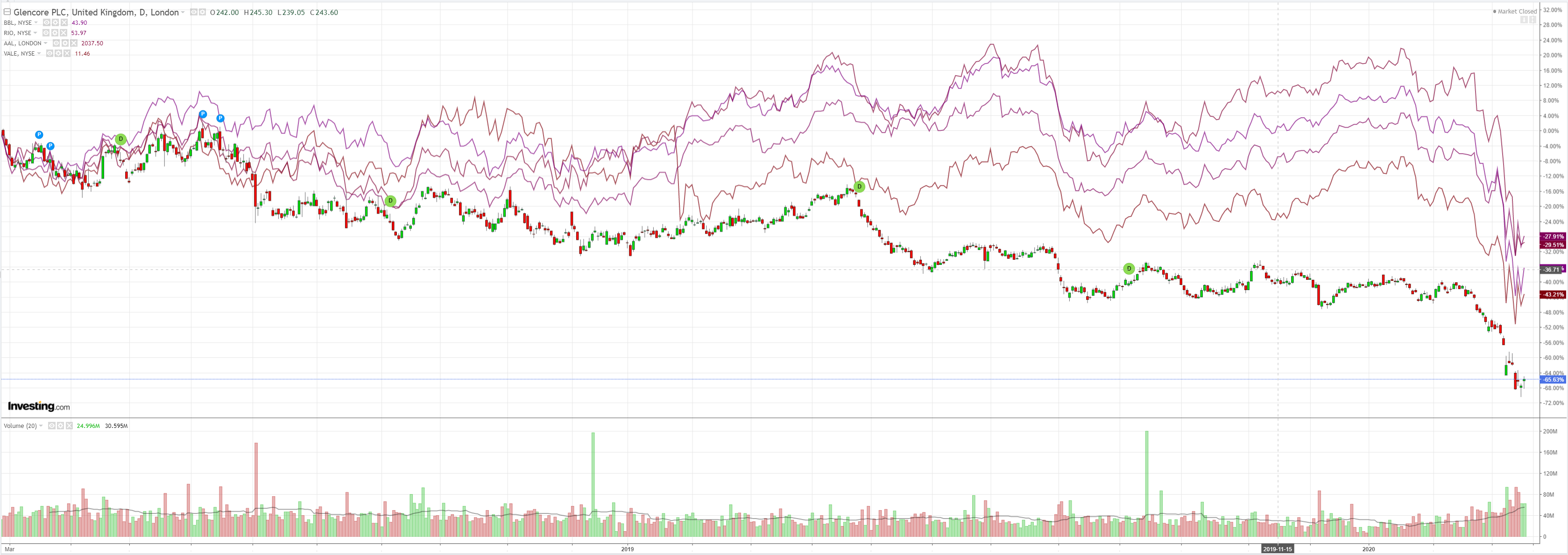

Miners are now iron ore patsies, the end:

EM stocks bounced:

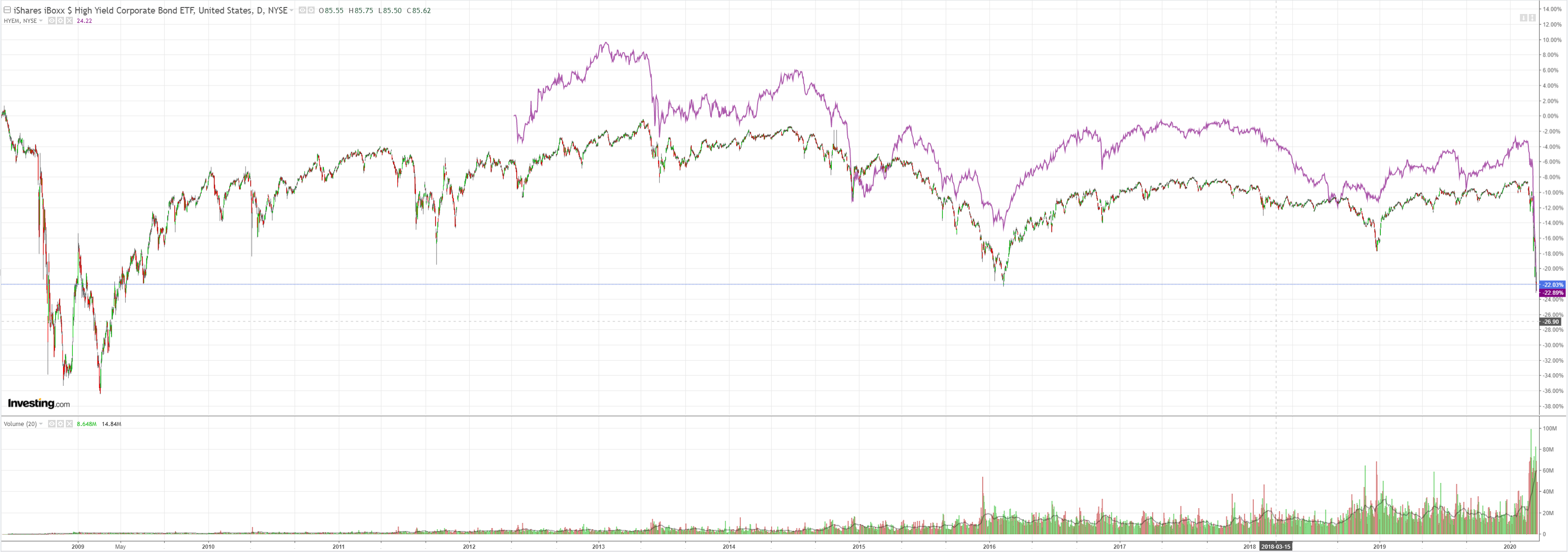

Global junk went no bid. Beware everything:

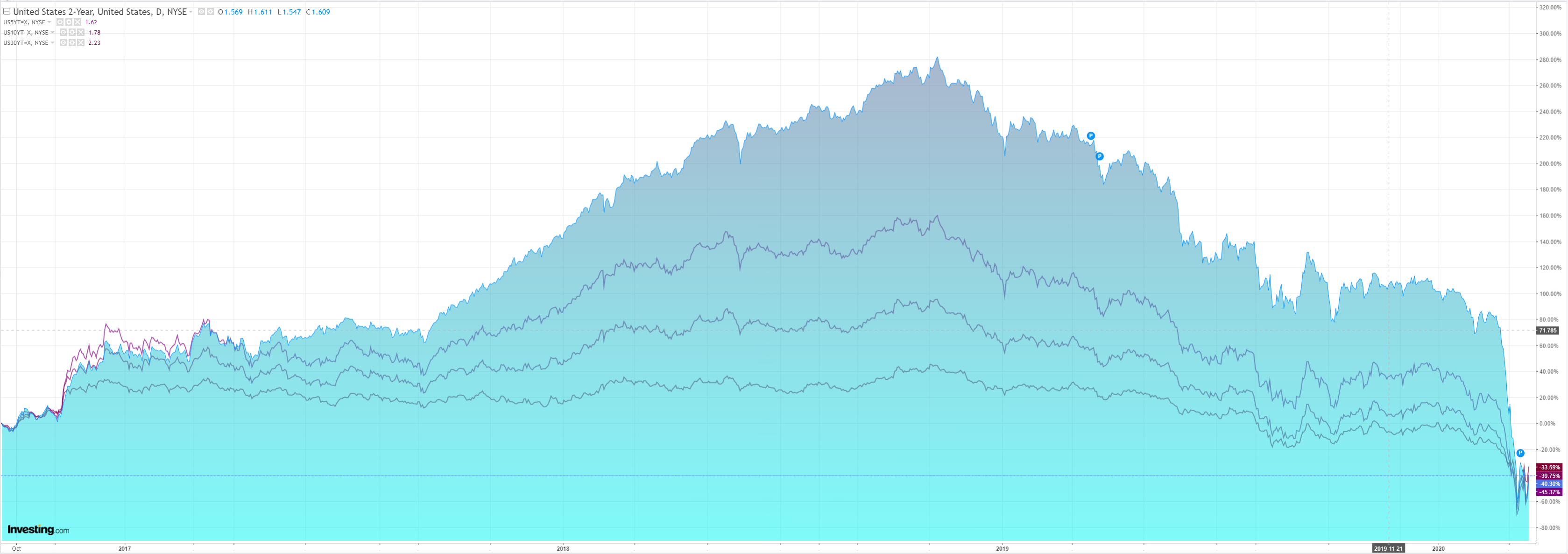

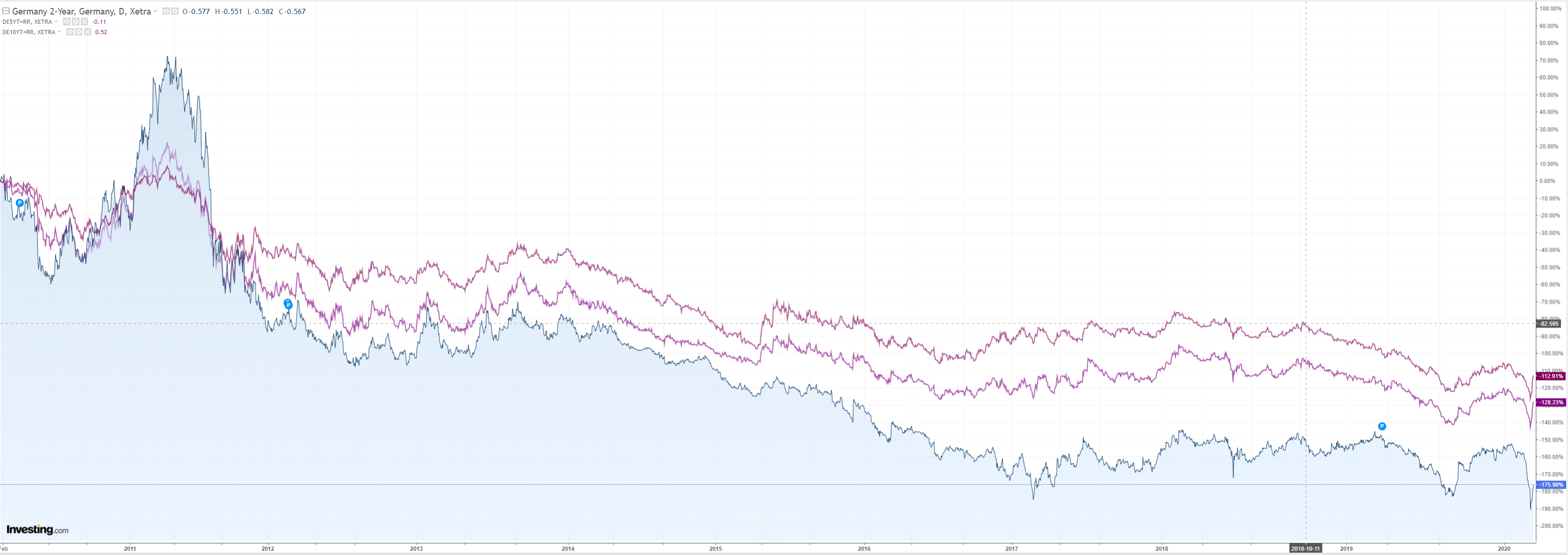

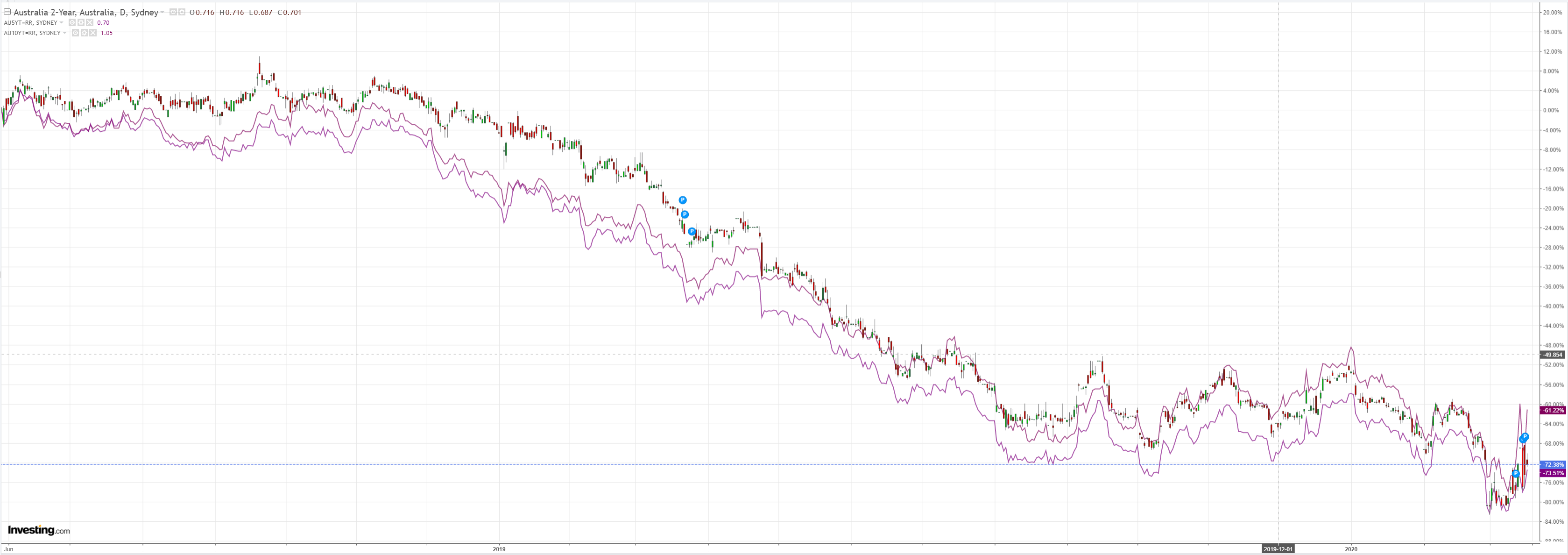

All bonds eased:

As stocks rebounded:

We are not at the bottom in anything. Indeed, we are not even out of outright monetary crisis. Via Zoltan Pozsar at Credit Suisse:

The Fed’s liquidity injections appear not to be working.

All segments of funding markets – secured, unsecured and FX swaps – continue to show growing signs of stress. The Fed may have to do more still.

In the U.S., we watched, but didn’t feel the funding impact of large banks in other countries being asked to help their economies. Now that U.S. banks are asked to do the same, dollar funding markets are starting to feel the impact.

As U.S. banks increase their lending to the real economy as corporations draw on credit lines and banks lend more to households and firms, lending will consume more balance sheet and risk capital, and that will leave less room for market making and arbitrage, which under current circumstances are “luxury”.

The breakdown of o/n repo markets yesterday tell us that balance sheet is now getting scarce to conduct even the most basic type of market making.

As banks are pulling back from market making, the Fed and other central banks need to assume the role of dealer of last resort…

The Fed needs to become a buyer of CDs and CP, but not through the CPFF.

The Fed needs to offer dollars on a daily frequency through the swap lines, and other central banks need to lend dollars on to both banks and non-banks.

The Fed needs to broaden access to the swap lines to other jurisdictions as dollar funding needs are large in Scandinavia, Southeast Asia, Australia and South America, not just in the G-7. The dollar funding needs of both banks and non-banks is what’s at risk and the assets that are being funded are U.S. assets – Treasuries, MBS and credit – so the Fed has a vested interest.

A hallmark theme of the post-QE global financial order has been the secular growth of FX hedged fixed income and credit portfolios at non-bank institutions like life insurers and asset managers from negative interest rate jurisdictions – the new shadow banking system, epitomized by money market funding (FX swaps) of capital market lending (Treasuries and the full credit spectrum).

Carry makes the world go round and as banks do more for the economy central banks will have to backstop the shadow banking system – yet again…

More stress ahead. More Fed action ahead. More DXY rocket ahead. More crashing Australian dollar ahead.

And that’s only the northern hemisphere crisis. Wait until it begins to clear in the northern hemisphere Summer and Australia is left alone as the last bastion of the Winter virus…