DXY has blasted off:

Once again, the Australian dollar sits on the cliff edge:

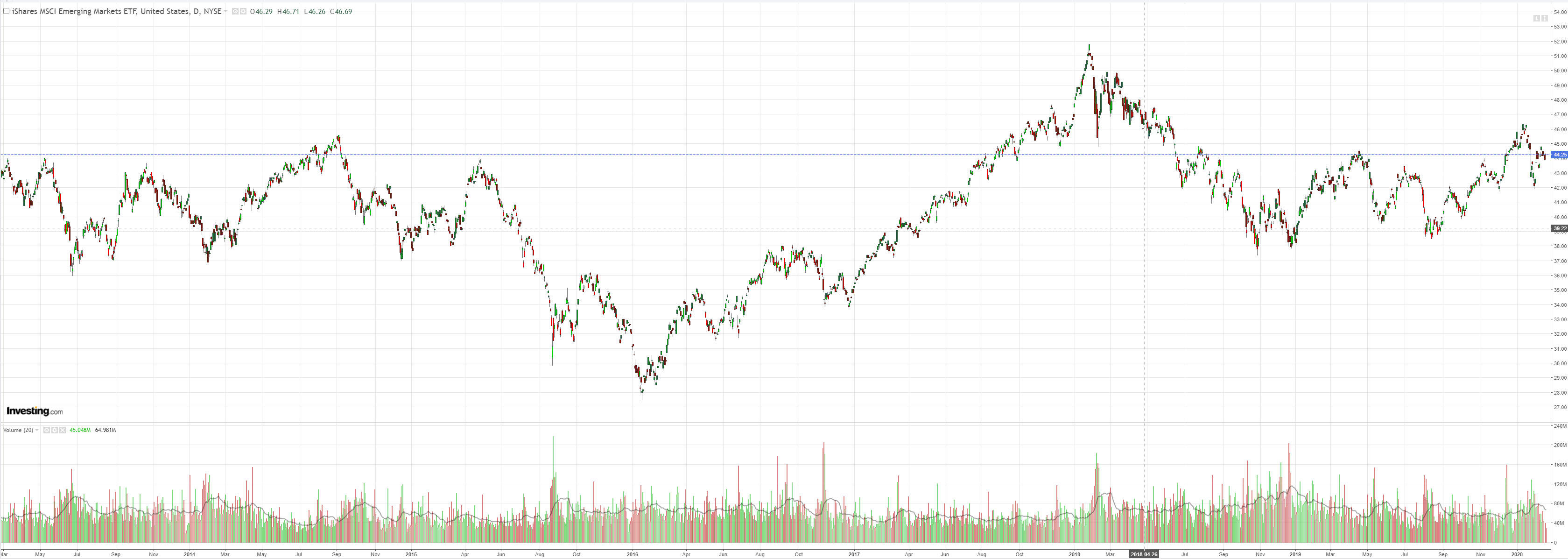

EMs were stronger:

Gold runs on:

Oil popped:

Metals meh:

And miners:

Plus EM stocks:

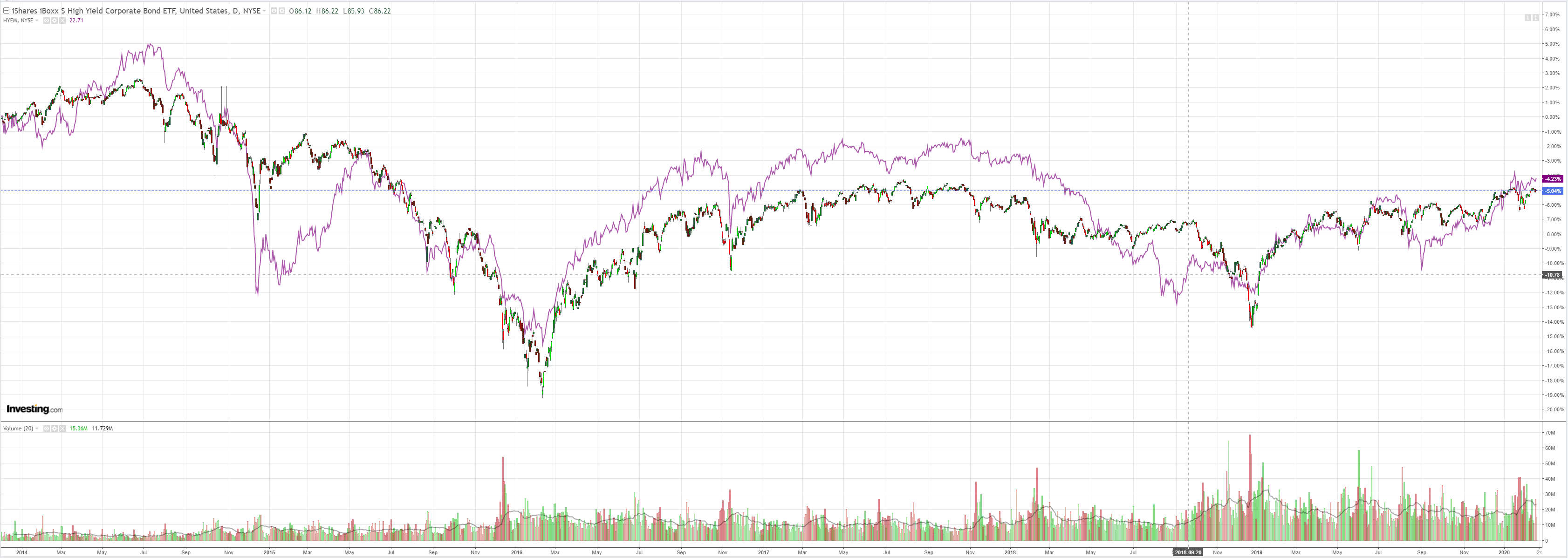

Junk is still fine:

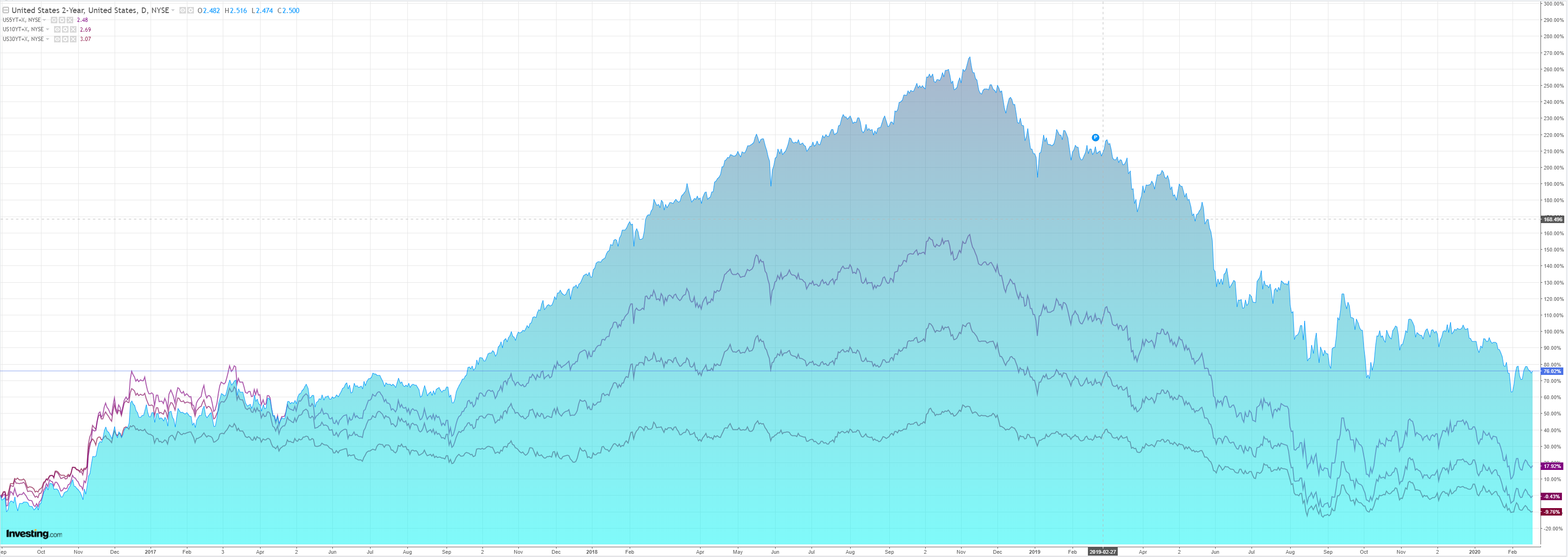

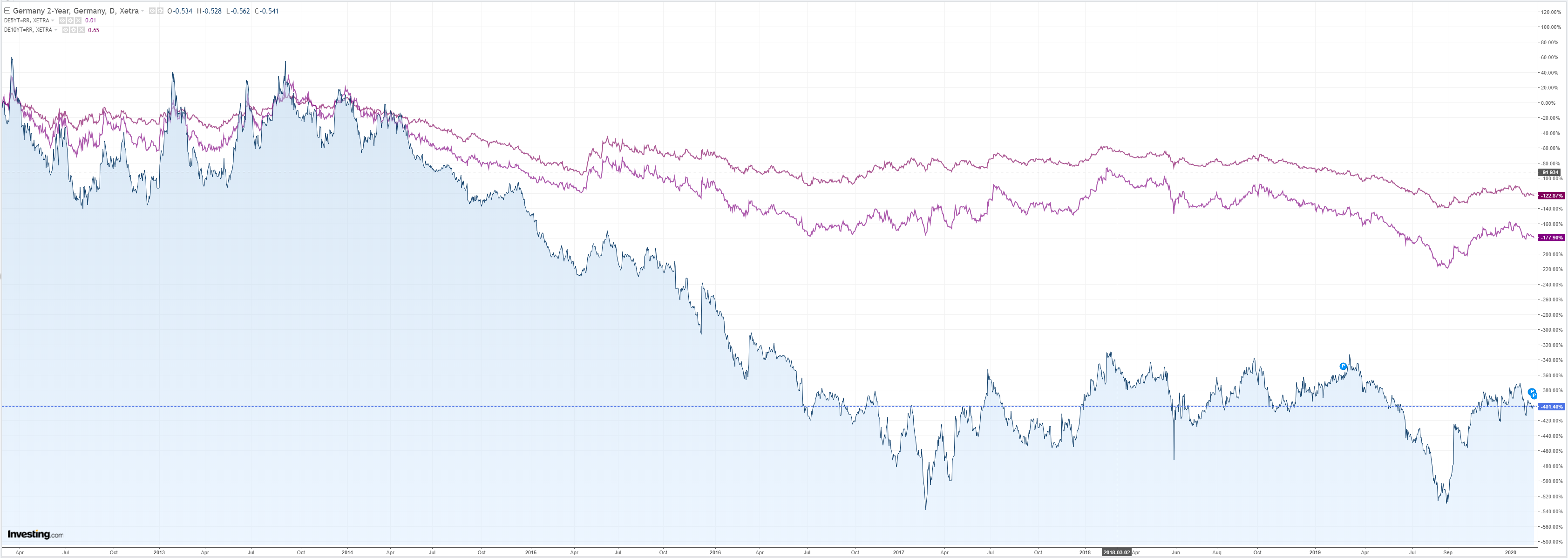

Bonds were soft:

Stocks, or should I say Nasdaq, to the moon:

Westpac has the wrap:

Event Wrap

The FOMC minutes just released offered little new, reiterating that the current policy stance should “remain appropriate for a time”. Some trade uncertainties had diminished recently, and there were signs global growth was stabilizing. However, they also noted risks which could slow the current expansion, including the coronavirus outbreak and Middle East tensions. Liquidity operations to support the short-term money markets were seen as becoming less necessary.

US housing starts fell 3.6% in January, not as weak as the 11.2% fall expected, and December was revised higher. Building permits rose 9.2%, beating the +2.1% estimate. A mild winter has added to the well-known fundamental supports of low mortgage rates and a strong labour market. PPI inflation rose 0.5% in January (vs 0.1% expected), the core measure up 0.5% (vs 0.2% expected). These take the annual paces to 2.1% and 1.7%. Strength was concentrated in the services sector.

Fed speakers included Bostic, who reiterated the mantra that policy is in a “good place”; Mester, who said US trade deals should help ease uncertainty; and Kaplan, who said a fall in growth in Q1 and rebound in Q2 and Q3 are expected, but it’s too soon to make that judgement with confidence.

Event Outlook

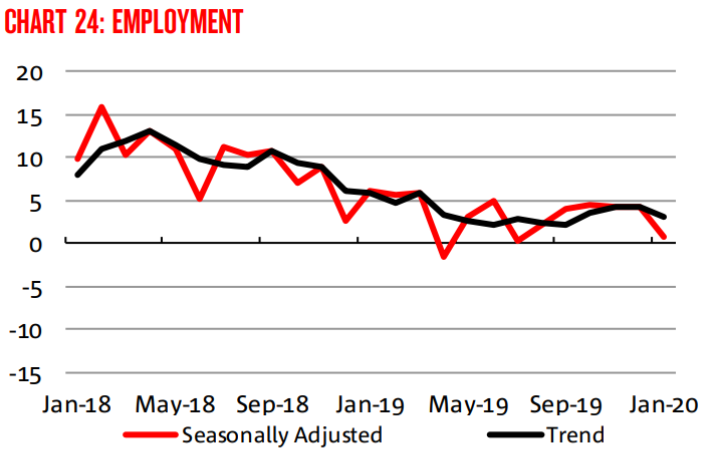

Australia’s January employment data is expected to show an increase of 15k, in line with the lead from recent business surveys. The market anticipates 10k jobs will be created. We look for the unemployment rate to rise to 5.2% from 5.1% despite this job gain as participation edges higher.

NZ Q4 PPI is due, but attracts little attention given Q4 CPI is already known.

For the Euro Area, February consumer confidence will be released. And in the UK, January retail sales are due.

Over in the US, the February Philadelphia Fed Index will follow. And the Federal Reserve’s Barkin, Kaplan, Brainard, Bostic, Clarida and Mester will speak.

Not even threatend withdrawal of liquidity can stop the US stock freight train now. It is out of control come what may:

Normally the Australian dollar would be wildly bid during such a euphoric period. That it is not is further evidence that something is not right with the boom.

Indeed, today, we get another chance for the AUD to finally break

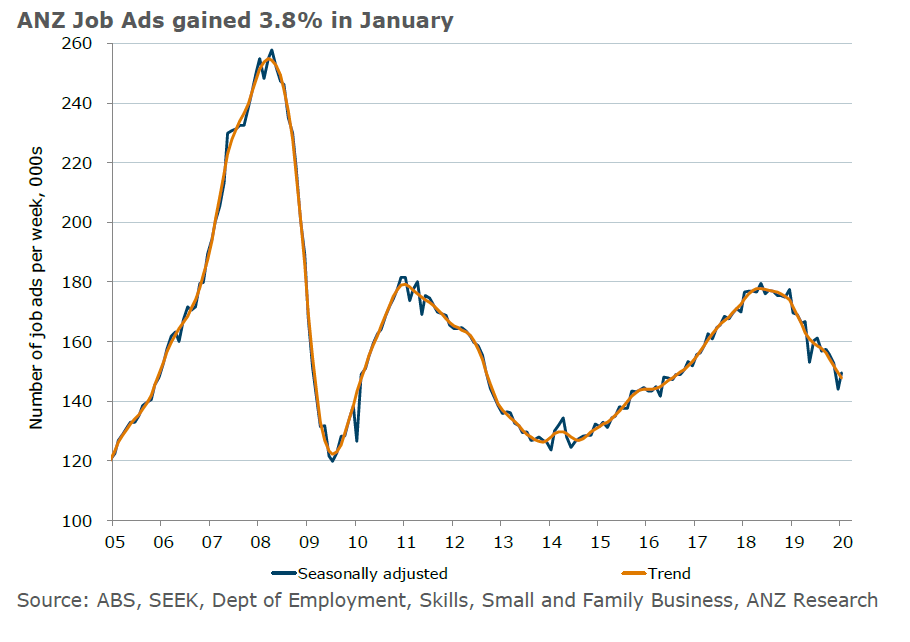

All data has been pointing at rising joblessness for a year. ANZ:

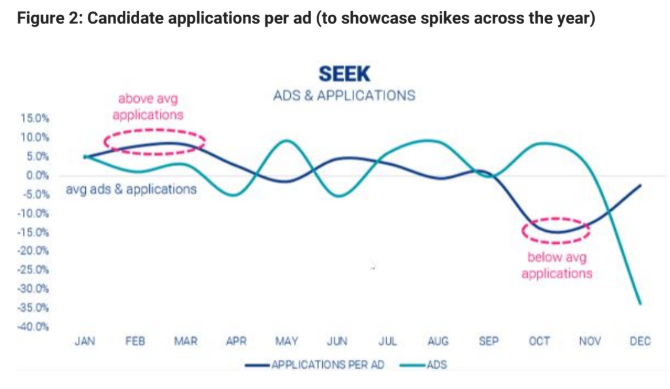

SEEK job ads:

NAB business survery:

The PMIs, Roy Morgan etc, falling wages growth, I could go on, are all pointing to labour market weakening.

Yet we’ve barely seen it in offical data. Will it appear today? Employment reports are a craps shoot, especially ABS numberwang versions, so I have no idea.

All I can say is, we’re due!