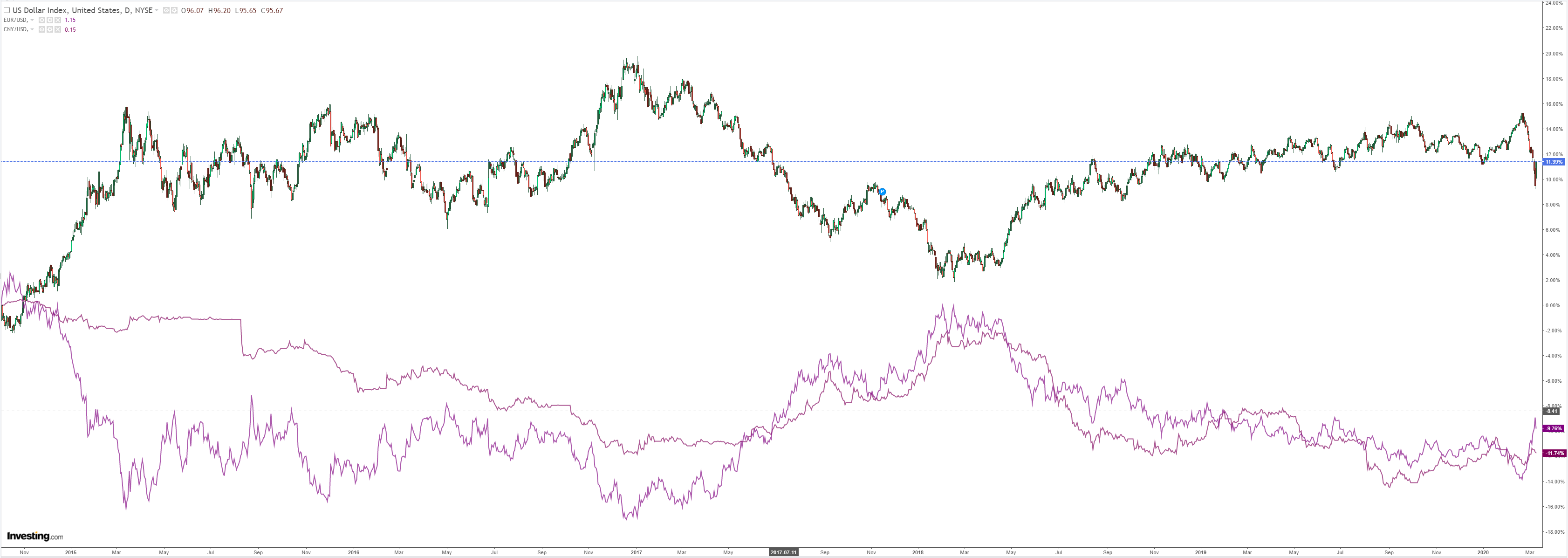

DXY launched last night as EUR flamed out:

The Australian dollar was crushed:

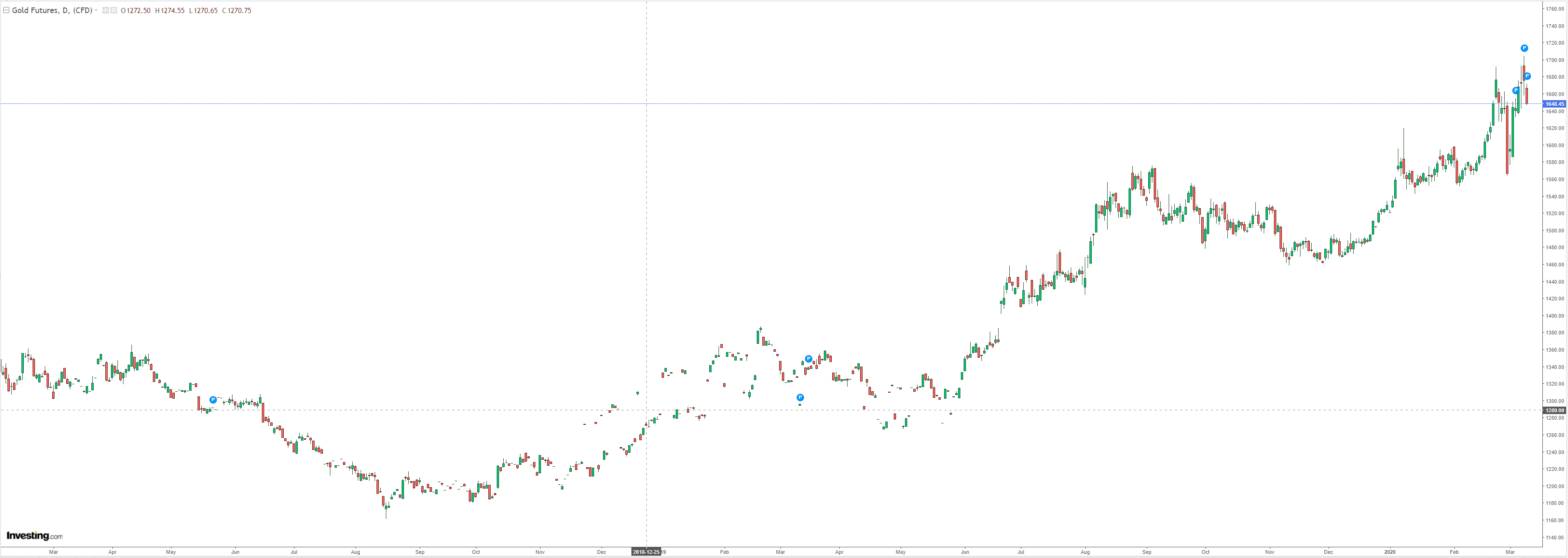

Gold fell:

Commodities bounced:

Miners to the moon:

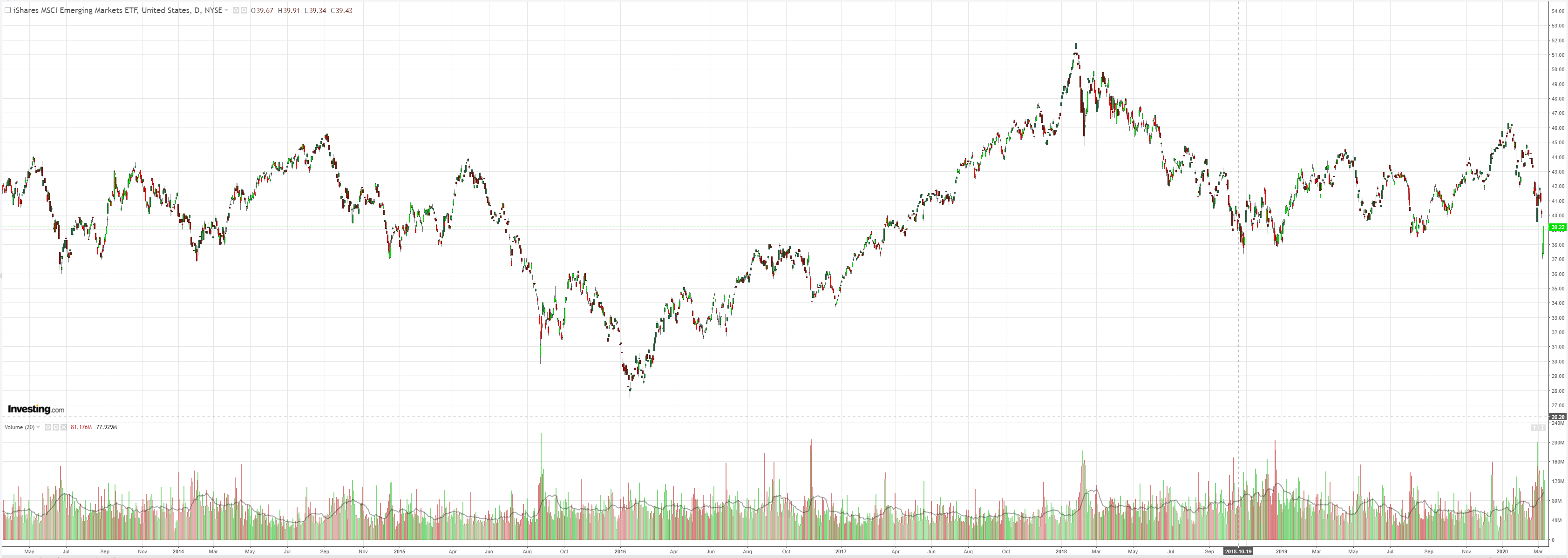

And EM stocks:

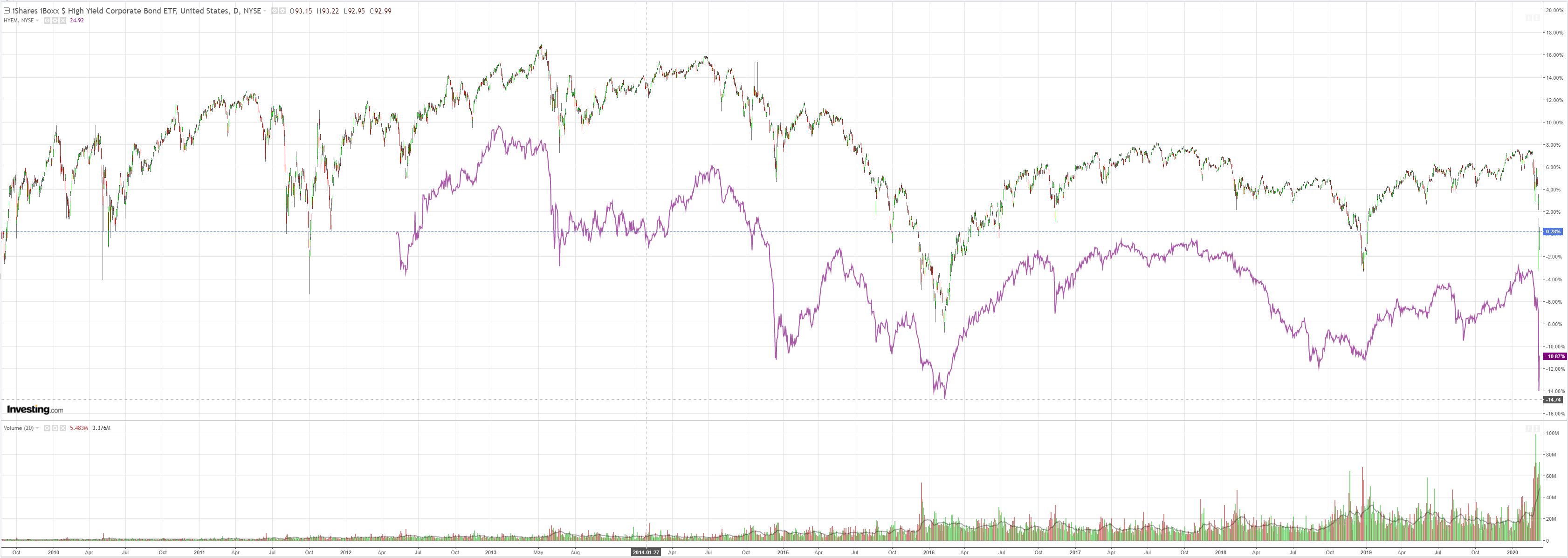

And junk

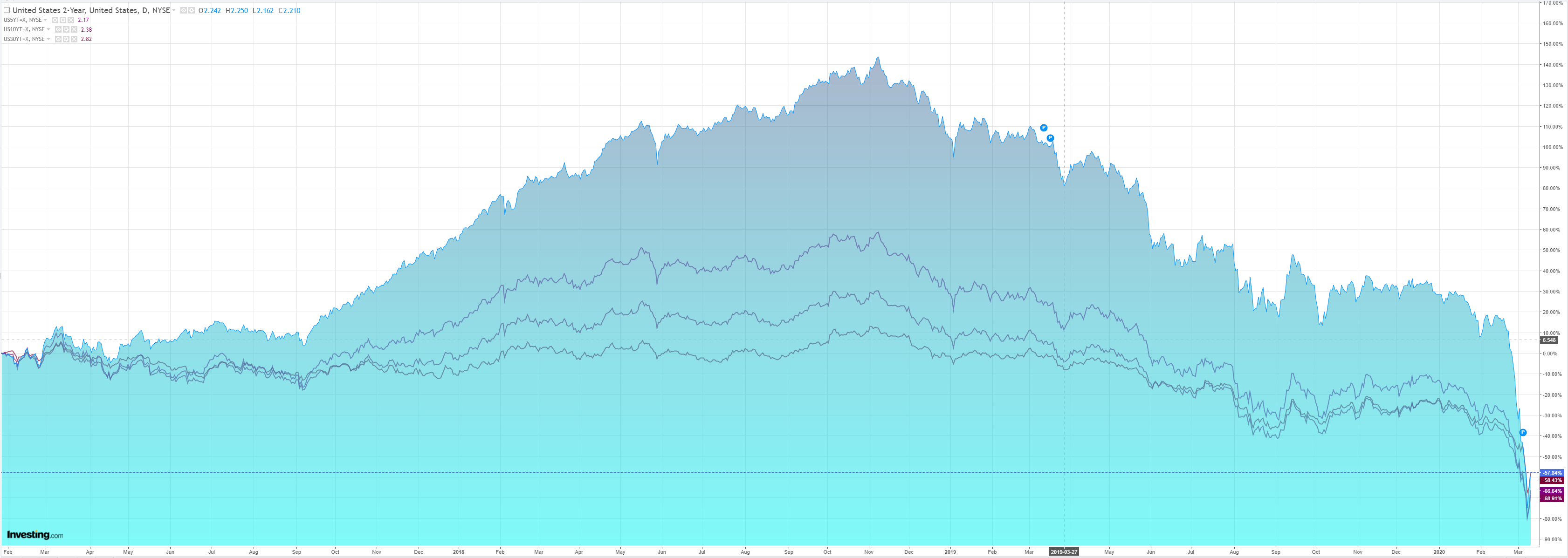

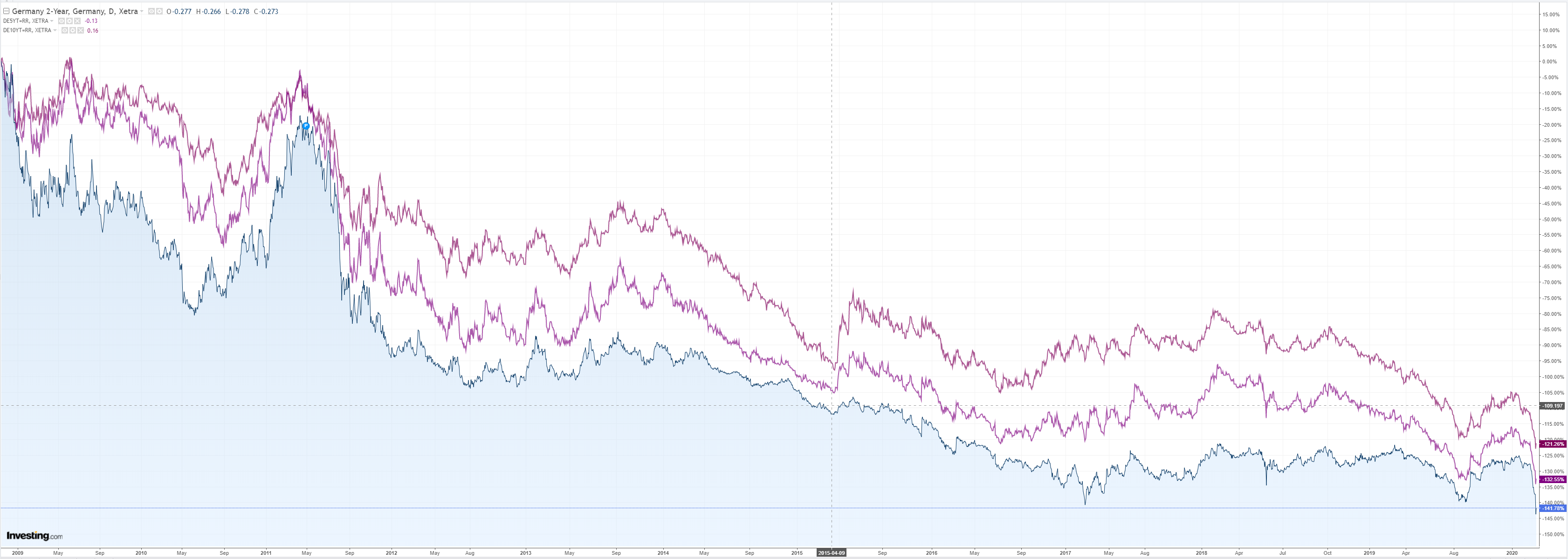

Bonds were hosed:

Stocks to the moon:

Westpac has the wrap:

Event Wrap

Coronavirus update: Latest WHO data, via the Situation Reports, shows 109,578 cases confirmed as at 9 March, with 45 new cases in China and 3949 new cases outside China. The latter continues to accelerate. Unofficial sources such as Worldometer show cases ex-China rose by 4,028 on 10 March.

Euro Area Q4 GDP was unrevised in its second estimate at 0.1%, for an annual pace of 1.0%. Growth in the region slowed in 2019 and is clearly at risk in 2020.

US NFIB small business optimism index rose from 104.3 to 104.5 in Feb, indicating strength in that sector before coronavirus concerns escalated.

Event Outlook

NZ electronic retail spending is estimated to have fallen 0.3% in Feb. REINZ housing data for Feb may be released.

RBA Deputy Governor Debelle will speak on investment at the Australian Financial Review Business Summit at 9am. Westpac-MI consumer sentiment for March will follow later in the morning as will January housing finance. For sentiment, COVID-19 is likely to dominate, its spread across the world over the past month seeing markets move sharply lower. Housing finance meanwhile is expected to lift 2.0% in January following a 4.4% gain in December.

In the US, the February CPI is expected to print a flat outcome as energy prices offset a 0.2% gain for core prices.

It was an eveing of “dead bat bounce”, from RaboBank:

Monday was one of those days that will live long in market infamy. The scale and breadth of moves seen was up there with the very blackest, or should one say reddest, after the Saudis released a second oil Black Swan on top of the one China already released with Covid-19 – though the official line from China is now that nobody knows where the virus started.

These are extraordinary times. We saw the S&P close -7.6% and the Dow -7.8%: we are now down six whole baseball caps in the latter since the end of February. As I type we see the US 10-year Treasury yield is at 0.67%, which if you had just returned from Mars would be a jaw-dropping figure – until you realise that we were at 0.31% at one point intra-day yesterday. As I said, the scale of moves is just amazing.

After Panic Monday we are currently seeing what looks like a dad bat bounce. US stock futures are up around 3%, Asian bourses have generally staged small rallies, USD/JPY is up to 104.7, and EURUSD is back to 1.1359, while even Brent crude is up 7.3% (to just USD36.88, of course). The reason for this optimism is purely technical, and lies not in what we see unfolding in front of us.

…Of course, we need to focus on what are now going to be a flood of fiscal and monetary policy responses. But to differentiate between a bat that can fly and a dead bat bounce, we need to look and see what is being done on the ground to fight the virus. Only when that corner is turned can we start to argue for a return to market normality – and we are a long way from that corner being turned globally.

For example, even if South Korea and China stay virus free (which remains to be seen), won’t they have to seal themselves off until everyone else has achieved the same status? If they don’t it will re-enter the country and spread again, necessitating fresh panic and lockdowns. Either we all sort this out, even in places nobody is even looking at, like Africa; or we all seal ourselves in. Neither option suggests the bottom is in for markets yet, even if today gives us some room to breathe (behind a mask, I hope).

That pretty much sums it up. The trigger for the dead bat was rushed Trumpian stimulus, at CNN:

President Donald Trump and top economic officials will pitch wary Senate Republicans on a payroll tax cut and other policy proposals meant to ease the economic fallout of coronavirus during a closed-door lunch on Tuesday, a senior administration official told CNN.

The President is now expected to attend the meeting, a senior administration official and Texas Republican Sen. John Cornyn said late Tuesday morning.White House economic officials plan to lay out additional measures to try and arrest the economic pain stemming from the spread of the virus, including proposals to implement paid sick leave, deferral on tax collection on specific industries including airlines, cruise lines and hotels, and specific proposals to make small business loans more available and with flexible repayment options, according to the two people.