DXY was up last night:

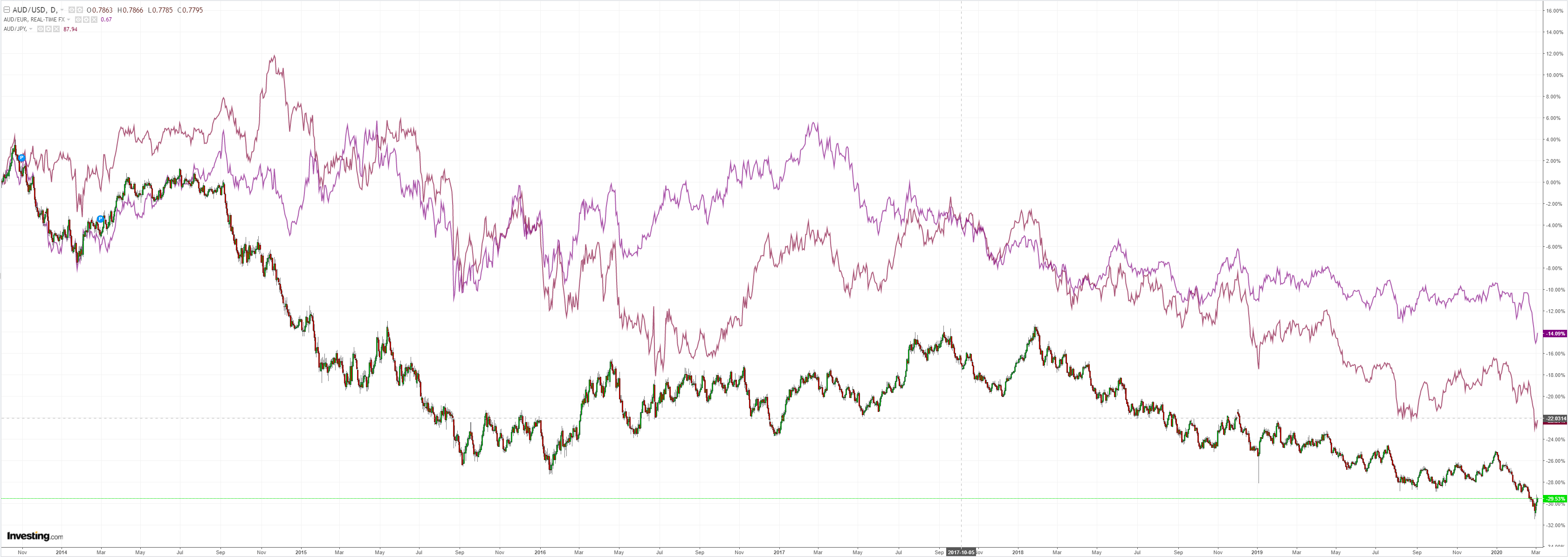

But the Australian dollar was anyway, across the board actually, as it built upon its RBA stupidity premium:

Gold held on:

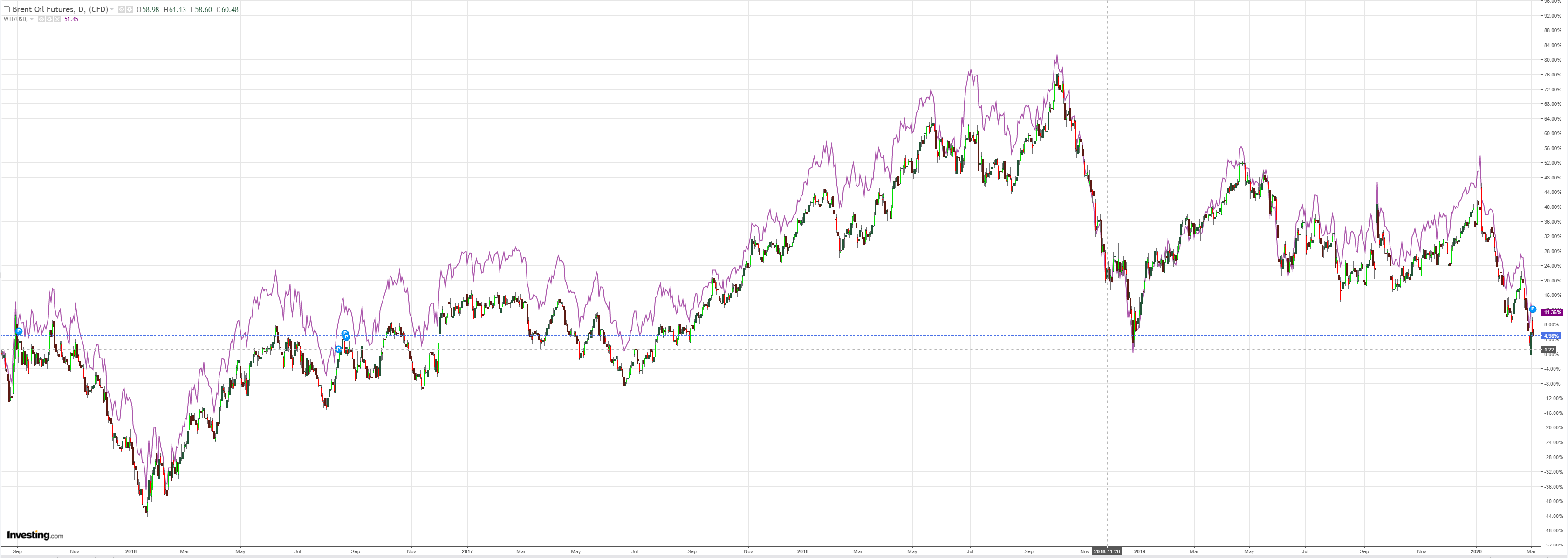

Oil is struggling:

Metals too:

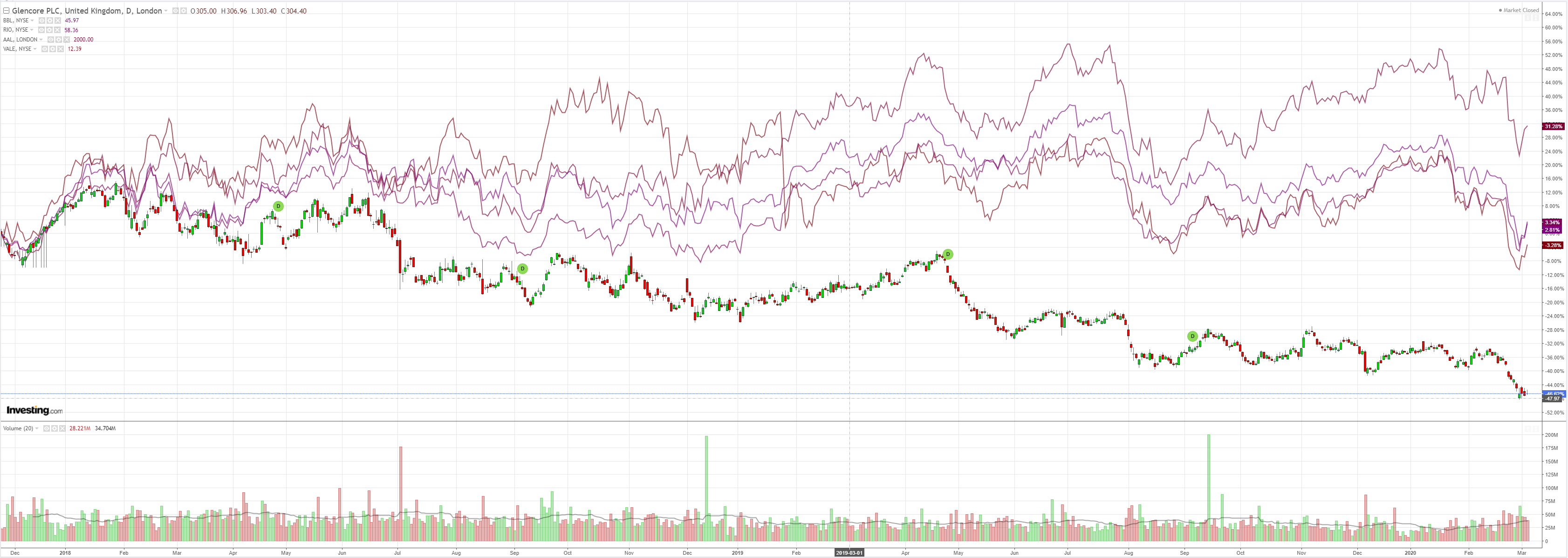

Miners to the moon!

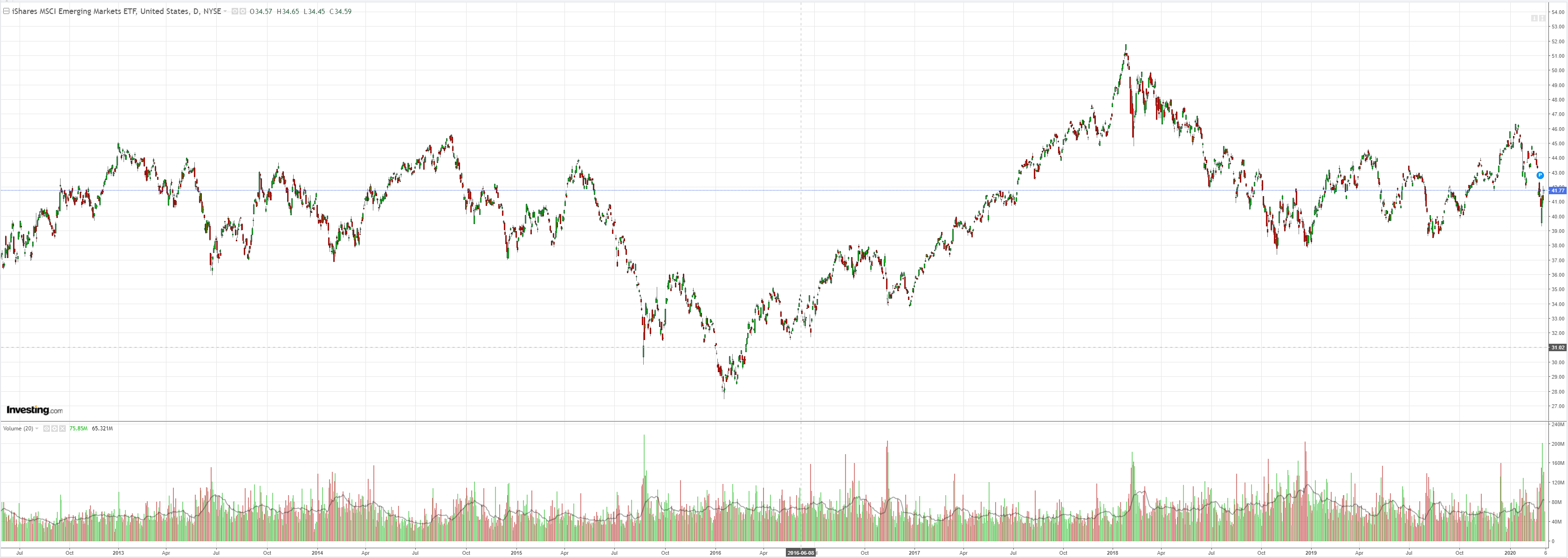

EM stocks too:

Junk is fixed:

Bonds were soft:

And stocks lifted for the imminent global boom:

Actually, pundits reckon stocks lifted as Fake Left doyen, Joe Biden, closes in the DNC presidential nomination, guaranteeing Trump a second term. I honestly don’t know. Stocks look insane to me right now.

As for the Australian dollar, the Central Bank of Canada did a great job of underlining the RBA stupidity premium that is being built into the currency for now. It cut 50bps and the statement was excellent compared to the RBA’s happy clappy dross:

The Bank of Canada today lowered its target for the overnight rate by 50 basis points to 1 ¼ percent. The Bank Rate is correspondingly 1 ½ percent and the deposit rate is 1 percent.

While Canada’s economy has been operating close to potential with inflation on target, the COVID-19 virus is a material negative shock to the Canadian and global outlooks, and monetary and fiscal authorities are responding.

Before the outbreak, the global economy was showing signs of stabilizing, as the Bank had projected in its January Monetary Policy Report (MPR). However, COVID-19 represents a significant health threat to people in a growing number of countries. In consequence, business activity in some regions has fallen sharply and supply chains have been disrupted. This has pulled down commodity prices and the Canadian dollar has depreciated. Global markets are reacting to the spread of the virus by repricing risk across a broad set of assets, making financial conditions less accommodative. It is likely that as the virus spreads, business and consumer confidence will deteriorate, further depressing activity.

In Canada, GDP growth slowed to 0.3 percent during the fourth quarter of 2019, in line with the Bank’s forecast, although its composition was different. Consumption was stronger than expected, supported by healthy labour income growth. Residential investment continued to grow, albeit at a more moderate pace than earlier in the year. Meanwhile, both business investment and exports weakened.

It is becoming clear that the first quarter of 2020 will be weaker than the Bank had expected. The drop in Canada’s terms of trade, if sustained, will weigh on income growth. Meanwhile, business investment does not appear to be recovering as was expected following positive trade policy developments. In addition, rail line blockades, strikes by Ontario teachers, and winter storms in some regions are dampening economic activity in the first quarter.

CPI inflation in January was stronger than expected, due to temporary factors. Core measures of inflation all remain around 2 percent, consistent with an economy that has been operating close to potential.

In light of all these developments, the outlook is clearly weaker now than it was in January. As the situation evolves, Governing Council stands ready to adjust monetary policy further if required to support economic growth and keep inflation on target. While markets continue to function well, the Bank will continue to ensure that the Canadian financial system has sufficient liquidity.

The Bank continues to closely monitor economic and financial conditions, in coordination with other G7 central banks and fiscal authorities.

The market greeted it with a big fall in the CAD versus the RBA’s ridiculous 25bps and big rise in the AUD.

Next month the RBA will cut again and we’ll be into the era of unconventional monetary policy. What will that look like? Who knows. Because rather than look forward and describe it in gory detail to keep up the curreny pressure, the bank is looking backwards as usual. In parliament yesterday was Reserve Bank deputy governor Guy Debelle:

“One part we can get a handle on is tourism and education. We have looked at student visa numbers our estimate is they will fall by 10 per cent.

“They account for 2 per cent of GDP so they will subtract about 0.5 per cent of GDP. And we are sitting here and it’s the 4th of March so there is a month to go.”

…”If people go out and and clean the shelves out, that boosts consumption in the short term – presumably you are bringing forward some of those purchases.”

“The board took this decision to support the economy as it responds to the global coronavirus outbreak.”

“The coronavirus outbreak overseas is having a significant effect on the Australian economy at present, particularly in the education and travel sectors.”

Rather than looking on the bright side of a toilet paper cleanout, perhaps the bank might like to contemplate what the imminent six month shut down of the entire economy will look like. Just a thought.

It is for that reason that I do not see the AUD at its lows yet despite the extraordinary blundering of the RBA. Within a few months it will be printing Australian dollars like toilet paper.

Whether it knows it today or not.