Advertisement

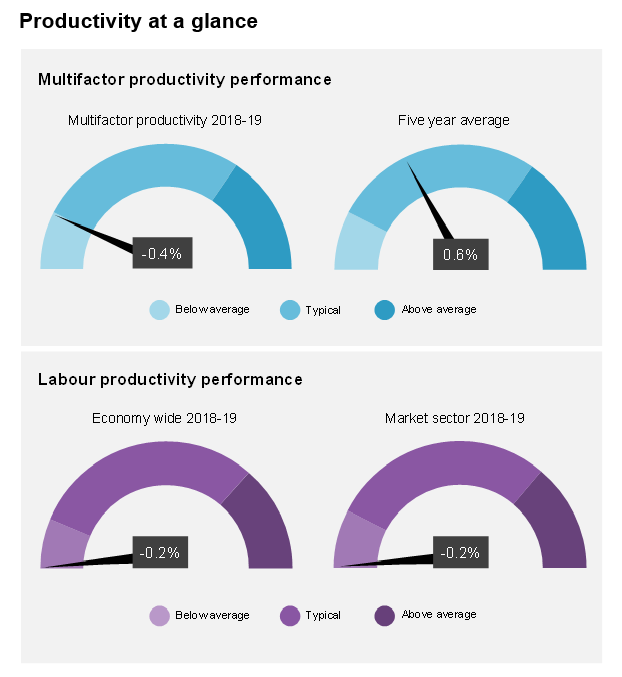

The Productivity Commission (PC) has released its Productivity Insights 2020 report, which shows that Australia’s productivity performance is poor:

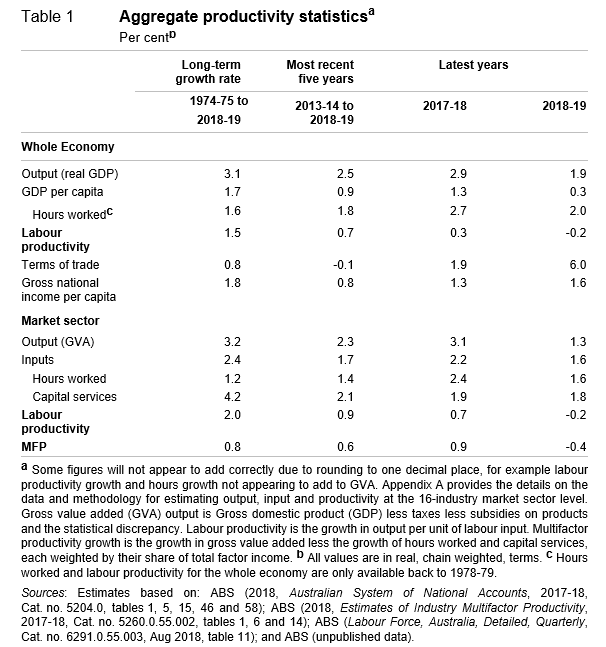

Accordingly, growth in per capita GDP has bombed:

According to the PC:

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement