The Australian Council of Trade Unions’ (ACTU) submission to The Retirement Income Review has demanded that the legislated increases in the superannuation guarantee to 12% be maintained for men and lifted to 15% for women:

Australian workers have been left out in the cold and are paying the price for the Coalition Government’s freeze on the Superannuation Guarantee…

Stagnant wage growth and the frozen Super Guarantee is a nasty combination that is shrinking the net worth of retirement savings for Australian workers according to ACTU Assistant Secretary, Scott Connolly.

“The notion that cutting wages will inspire employers to suddenly boost their superannuation contributions or vice versa is pure fantasy.

“Too many Australians are starting to see their plans for a comfortable retirement after a lifetime of work being eroded by low wage growth and the Morrison government straight jacket on the Super Guarantee,” Mr Connolly said.

The ACTU’s submission to The Retirement Income Review that has been commissioned by the Federal Government will emphasise the need to raise the Super Guarantee to 12% and accelerate its growth to 15% for working women.

Mr Connolly said fighting for a stronger Superannuation guarantee was vital.

“Australian workers should expect the government to be their champion when it comes to enjoying a decent retirement. Working people have created a superannuation system that is the best in the world, and we won’t let it be nobbled by Scott Morrison and his government.”

Clearly, the ACTU has missed the abundant evidence showing that the superannuation guarantee is paid for by workers (not employers) via lower take-home pay (less disposable income), with lower income earners most adversely impacted.

In case you have been living under a rock, here are the findings of the Henry Tax Review, which explicitly recommended against raising the superannuation guarantee:

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

Here’s the Grattan Institute’s latest modelling, released last week:

On average 80% of the cost of increased compulsory super contributions was passed on to workers through lower wage rises than would have been expected over the life of those agreements. The long-term impact is likely to have been higher…

It is unlikely the leglislated future step ups in compulsory super contributions will be different from the earlier ones.

Although wage growth is slower now than in the past, wages are nevertheless – by all measures – growing by more than 2% a year, offering ample room for employers to wind back wage increases in order to fund each of the five scheduled annual step ups of 0.5% in compulsory super contributions that begin on July 1, 2021.

In fact, if workers’ bargaining power has fallen recently – as some suggest – employers might feel they can push even more of the cost of higher super onto workers than in the past.

Which was supported in full by the Reserve Bank of Australia:

RBA assistant governor Luci Ellis said it had “shaved” its worker pay forecasts to reflect that higher compulsory super will dampen future wage growth for private sector workers, offsetting wage increase pressures from a tightening labour market.

Wage growth would have got “a little bit of a pick-up from here” if not for the legislated requirement for business to boost their superannuation contributions, Dr Ellis said.

“Historically about 80 percent of the increase in the non-cash benefit tends to show up as somewhat slower wages growth than what you would have otherwise seen.”

So basically, the ACTU supports lowering its members’ take-home pay so that it can increase the funds under management of its union-backed industry superannuation funds.

The ACTU’s demand to increase the superannuation guarantee for women to 15% also makes no sense, given this would further erode women’s take-home pay.

The inherent bias against women’s superannuation stems from the inequitable way that concessions are distributed, which disadvantages lower paid workers irrespective of gender.

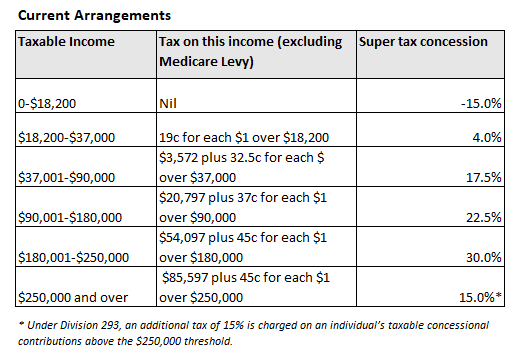

Under existing arrangements, superannuation contributions/earnings are taxed at a flat rate of 15%. As such, those on lower incomes receive minimal concessions, whereas those on higher incomes receive the biggest tax concessions:

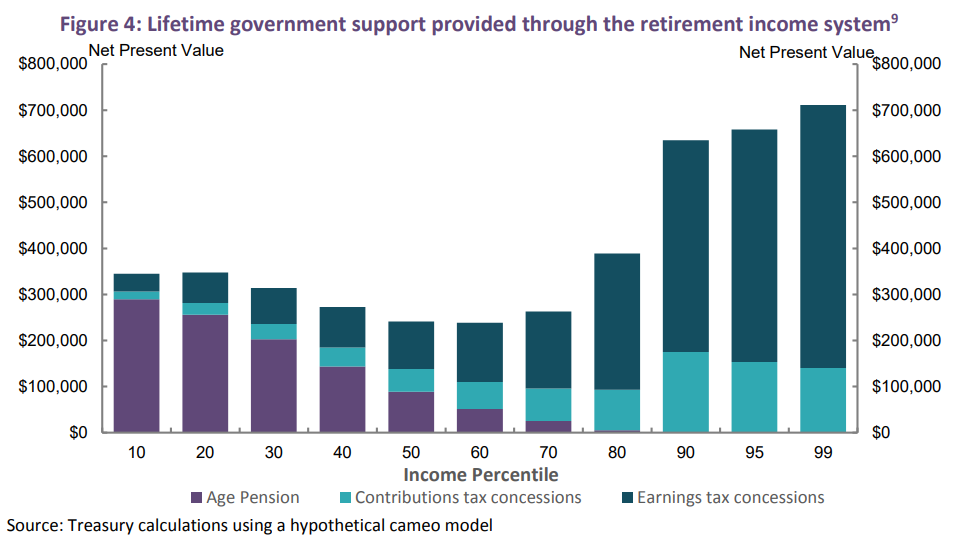

As a result, the top 1% of income earners (mostly men) will receive over $700,000 in taxpayer contributions to their personal superannuation accounts over their working lives compared to just $50,000 received by the bottom 10% of income earners, according to the Australian Treasury:

The first best solution to this problem is to reform the superannuation system to make concessions more equitable and sustainable. This would benefit low income earners irrespective of gender.

Moreover, simply lifting the superannuation guarantee, as demanded by the ACTU, would heighten the gross inequities already plaguing the system and would deprive workers of much-needed disposable income at a time of sluggish wage growth.

Given the ACTU has its fingers in the Industry Superannuation pie, and raising the superannuation guarantee would grow their funds under management, maybe this is its intention?

Because the ACTU certainly doesn’t seem to care about the welfare of ordinary workers.