DXY is up and away:

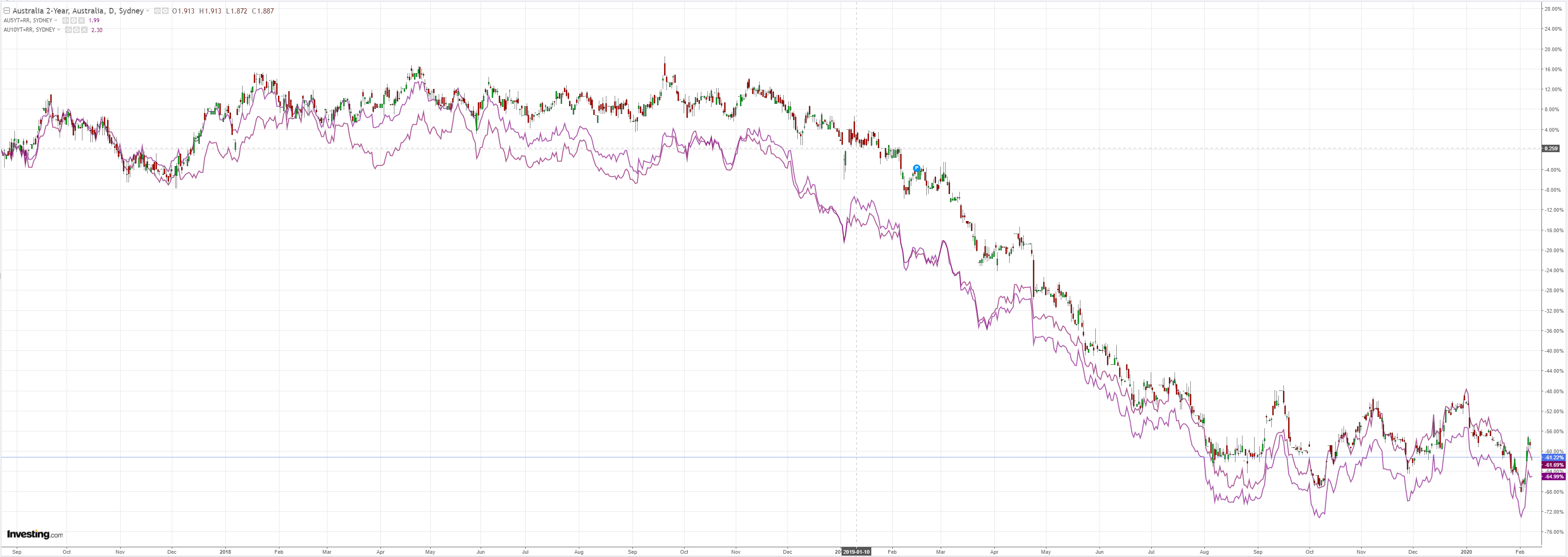

The Australian dollar was poleaxed to eleven year lows versus DMs:

EMs were even weaker:

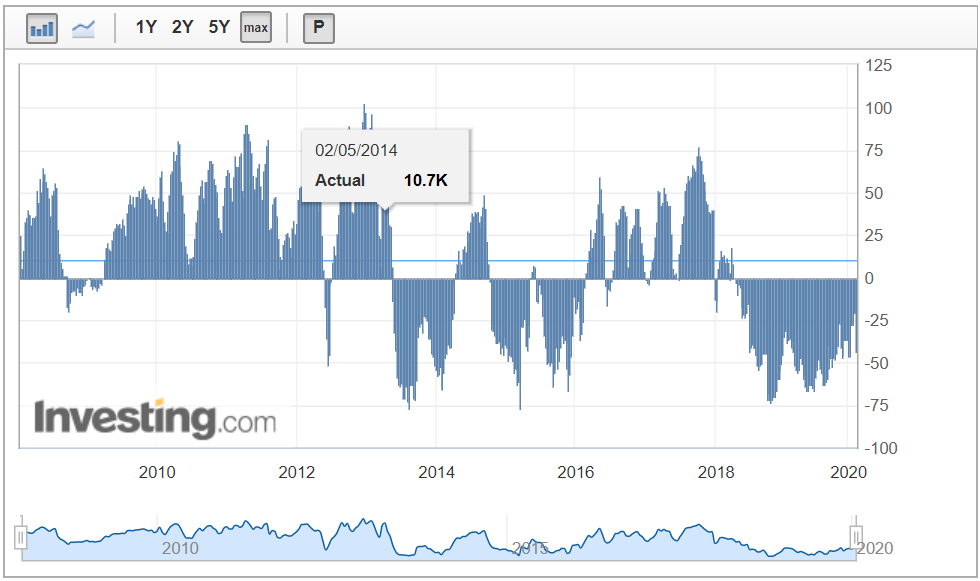

CFTC positioning shifted sharply shorter at -43k contracts. Still room to move lower:

Gold is simmering:

Oil is weak despite OPEC bleating:

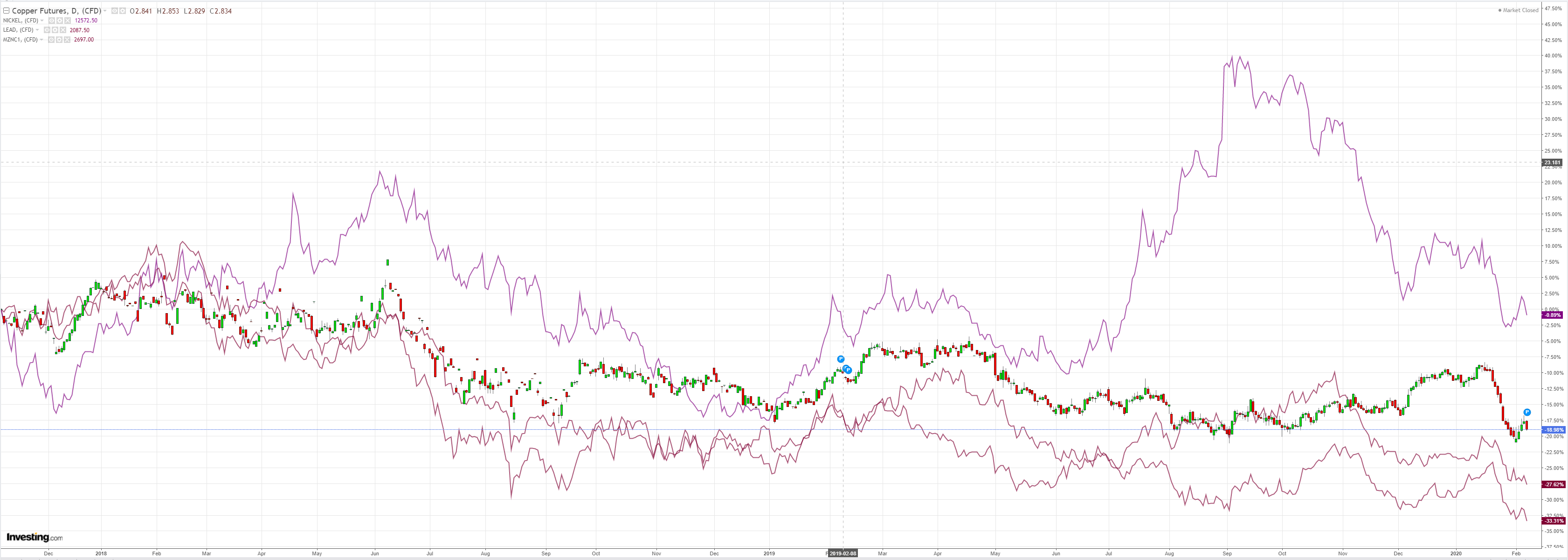

Metals rolled:

Miners were smashed:

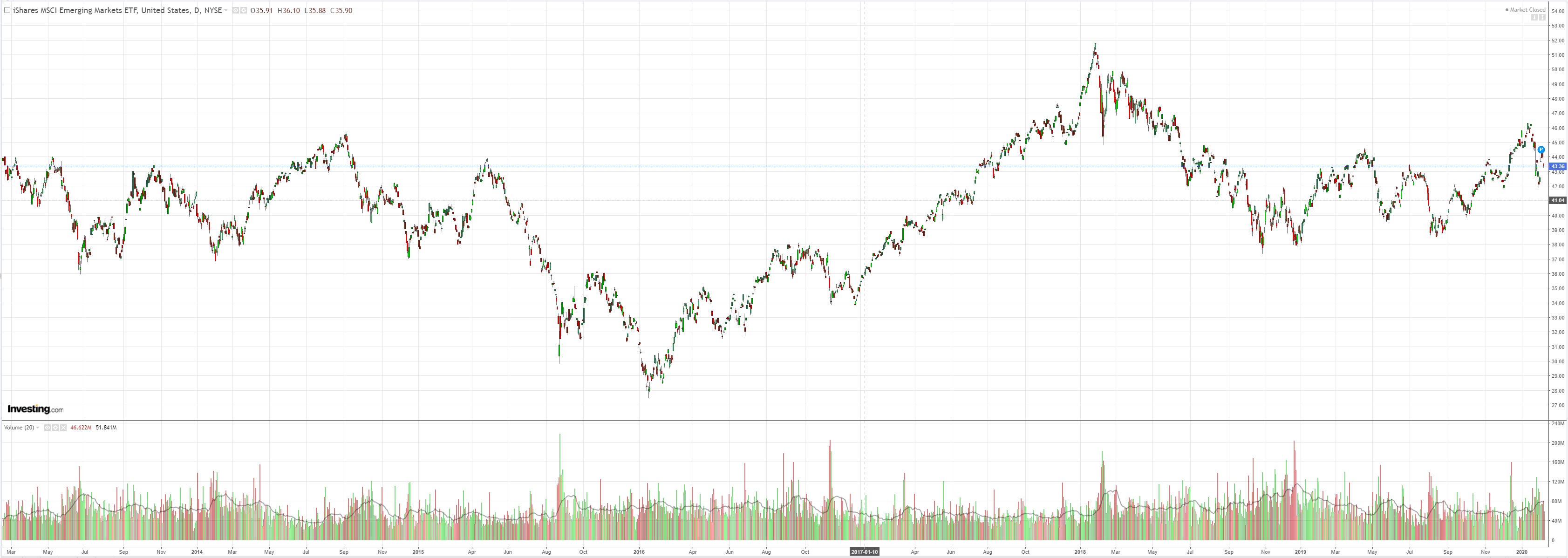

EM stocks rolled:

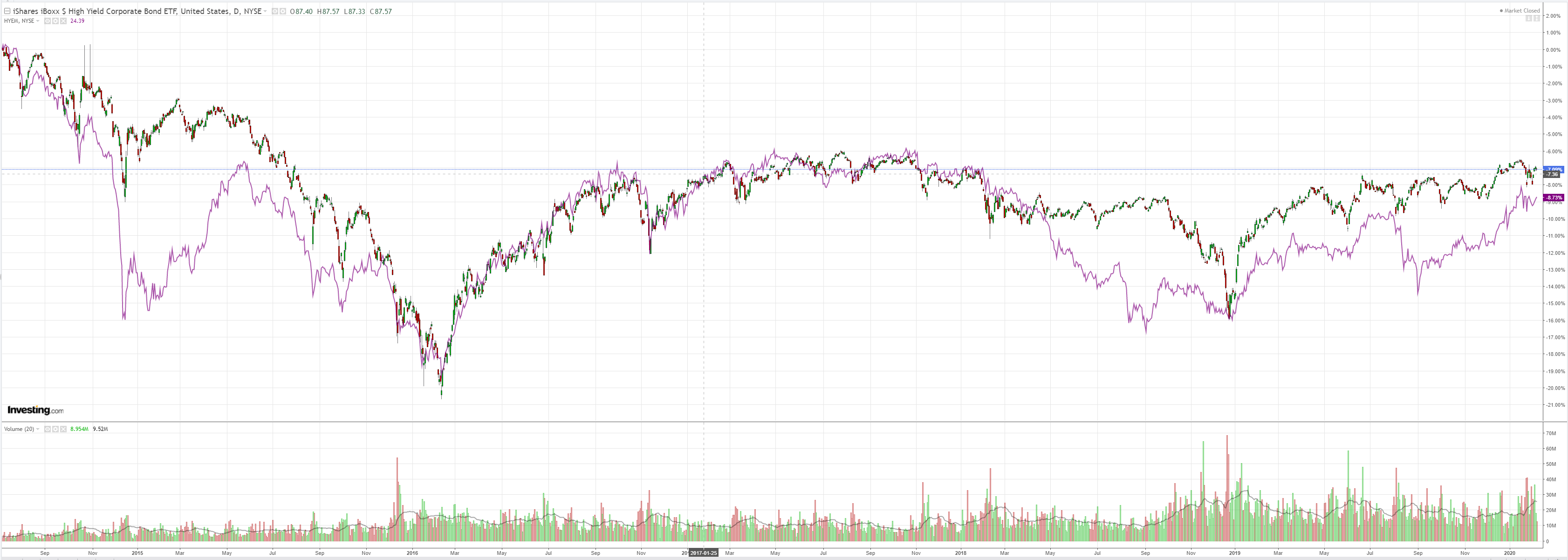

Junk remains bizarrely serene:

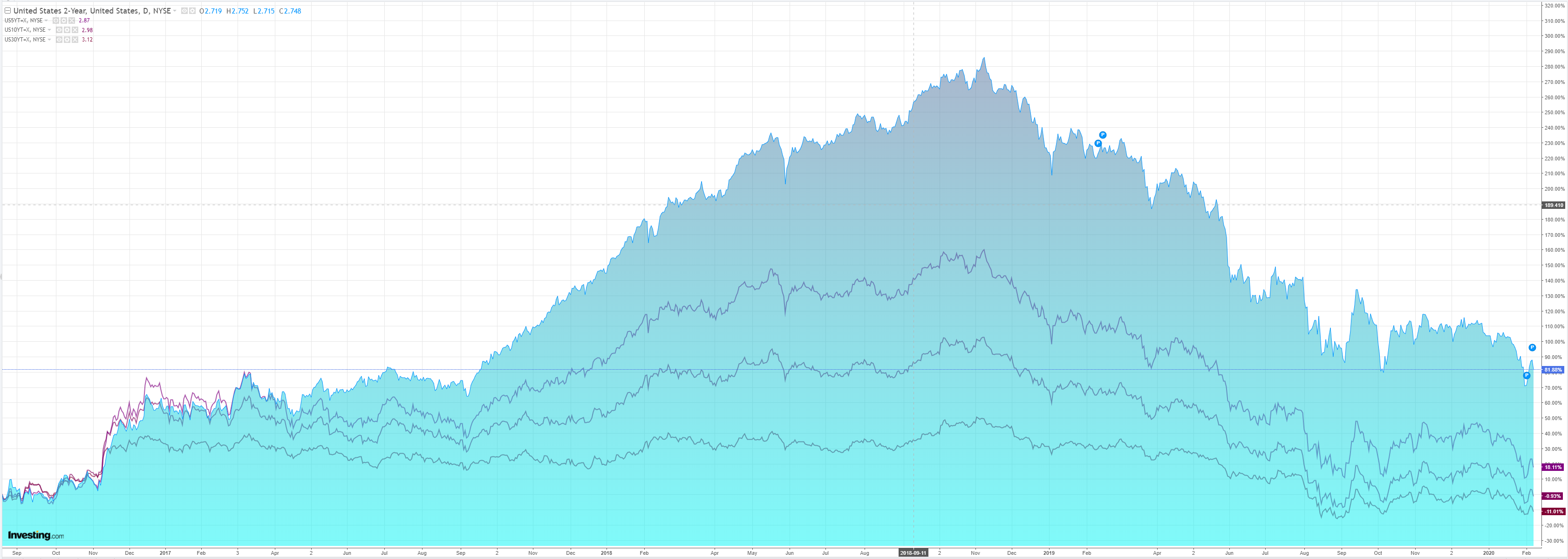

Bonds were all bid:

As stocks pulled back modestly:

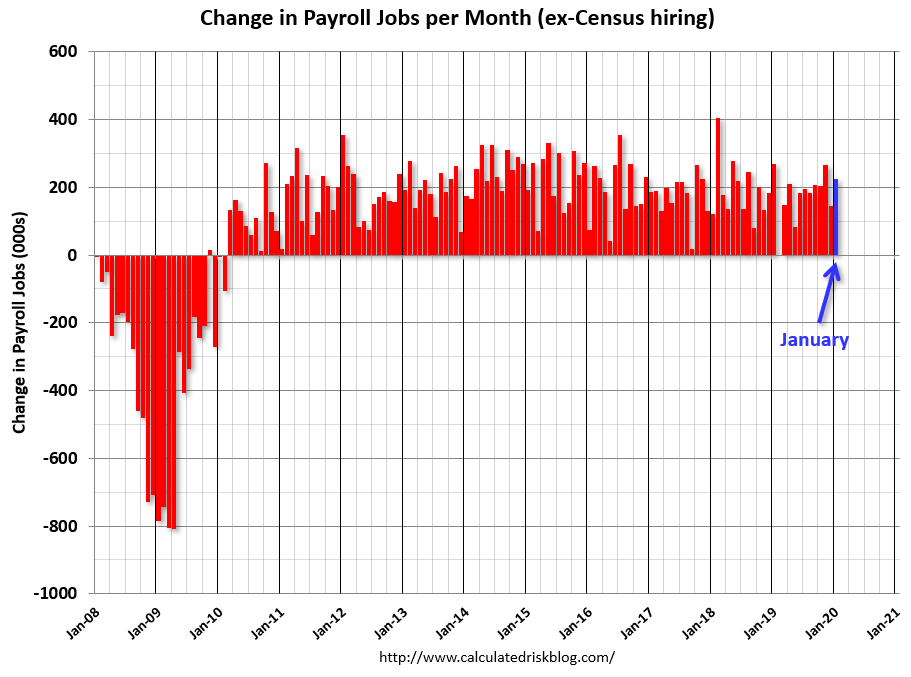

The big data release was US jobs:

Total nonfarm payroll employment rose by 225,000 in January, and the unemployment rate was little changed at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in construction, in health care, and in transportation and warehousing.

…The change in total nonfarm payroll employment for November was revised up by 5,000 from +256,000 to +261,000, and the change for December was revised up by 2,000 from +145,000 to +147,000. With these revisions, employment gains in November and December combined were 7,000 higher than previously reported.

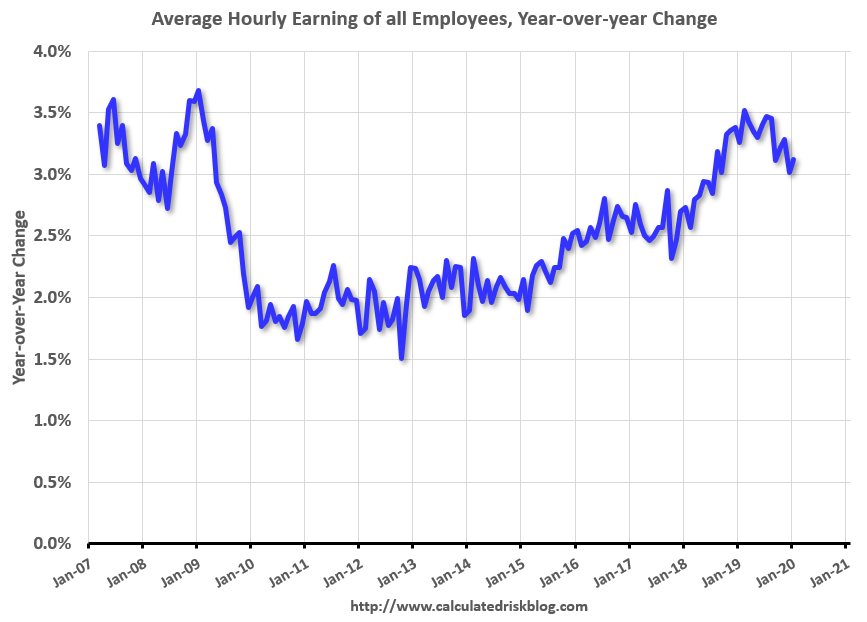

…In January, average hourly earnings for all employees on private nonfarm payrolls rose by 7 cents to $28.44. Over the past 12 months, average hourly earnings have increased by 3.1 percent.

Headline beat:

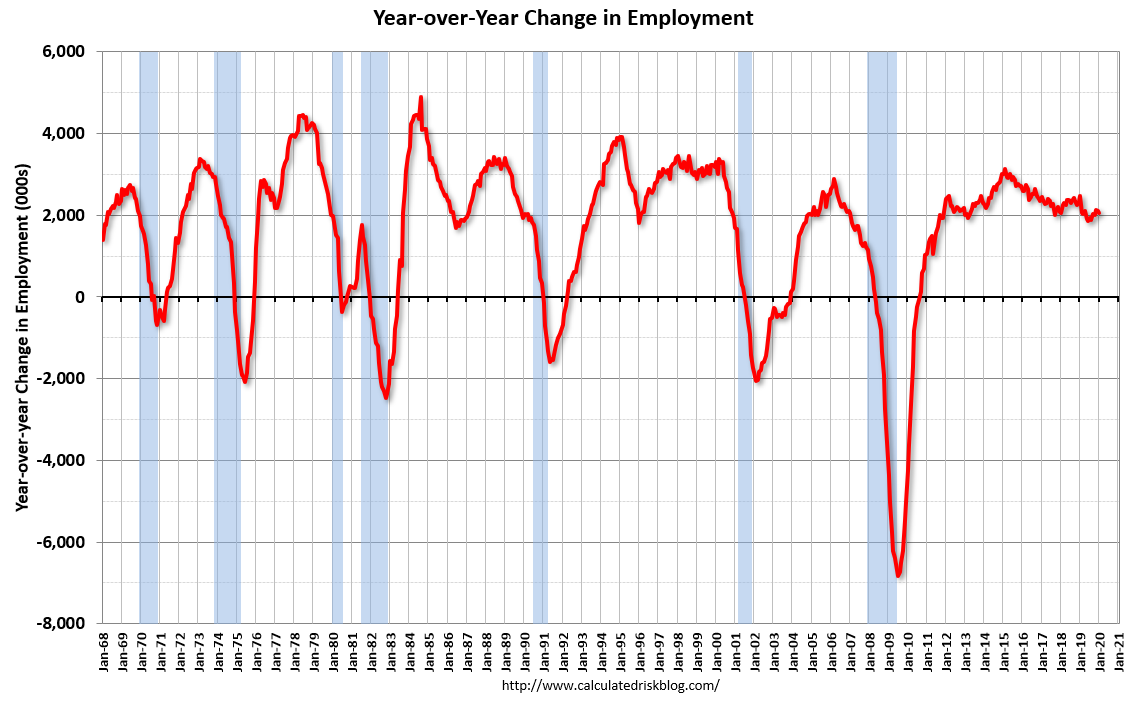

Jobs growth is solid:

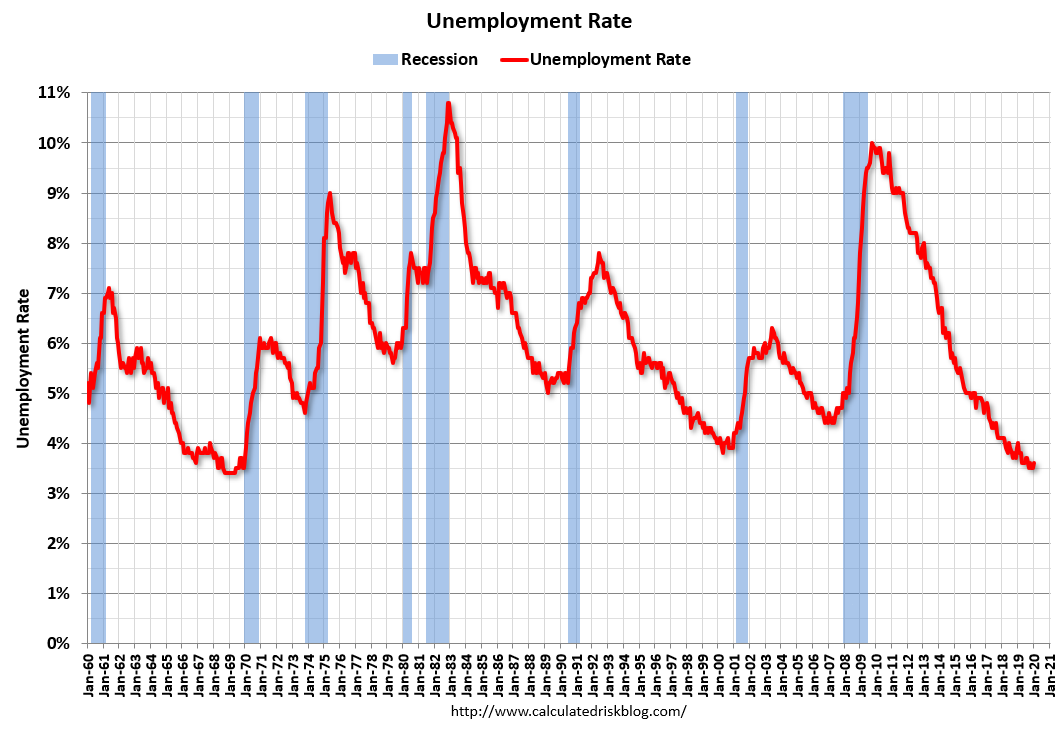

Unemployment very low:

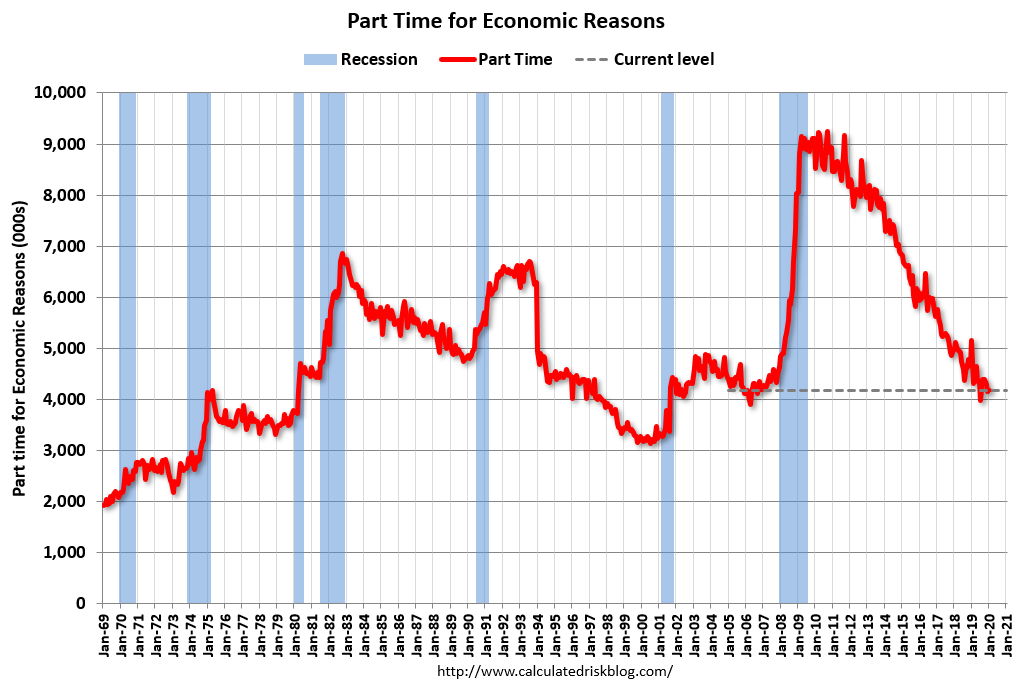

But underemployment more loose:

Wage growth firmed but the trend is weak:

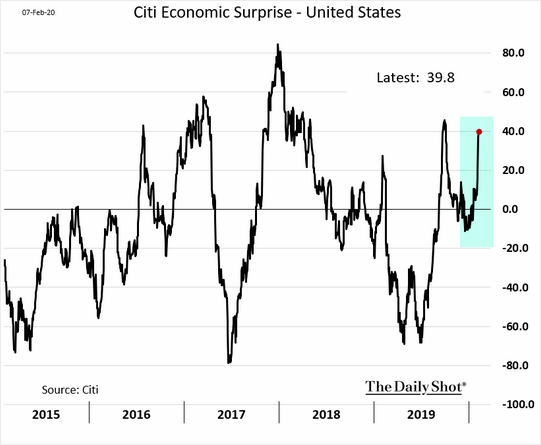

In short the US jobs market remains rock solid as housing and stocks support the consumer. That’s driving up expectations, which were too weak:

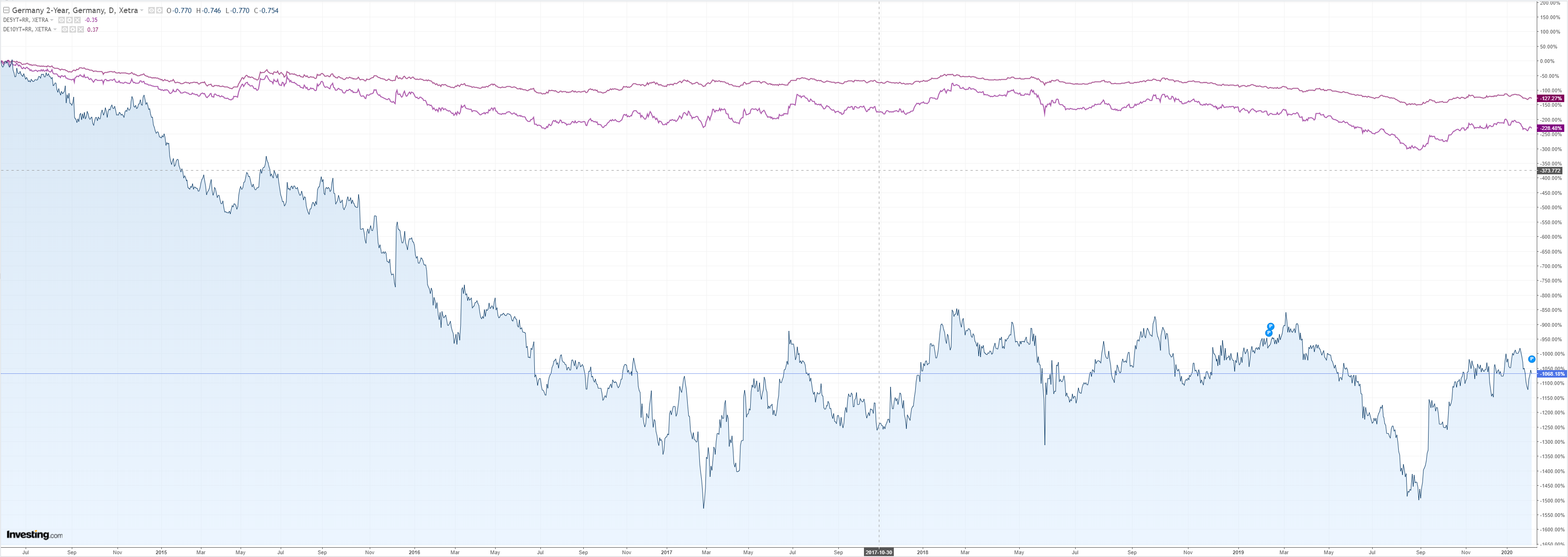

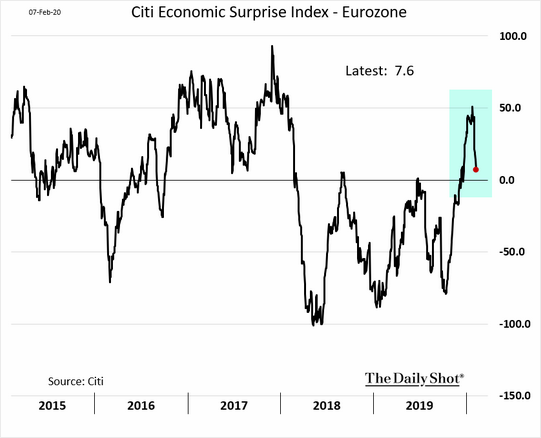

Meanwhile, Europe is going the other way:

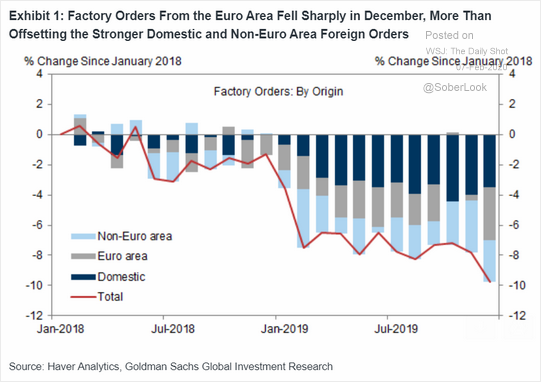

Driven by the external trade shock:

The hope was to see a rebound this year:

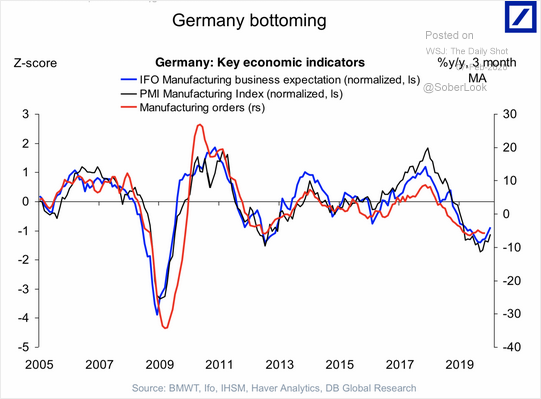

But Europe is much more exposed to Chinese import demand than America is, Germany in particular, so that hope is forlorn.

USD is clealy better postioned than EUR. That means a strong DXY and weak AUD at least until the virus shock passes.