DXY was firm last as EUR fell with stocks:

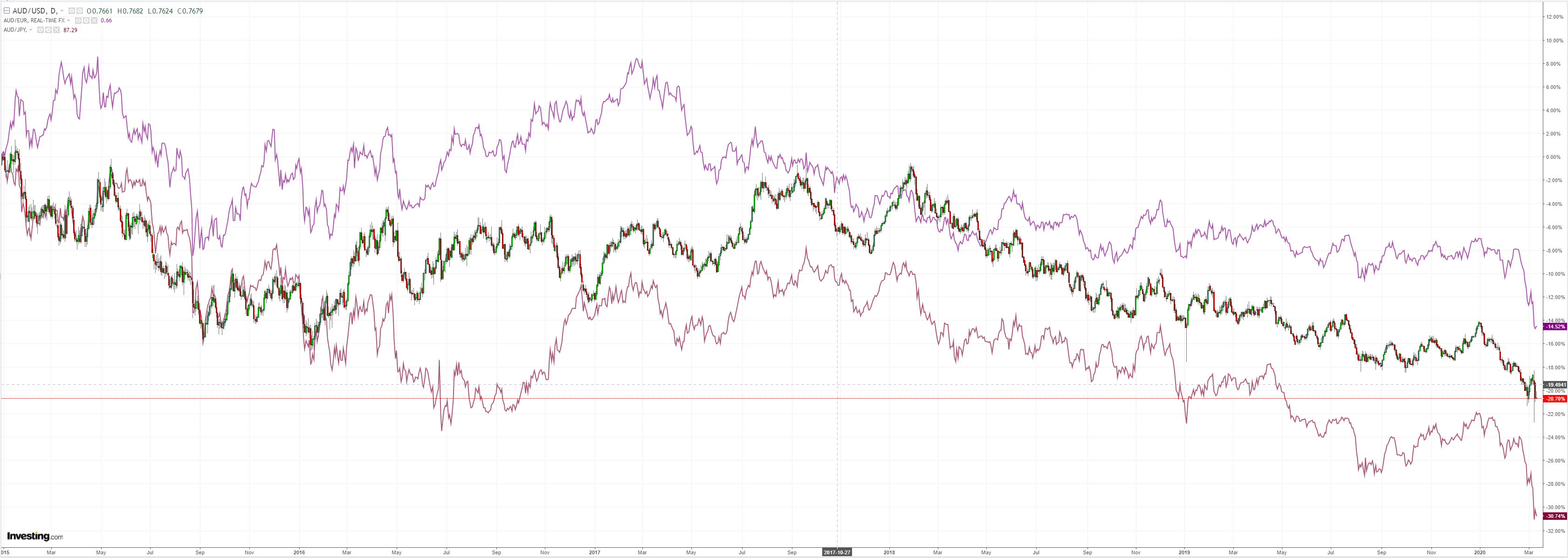

The Australian dollar was belted:

Though could not keep pace with EMs:

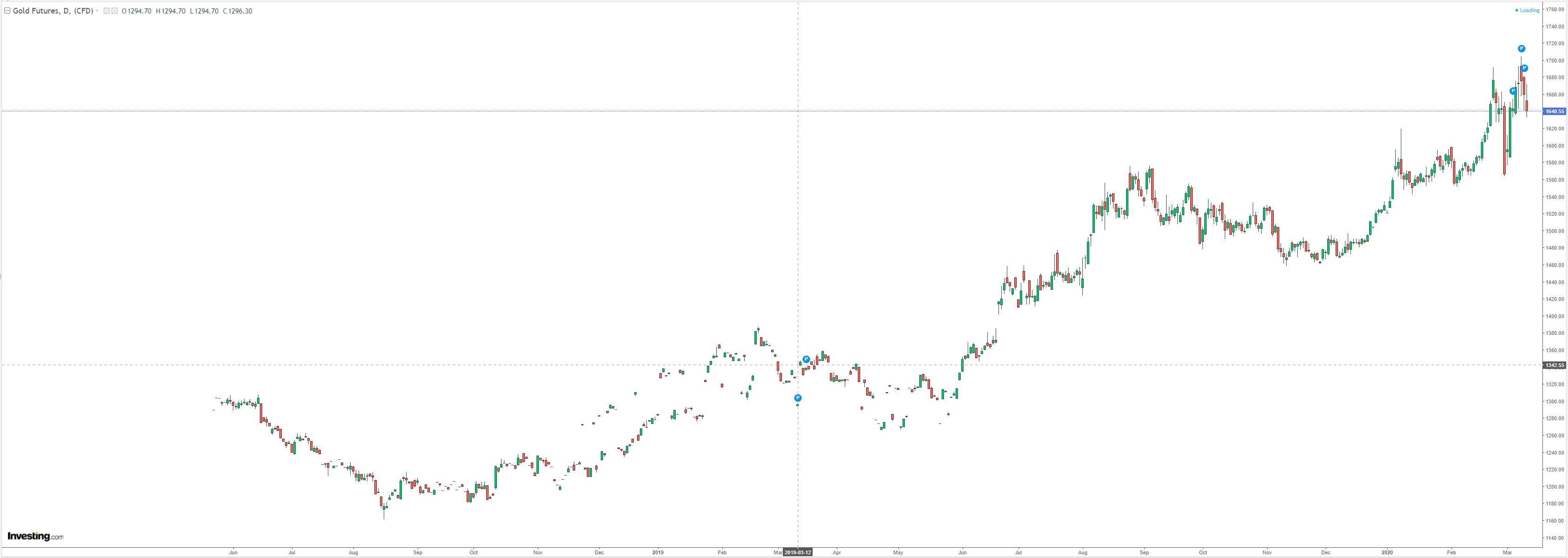

Gold has another hint of liquidation:

Oil is finished:

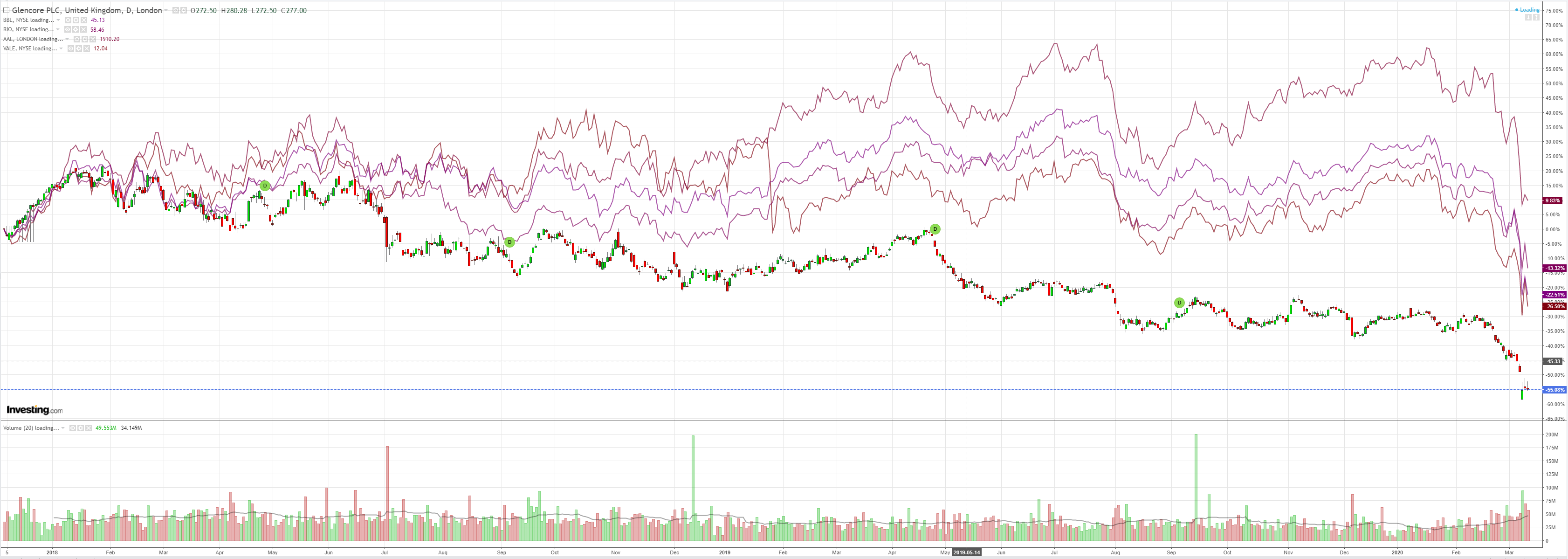

Base metals were weak:

Miners reversed down:

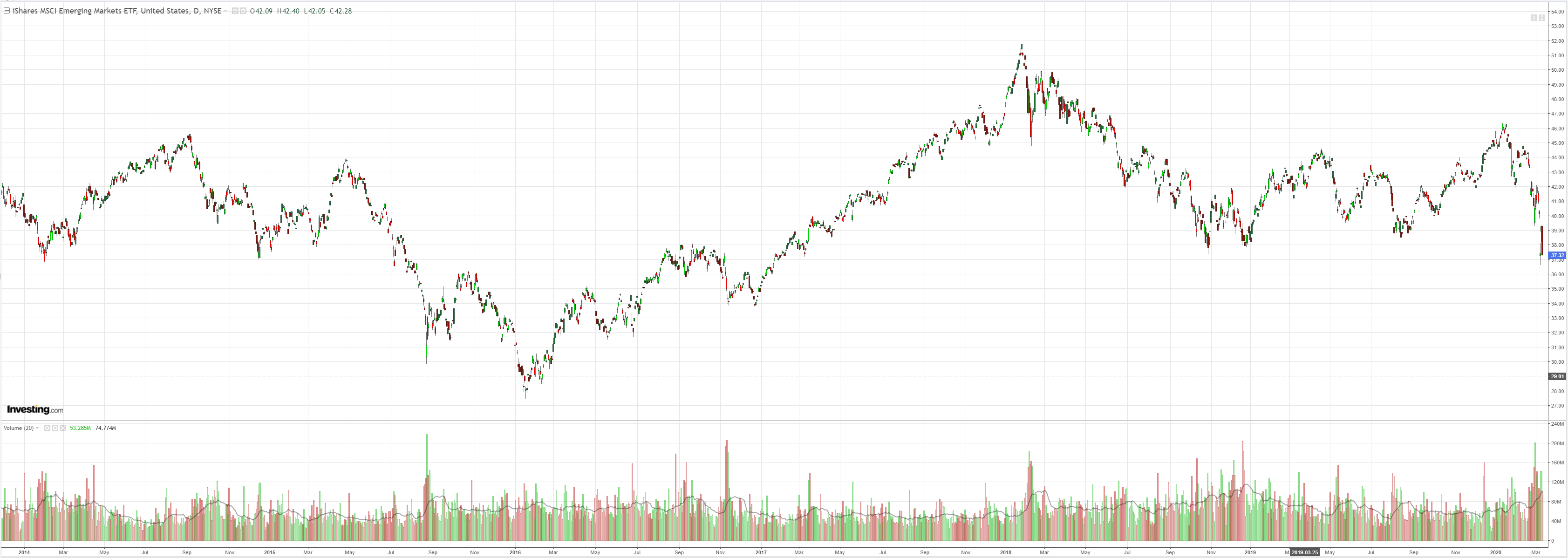

EM stocks are going over the cliff:

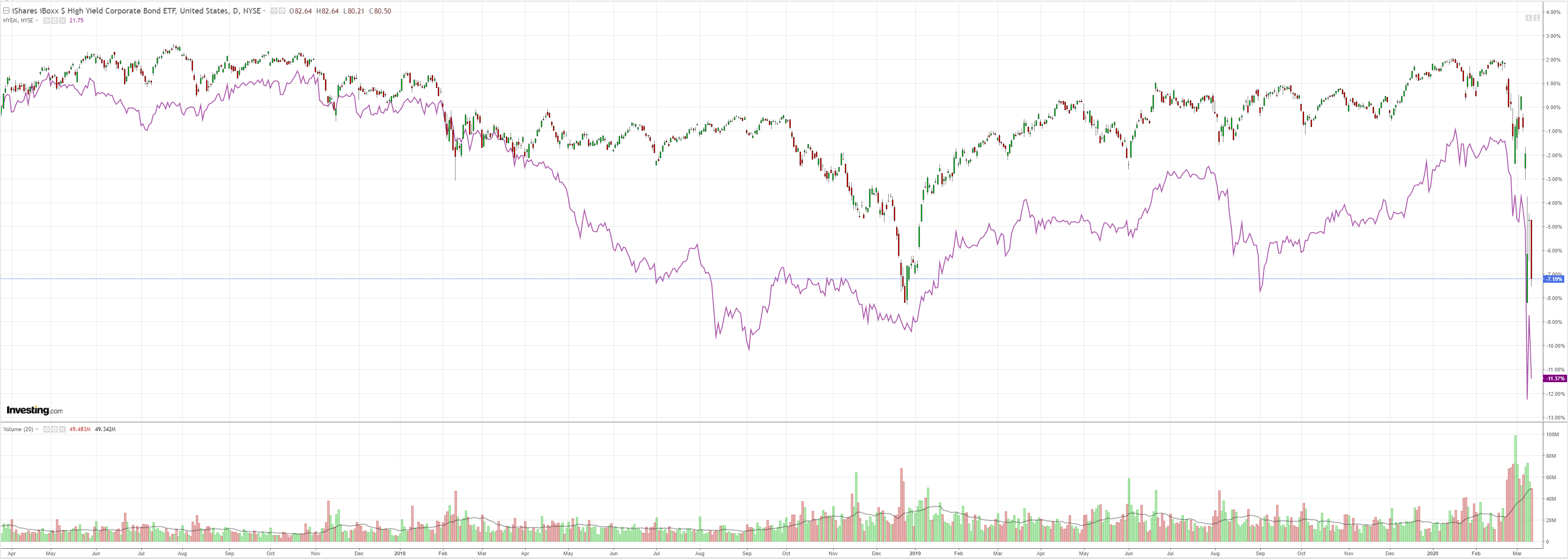

With junk:

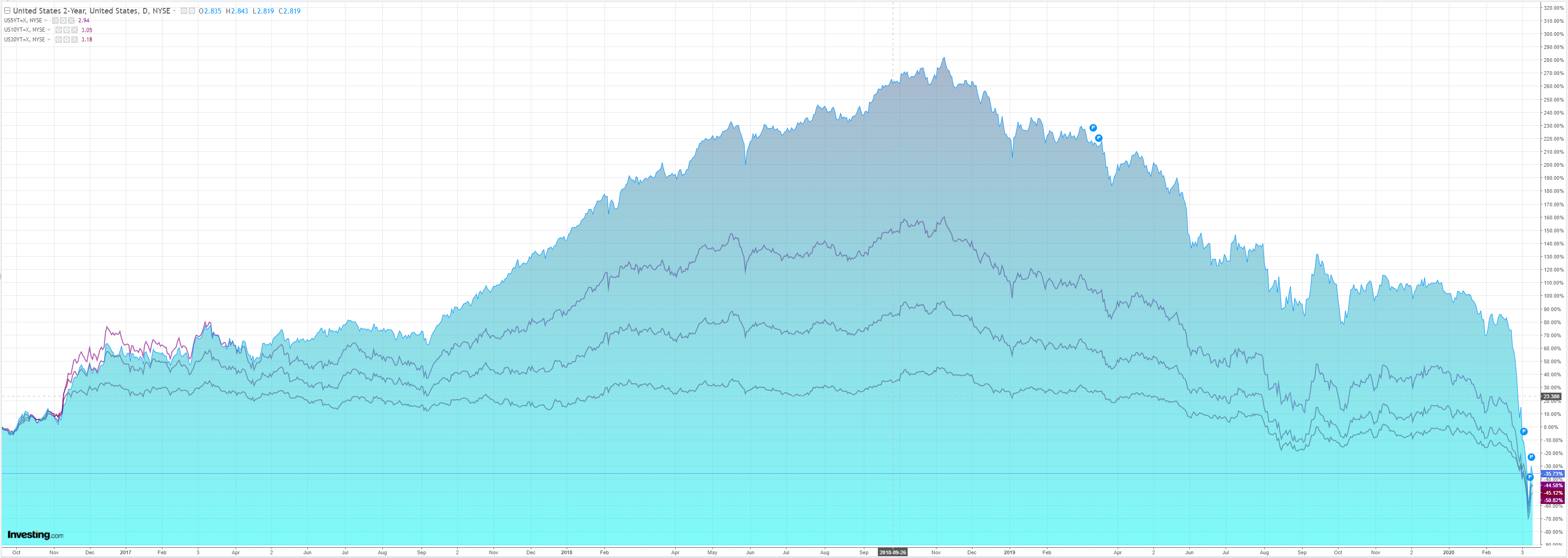

Oddly, all bonds were sold, presumably on fiscal bets:

As stocks were smashed again:

Westpac has the wrap:

Event Wrap

Coronavirus update: Latest WHO data, via the Situation Reports, shows 113,702 cases confirmed as at 10 March, with 20 new cases in China and 4105 new cases outside China. The latter continues to accelerate. Unofficial sources such as Worldometer show cases ex-China rose by 6,114 on 11 March, the large jump caused by Italian cases rising by 2.313.

Bank of England cut its cash rate 50bps to 0.25% in a surprising inter-meeting move (the first since 2008), taking the rate back to the post Brexit-vote insurance low in 2016-17. The

BoE also launched new targeted funding for SME’s (TFSME) to provide funding for businesses and individuals impacted by COVID-19. It erased the countercyclical capital buffer previously imposed on banks (1% of banks’ UK borrower exposure), releasing up to GBP190bn of lending potential to be targeted towards disrupted businesses. The UK Government unveiled a GBP30bn package of COVID-19 related support within a broadly expansionary Budget in coordination with the BoE’s actions.Throughout the day there were headlines from multiple officials suggesting moves to release support packages from France, Germany, Italy (increasing COVID-19 spending to EUR 12bn and potentially EUR20bn) and the US.

US Feb CPI at 2.3%y/y beat estimates of 2.2%y/y, with core CPI ex food and energy at 2.4% (est. 2.3%).

Event Outlook

The ECB’s March meeting is today’s main event. A 10bp deposit rate cut is expected along with some form of alternative measures to support liquidity and credit supply and to limit risks around credit spreads. As demand needs support, an increase in monthly asset purchases would be most effective. However, another wave of TLTROs is also an option.

Eurozone January industrial production data is also due, as is February PPI data for the US. The market will likely show greater interest in US initial claims though. Any signs of job shedding will unnerve the market.

Are we at a forex inflexion point here? All past days of stocks liquidation have been met with DXY falls as the EUR carry trade reversed. It cannot be overstated how significant a regime change that this represents. We live in a USD and Eurodollar world. There is no alternative. When trouble strikes, DXY is bid.

At least, there wasn’t an alternative. If the EUR keeps rallying into safe haven status then DXY may well be at some invisible turning point in its viability as the global reserve.

Don’t get me wrong. I’m not saying EUR is the emerging reserve. That’s preposterus given its half-baked underpinnings. The question is more about the primacy of DXY. This harks back to the conversation started by Mark Carney at Jackson Hole last year, via Reuters:

Bank of England Governor Mark Carney took aim at the U.S. dollar’s “destabilizing” role in the world economy on Friday and said central banks might need to join together to create their own replacement reserve currency.

The dollar’s dominance of the global financial system increased the risks of a liquidity trap of ultra-low interest rates and weak growth, Carney told central bankers from around the world gathered in Jackson Hole, Wyoming, in the United States.

“While the world economy is being reordered, the U.S. dollar remains as important as when Bretton Woods collapsed,” Carney said, referring to the end of the dollar’s peg to gold in the early 1970s.

Emerging economies had increased their share of global activity to 60% from around 45% before the financial crisis a decade ago, Carney said.

But the dollar was still used for at least half of international trade invoices – five times more than the United States’ share of world goods imports – fuelling demand for U.S. assets and exposing many countries to damaging spillovers from swings in the U.S. economy.

CNY is not ready for that role. Gold is not widely enough accepted. There is no Keynesian-style bancor seriously in the works yet. Bitcoin pfft.

So perhaps it is not surprising that as this virus crisis intensifies, markets return to the status quo of the USD/DXY safe haven. In the process, that lets the Australian dollar off the DXY hook.

That is my working thesis for now but it is a watching brief. Hopefully it is right. It will help the AUD fall much lower, faster.